April 2026

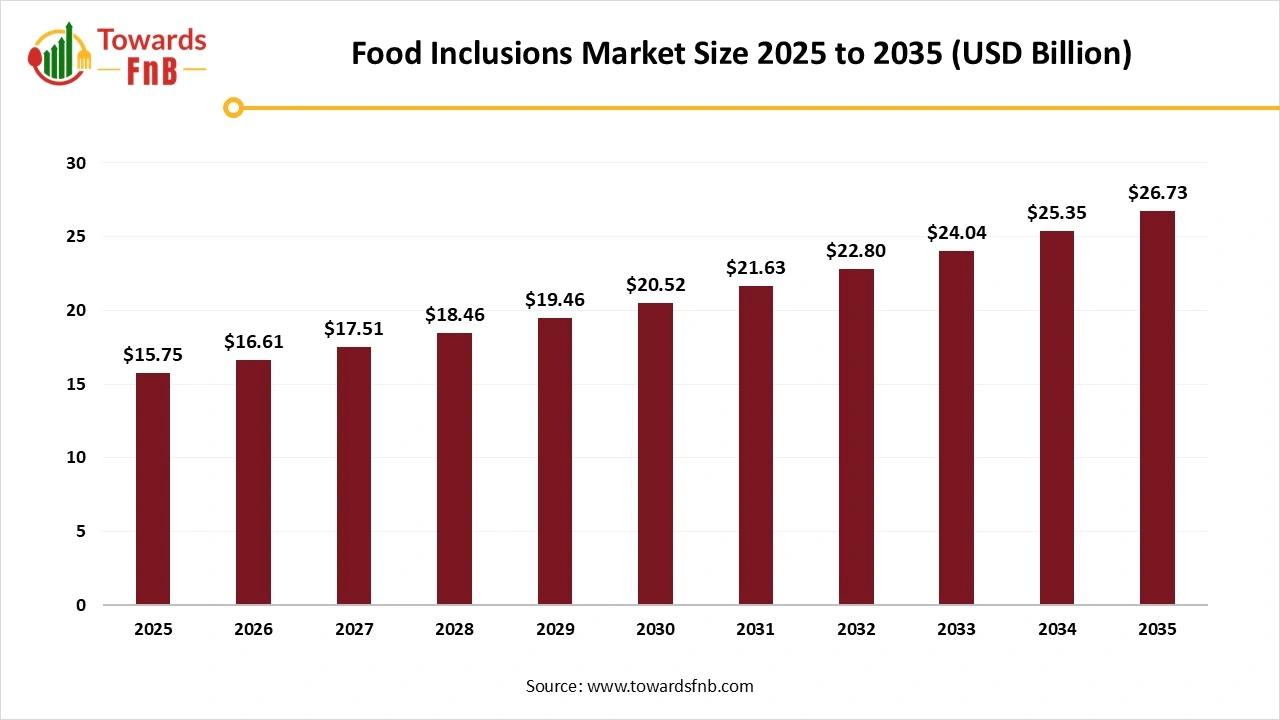

The global food inclusions market size reached at USD 15.75 billion in 2025 and is anticipated to increase from USD 16.61 billion in 2026 to an estimated USD 26.73 billion by 2035, witnessing a CAGR of 5.43% during the forecast period from 2026 to 2035. The food inclusions market is driven by the increasing consumer demand for premium products with new textures and flavors.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.43% |

| Market Size in 2026 | USD 16.61 Billion |

| Market Size in 2027 | USD 17.51 Billion |

| Market Size by 2035 | USD 26.73 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The food inclusions market refers to ingredients added to food and beverage products to enhance flavor, texture, color, and appearance. These inclusions include chocolate chips, fruit pieces, nuts, candies, and cereals used in bakery, dairy, confectionery, snacks, and beverages. They improve sensory appeal, nutritional value, and product differentiation. The market’s growth is driven by rising demand for premium, customized, and clean label products, alongside innovation in natural and functional inclusions for health-conscious consumers worldwide.

The food inclusions market growth is driven by the rising innovation in the dairy, bakery and confectionery, increasing consumer awareness of nutritional and functional benefits, and increasing demand for value-added and convenience products. In addition, rising technological advancements in food processing, rising popularity of clean-label and healthy options and increasing consumer demand for artisanal and premium products are further expected to drive the market growth during the forecast period.

The rise of technological advancements in the food inclusions industry is focusing on improving functionality, stability and quality, driven by innovations such as 3D printing, microencapsulation, and freeze-drying. These technologies enable customization to address consumer demands for plant-based, natural and healthier options and help create products with enhanced shelf-life, flavor and texture. In addition, IoT integration, advanced sensors, and AI-based tools are ensuring food safety and quality and streamlining product development throughout the supply chain, which further expected to further revolutionize the growth of the food inclusions market in the coming years.

Raw Material Procurement

Packaging and Branding

Waste Management and Recycling

| Region/Country | Regulatory Authority | Key Regulations / Standards | Relevance to Food Inclusions Industry |

| United States | Food and Drug Administration (FDA) | FDA Food Safety Modernization Act (FSMA); CFR Title 21 for food additives and colourants | Governs safety standards, approved additives, allergen controls, facility hygiene and labelling requirements. |

| European Union | European Food Safety Authority (EFSA); European Commission | EU Regulation (EC) No 1333/2008 on food additives; General Food Law Regulation (EC) 178/2002 | Sets harmonised rules for ingredient safety, allowable colourants, clean-label definitions and traceability. |

| United Kingdom | Food Standards Agency (FSA) | Food Additives, Flavourings, Enzymes and Extraction Solvents Regulations 2013 | Maintains safety rules for colours, inclusions and flavouring ingredients used in foods after post-Brexit alignment. |

| Canada | Health Canada; Canadian Food Inspection Agency (CFIA) | Food and Drug Regulations (FDR); Safe Food for Canadians Regulations (SFCR) | Defines permitted additives, allergen labelling and safety controls for processed inclusions. |

| Australia / New Zealand | Food Standards Australia New Zealand (FSANZ) | Food Standards Code, Standard 1.3.1 on Food Additives | Determines allowed colours and inclusion ingredients, purity requirements and food safety testing. |

| India | Food Safety and Standards Authority of India (FSSAI) | FSSAI Food Safety and Standards Regulations; Food Additives Regulations 2011 | Specifies approved colours, flavouring substances, microbial limits and safety practices for inclusion manufacturers. |

| China | National Health Commission (NHC); State Administration for Market Regulation (SAMR) | GB Standards (GB 2760 for additives; GB 14880 for nutrient fortification) | Regulates additive use, contaminant limits, colour approvals and quality testing for processed food inclusions. |

| Japan | Ministry of Health, Labour and Welfare (MHLW) | Food Sanitation Act; Standards for Food Additives | Establishes strict purity, additive safety and quality rules for inclusions in confectionery and bakery applications. |

| Brazil | National Health Surveillance Agency (ANVISA) | Resolution RDC No. 45 and RDC No. 239 for additives and colour approvals | Controls approved colourants, ingredient limits, allergenic substances, and labelling for packaged inclusions. |

| Gulf Cooperation Council (GCC) | Gulf Standardization Organization (GSO) | GSO Food Additive Standards; GCC Unified Food Law | Harmonises the additive approvals and testing requirements across Gulf markets for food inclusions. |

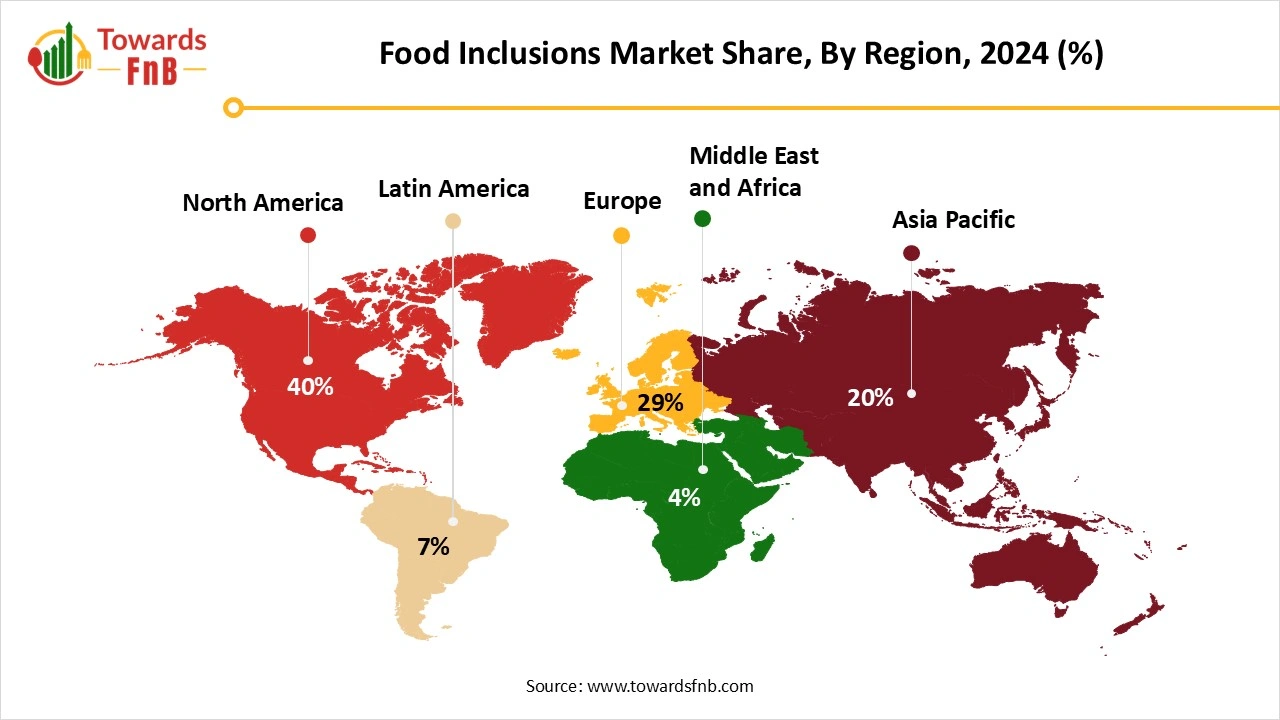

Why is North America Dominating the Food Inclusions Market?

North America dominated the global market revenue in 2025. The market growth in the region is witnessing rapid growth, driven by the demand for plant-based, clean-label and sustainable food products in the food and beverage industry. Major factors such as the increasing applications in alternative baked goods, snacks and convenience foods and increasing demand for frozen food and increasing consumer demand for dairy products. The U.S. and Canada are the major drivers of market growth.

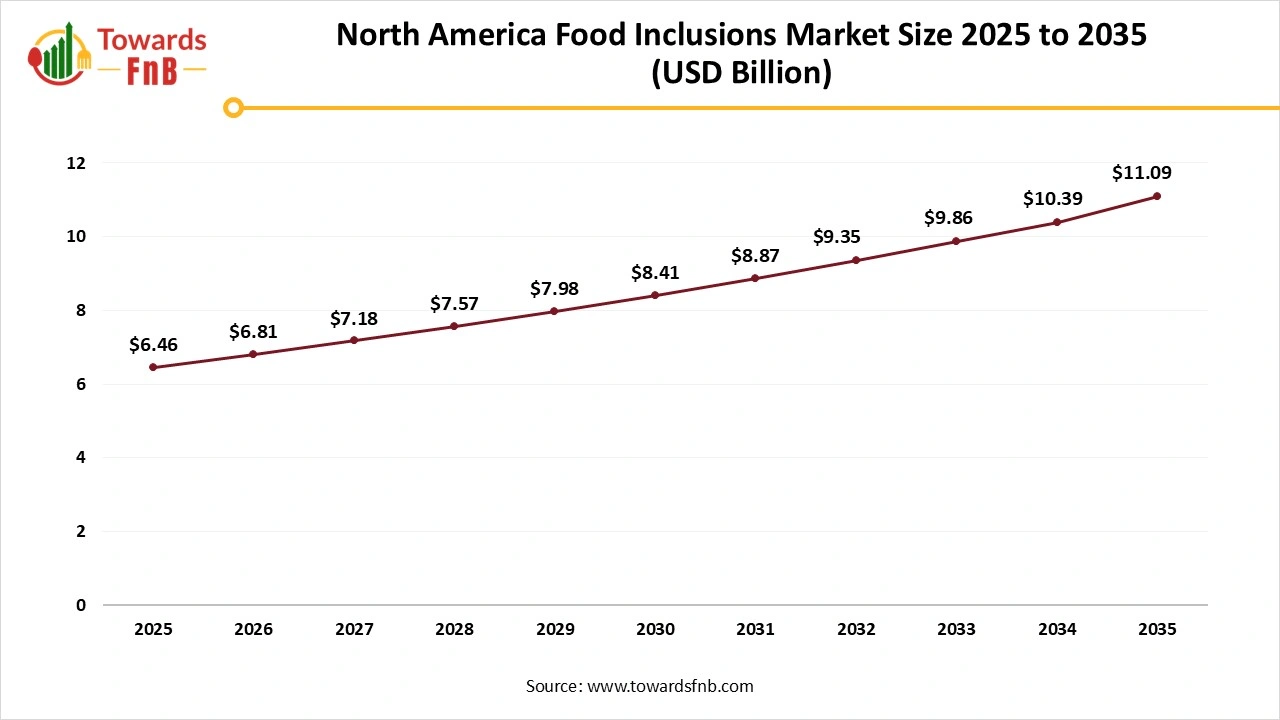

North America Food Inclusions Market Size 2025 to 2035

The North America food inclusions market size was valued at USD 6.46 billion in 2025 and is anticipated to increase from USD 6.81 billion in 2026 to an estimated USD 11.09 billion by 2035, witnessing a CAGR of 5.55% during the forecast period from 2026 to 2035.

The U.S. Food Inclusions Market Trends

The U.S. dominated to global market revenue, with demand driven by the popularity of frozen and processed goods, clean-label products, increasing use of dairy alternatives, increasing consumer focus on health and wellness, and increasing demand for sustainable and plant-based products such as dairy and bakery and snacks.

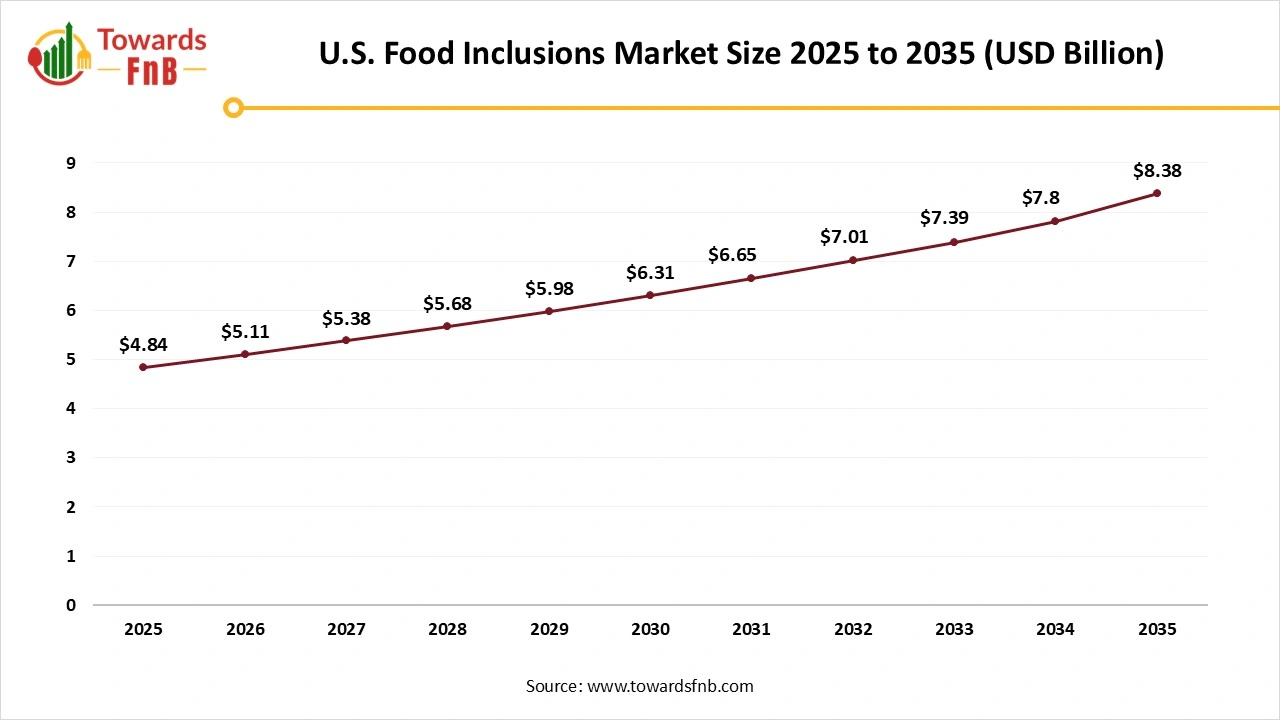

U.S. Food Inclusions Market Size 2025 to 2035

The U.S. food inclusions market size was calculated at USD 4.84 billion in 2025 and is anticipated to increase from USD 5.11 billion in 2026 to an estimated USD 8.38 billion by 2035, witnessing a CAGR of 5.64% during the forecast period from 2026 to 2035.

Asia Pacific is Expected to Grow at an 8% CAGR During the Forecast Period

The global market growth in the region is attributed to the factors such as increasing applications in the food and beverage, increasing awareness of health and environmental benefits, rising technological advancements in protein engineering, increasing consumer demand for plant-based, natural and sustainable ingredients, increasing significant investment in the food industry, increasing demand for alternative food products and increasing demand for dairy alternatives such as cheese, ice cream, snacks and milk. China, India, Japan and South Korea are the fastest-growing countries driving the market growth.

India Food Inclusions Market Trends

India is expected to grow fastest during the forecast period. The global food inclusions industry in India is growing rapidly, driven by increasing demand dairy alternatives and natural products, increasing government supportive initiatives, expansion of food and beverage industry, increasing consumer popularity of sustainable and natural ingredients and increasing demand for frozen desserts, frozen foods and ready-to-eat meals.

")

Europe is Expected to Grow at a Notable Rate During the Forecast Period

The global food inclusions market is driven by the increasing demand for natural and healthier products for its nutritional products, increasing growth of the well-developed food and beverage industry, increasing demand for processed and frozen goods, technological advancements, increasing food safety regulations and increasing demand for processed food, bakery and confectionery. The UK, Germany and France are the major countries driving the market growth.

Germany Food Inclusions Market Trends

The food inclusions industry in Germany is driven by growing consumer interest in plant-based, vegan and gluten-free diets, which has increased demand for clean-label and naturally sourced ingredients. Technological progress in protein engineering, extrusion and ingredient processing is enabling manufacturers to create inclusions with improved texture, stability and nutritional value. German consumers also show a strong appetite for new flavour profiles and multisensory eating experiences, which supports the rise of textured inclusions in bakery, confectionery, dairy and snack products. This sustained focus on natural, functional and texture-rich ingredients continues to shape innovation and market expansion across the country.

Latin America Food Inclusions Market Trends

The market growth in the region is driven by the increasing large consumer base, growing rapid urbanization, growing food and beverage, increasing use of protein in alternative ingredients, increasing consumer preference in sustainable food ingredient and confectionery, expanding food and beverage industry, increasing consumer preference towards vegan and gluten-free options, increasing need for greater regulatory support and increasing consumer preference for natural, plant-based and healthier options. Brazil, Mexico and Argentina are the major countries driving the market growth.

Mexico Food Inclusions Market Trends

The market growth in the country is driven by increasing demand for sustainable and alternative food options and expanding food and beverage industries, especially convenience and frozen foods. Other factors such as the growing fermentation applications in food and beverages and growing strong food processing industry, rising technological advancements in inclusions and increasing demand for baked goods and snacks.

Middle East and Africa Is a Significant Region in the Market in 2025

The food inclusions market growth in the region is driven by factors such as increasing support from private and government initiatives, increasing investment in efficiency improvements and food processing industry, increasing use of fermentation in various industries, increasing need to improve cold chain logistics for foods, increasing disposable incomes, growing food and beverage industry and rising rapid urbanization. South Africa, UAE, Saudi Arabia and Kuwait are the major countries driving the market growth.

South Africa Food Inclusions Market Trends

The food and beverage industry is the largest consumer in the country, driven by increasing consumer demand for premium and healthier options such as confectioneries, dairy and bakery items, increasing consumer trend towards nutrient-rich additions such as nuts and fruits, rising investment in research and development activities, increasing versatility in baking and sweets and increasing demand for plant-based protein in food and beverages.

Ketones Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Chocolate Inclusions | 48.5% |

| Fruit & Nut Inclusions | 20% |

| Cereal Inclusions | 15% |

| Flavored Sugar & Caramel Inclusions | 16.5% |

Why is the Chocolate Inclusions Segment Dominating the Food Inclusions Market?

The chocolate inclusions segment dominated the global market, accounting for 48.5% of revenue in 2025. Chocolate inclusions play an important role in the food inclusions industry as they drive demand for high-quality products by improving visual appeal, adding rich texture and enhancing flavor. Their versatility enables them to be used across a huge range of products across the globe, such as desserts, snacks and baked products. In addition, chocolate inclusions offer intense, creamy and rich flavors and improve the overall texture and taste of food products that enhance consumer satisfaction.

The Fruit & Nut Inclusions Segment is Expected to Grow Fastest 7% CAGR During the Forecast Period

Segment growth in the food inclusions market is driven by the increasing popularity of functional and plant-based foods, technological advancements, the growth of processed foods such as baked goods and snacks, the focus on clean label ingredients, and consumer demand for premium, convenient, and healthy products.

The cereal inclusions segment is expected to grow at a notable rate during the forecast period. The segment growth in the global market is attributed to the increasing demand for convenience food, such as bakery products, snack bars and breakfast cereals, rising innovation in textures and flavors, increasing demand for functional, health and convenience foods and increasing consumer preference towards artisanal and premium products.

Ketones Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Solid Form | 68.9% |

| Liquid Form | 31.1% |

How is Solid Form Segment Dominating the Food Inclusions Market?

The solid form segment dominated the global market, accounting for 68.9% of revenue in 2025. The solid form plays an important role in the food inclusions industry as it provides visual appeal, flavor and texture to a huge variety of products. Solid inclusions such as pieces, flakes, chips and nuts are necessary for adding sensory qualities, catering to consumer demand for indulgent and premium foods and offering stability during food processing.

The Liquid Form Segment is Expected to Grow Fastest During the Forecast Period

The liquid form of food inclusions expanded application versatility compared to solid forms and offers unique functional properties. Its primary presence lies in providing essential smooth texture, flavor distribution and essential moisture in various food products. Liquid inclusions, including flavor extracts, chocolate drizzles, syrups and fruit juice, are crucial in products such as beverages, yogurt and ice-cream, where seamless integration and flow are needed, which further drives the segment growth.

Ketones Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Bakery & Confectionery | 43.3% |

| Dairy & Frozen Desserts | 20% |

| Snacks & Bars | 18.5% |

| Beverages | 18.2% |

What Factors Help Bakery and Confectionery Segment to Grow in 2025?

The bakery and confectionery segment dominated the global food inclusions market by having 43.3% of revenue in 2025. The segment growth in the global market is driven by the increasing demand for consumer desire for enhanced visual appeal, texture and flavor. Inclusions such as fruits, nuts and chocolate chips are necessary for creating functional, premium and unique products, and they a major segment for product innovation and market growth. Manufacturers are rapidly adopting inclusions to deliver functional benefits, such as fiber-packed grains or protein-enriched crisps, further driving segment growth.

The Dairy and Frozen Desserts Segment is Expected to Grow at a 7.2% CAGR During the Forecast Period

The segment growth in the food inclusions market is driven by the rising innovation in inclusions such as nuts, fruit and cookie dough, increasing consumer trend towards plant-based, clean-label and healthier options, increasing demand for innovative and premium products, enhance texture and flavor. Dairy and frozen dessert help create a more engaging eating experience and add flavor and texture complexity that enhance the product from basic to premium indulgence.

The beverages segment is expected to grow at a notable rate during the forecast period. The segment growth in the food inclusions market is driven by the increasing demand for convenient and new products, rising urbanization, increasing disposable incomes, increasing demand for clean-label, plant-based and natural ingredients and increasing consumer awareness towards health and wellness.

Why is B2B Segment is Dominating the Food Inclusions Market?

The B2B segment dominated the global market, accounting for 72.3% of revenue in 2025. The B2B distribution channel offers major benefits in the food inclusions industry by providing valuable data-driven insights, expanding market reach, reducing operational costs, and increasing efficiency. This approach enhances the supply chains and helps meet the demands of digitally native and modern buyers. In addition, B2B platforms automate the inventory, invoicing, and ordering management processes, which minimizes administrative burdens and manual errors.

The B2C Segment is Expected to Grow at a 7.3% CAGR During the Forecast Period

The B2C channel offers major benefits in the food inclusions market by allowing for greater control over the sales process and data, fostering brand loyalty and enabling direct customer engagement. The B2C channel also increased market accessibility, improved flexibility, enhanced brand building, and strengthened direct customer relationships and insights, which are expected to further drive market growth.

The Ministry of Statistics and Program Implementation (MoSPI)

By Type

By Form

By Application

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Food Inclusions Market