April 2026

The global legumes market size stood at USD 15.23 billion in 2025 and is anticipated to increase from USD 16.04 billion in 2026 to an estimated USD 25.65 billion by 2035, witnessing a CAGR of 5.35% during the forecast period from 2026 to 2035. Rising health consciousness and the increasing demand for plant-based and sustainable food products significantly driving the market.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.35% |

| Market Size in 2026 | USD 16.04 Billion |

| Market Size in 2027 | USD 16.90 Billion |

| Market Size by 2035 | USD 24.08 Billion |

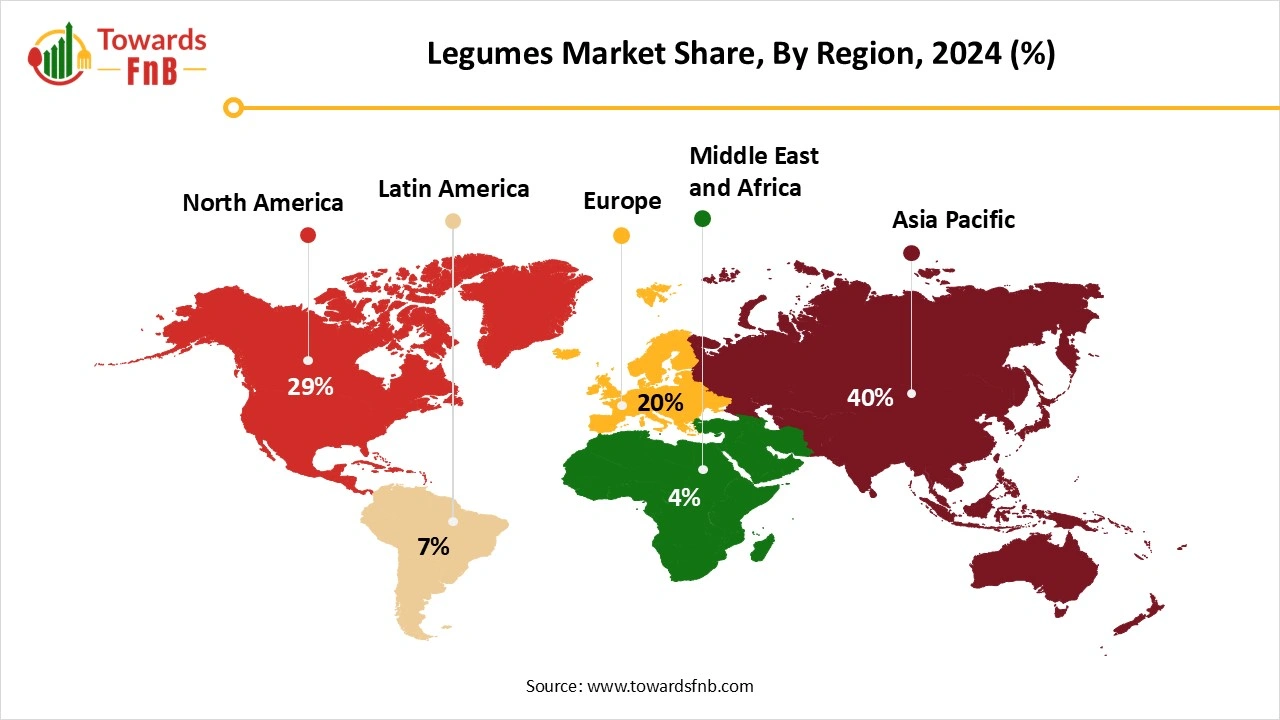

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The global legumes market encompasses the production, processing, and distribution of edible seeds from leguminous plants such as lentils, beans, chickpeas, and peas. These crops are a vital source of plant-based protein, dietary fibers, and essential micronutrients, making them a cornerstone of both human and animal nutrition. Demand for legumes is driven by their nutritional benefits, sustainability profile, and their increasing use in plant-based food formulations and meat alternatives. The market growth is also supported by shifting dietary preferences toward protein-rich and environmentally sustainable food sources, advancements in agricultural productivity, and expansion of value-added legume-based products in food, feed, and nutraceuticals industries.

The scientists have exerted significant effort to acquire novel genetic attributes in legumes, including yield, stress resilience, and nutritional value. In recent times, the notable surge in genomic resources for leguminous plants has established a foundation for utilizing advanced breeding technologies, including transgenic methods, genome editing, and genomic selection for enhancing crops. Innovations in legume processing emphasize unconventional techniques such as ultrasound, high hydrostatic pressure (HHP), and microwave/pulse electric field methods, enhancing protein digestibility, nutritional value, and shelf life while minimizing antinutrients.

In October 2023, the European Union's Horizon Europe program initiated an ambitious project, ‘Breeding European Legumes for Increased Sustainability’, aimed at establishing a strong foundation for the legume breeding community in both research and industry throughout Europe. Featuring a consortium of 34 partners across 18 nations, comprising research institutions, plant breeders, seed firms, regulatory agencies, and advisory services, BELIS is set to address critical issues in legume breeding research and the production of varieties. BELIS leads the way in incorporating advanced technologies into legume breeding to enhance genetic improvements for developing new varieties.

Raw Material Procurement

Processing of Legumes

Packaging of Legumes

What Factors are Driving the Demand of Legumes in Asia Pacific?

Asia Pacific dominated the legumes market in 2025. This dominance emerges from increasing demand for healthy food, governmental backing, and advancements in agriculture, driven by market growth in China and India. Increasing recognition of the health advantages of legumes is driving up demand. The market is experiencing an increase in processed and ready-to-eat items, as consumers look for convenient choices that need minimal preparation. The increasing population of employed individuals and households with two incomes enhances the need for easy food choices such as canned beans.

Asia Pacific Legumes Market Size and Growth 2025 to 2035

The global legumes market size was valued at USD 6.24 billion in 2025 and is anticipated to increase from USD 6.58 billion in 2026 to an estimated USD 10.64 billion by 2035, witnessing a CAGR of 5.48% during the forecast period from 2026 to 2035.

India Legumes Market Trends

The increasing population boosts demand because legumes act as an economical and nutritious main food source. The United Nations Organization (UNO) predicts that India's population will hit 1.45 billion in 2024, peaking at 1.69 billion by 2054. In addition, the expanding food processing sector generates demand, as beans are utilized in ready-to-eat (RTE) meals, snacks, and packaged food items. Rising disposable incomes and evolving eating patterns result in a greater consumption of various dry bean types, boosting their market worth. Demand for exports is increasing as Indian dry beans become more popular in global markets.

Growing Health Awareness Expanding the Legumes Market in North America

North America expects the significant growth during the forecast period. Legumes have gained popularity among Americans in recent years because of their convenience. Due to the affordability, simplicity of preparation, and nutritional value of these items, individuals in the United States and Canada are incorporating them into their diets. Individuals dietary patterns are changing. The number of American consumers adopting vegetarianism and veganism is increasing. Increasing recognition of the ecological advantages of legumes, especially their importance in sustainable farming and soil wellness, is further driving demand. A notable trend is emerging in organic and specialty legume seeds, emphasizing high-yielding and disease-resistant varieties for sustainable agricultural practices.

U.S. Legumes Market Trends

The U.S. legumes market captured the largest revenue share of the regional industry due to an increasing number of health-conscious consumers opting for nutritious, plant-based options. The demand is being fueled by the rising popularity of vegetarian, vegan, and flexitarian diets, as consumers look for affordable and shelf-stable substitutes for animal protein. Moreover, the growth of online grocery shopping and rapid delivery services has rendered canned legumes more available than ever, thereby fostering market expansion.

")

Health and Sustainability Drive Growth in the European Legumes Market

The European market is set for expansion, driven by increased awareness of the health advantages of consuming legumes, an expanding vegetarian demographic, and heightened demand for plant-based protein. A significant trend driving this growth is the rising transition of consumers from meat to plant-based protein options, especially beans and peas, suggesting a favorable outlook for product development. Additionally, the market will gain from shifting consumer preferences for organic and healthy food options, along with a rising demand for clean-label products.

UK Legumes Market Trends

The UK legumes market is expanding, fueled by the need for convenient, affordable, and plant-based foods, particularly canned options. Important factors encompass a strong need for protein and fiber, the rise in popularity of vegan and vegetarian diets, and the cost-effectiveness of canned beans, particularly amid inflation. Although there is a robust market for processed and frozen peas and faba beans used in animal feed and for export, the UK mainly relies on imports of common beans; however, there is an opportunity to boost local production to satisfy demand.

The Middle East and Africa Legume Industry Dynamics

The Middle East and Africa depend on a combination of domestic farming and imports, with demand rooted in traditional eating habits and institutional avenues. Opportunities emerge from initiatives for food security, enhancements in cold-chain logistics, and packaged staples designed for budget-conscious consumers. Traders and brands focus on shelf-life stability, fortification, and distribution collaborations to expand their presence in urban and rural markets.

Saudi Arabia Legumes Market Trends

The legumes market in Saudi Arabia is experiencing robust growth, driven by increasing health awareness, rising plant based dietary preferences and strong import dependence. Government efforts under the national food security strategy, urbanisation, higher disposable incomes and expansion of modern retail channels are further accelerating demand for legumes in Saudi Arabia.

Latin America Legumes Market Dynamics

The legumes market in Latin America is experiencing steady but moderate growth, driven by traditional consumption habits, rising interest in plant-based proteins, and expanding modern retail channels. High-growth segments include canned legumes and chickpea protein isolates, benefiting from urbanization, higher disposable incomes, and increasing imports in several countries. Overall, the market is stable in traditional staples but shows stronger potential in processed and value-added products.

Mexico Legumes Market Trends

The legumes market in Mexico is undergoing dynamic change. The country is one of the major consumers in Latin America, with import volumes increasing significantly in 2025. Key drivers include strong cultural consumption of beans and other legumes, rising interest in plant based proteins, growing processing/retail channels, and increased imports to fill domestic supply gaps. Constraints include weather and crop production volatility, dependency on imports for certain pulses, and competition for farmland.

Why did the Soybean Segment Dominated the Legumes Market?

Soybeans segment led the legumes market in 2025. Soybeans are known for their health benefits, including being a good source of protein, fiber, vitamins, and minerals. The increasing consumer awareness of these advantages stimulates demand, especially for items such as soy milk, tofu, and protein supplements. The sector has undergone considerable expansion, fueled by nutritional, ecological, financial, and market influences. Dry common beans segment is seen to grow at a notable rate during the predicted timeframe. Dry beans offer a budget-friendly source of protein and vital nutrients in comparison to products derived from animals. They may be utilized in numerous conventional and creative meals, rendering them a valuable food source. India's export worth of Dried Common Bean has surged by 753.4% in the last 5 years, climbing from 2,445,195 USD in 2019 to 20,867,183 USD in 2023.

The Chickpeas Segment is Growing at a Significant Pace Throughout the Forecast Period.

Due to their high fiber content, they serve as an excellent snack for those aiming to manage diabetes or sustain a healthy weight, as it aids in digestion and promotes feelings of fullness. Moreover, the increasing demand for low-fat and high-amino acid products is providing a positive market perspective for chickpeas.

Legumes Market Share, By Product Form, 2025 (%)

| Segments | Shares (%) |

| Whole/Dried Beans & Pulses | 56% |

| Processed Ingredients (Flours, Protein Concentrates/Isolates) | 15% |

| Canned / Ready-to-eat | 10% |

| Frozen Legumes | 5% |

| Snacks & Ready-to-eat Pulse-based Foods | 8% |

| Seed & Planting Material | 6% |

Which Product Form Dominated the Legumes Market?

Whole/dried beans & pulses segment held the dominating share of the legumes market in 2025. The demand for whole legumes continues to be robust because of their nutritional benefits and low processing needs. The convenience of storage and extended shelf life additionally promotes widespread use among food manufacturers and families. Minimal processing helps retain more fiber, protein, and micronutrients, aligning with clean-label food trends.

Processed Ingredients Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Main factors involve the demand for high-protein, high-fiber components in products such as snacks, pasta, and meat substitutes, along with their application in gluten-free recipes. In this context, there exists an increased opportunity within the food sector for incorporating legume components into different food systems.

The canned/ready-to-eat segment is expanding rapidly as consumer demand for convenient food options increases due to the growing popularity of plant-based diets. Additionally, an increasing preference for canned legumes among food service providers like restaurants and catering services is expected to boost the adoption of legumes in the market.

Legumes Market Share, By End-User Industry, 2025 (%)

| Segments | Shares (%) |

| Food Manufacturers & Processors | 36% |

| Animal Feed Producers | 20% |

| Retail Consumers (grocery / household) | 15% |

| Foodservice & HORECA | 12% |

| Ingredient Suppliers / B2B | 9% |

| Industrial / Non-food Users | 8% |

Which End-User Industry Segment Dominated the Legumes Market?

Food Manufacturers & Processors segment dominated the market with the largest share in 2025. Manufacturers are continually developing new ways to include legumes in a variety of food items. This involves incorporating legume flours into baked goods, using textured proteins in meat substitutes, and adding legume extracts for enhanced nutrition in snacks and drinks. Large-scale food manufacturers gain from economies of scale and employ cutting-edge technologies to produce a significant number of legume-based products effectively.

Animal Feed Producers Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Driven by a strong and steady demand for legumes as an affordable, protein-dense component for livestock feed. Soybean are a nutrient-rich legume utilized for oil production and protein in animal feed. Legumes provide an economical option compared to other protein sources such as fishmeal.

Retail Consumers segment growing at a notable pace. Retailers have broadened their legume selections in various formats, such as canned, frozen, and ingredient-based snacks, to meet these shifting consumer preferences. Retailers have tapped into the need for fast and simple meal options by providing legumes in a broader assortment of convenient, value-added forms.

Legumes Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Bulk Wholesale / Commodity Exchanges | 41% |

| Supermarkets & Grocery Chains | 20% |

| Foodservice / Institutional Procurement | 15% |

| Specialty Natural / Organic Retailers | 10% |

| Online Grocery & DTC Ingredient Sales | 9% |

| Seed & Agri-input Channels | 5% |

Which Distribution Channel Dominated the Legumes Market?

Bulk wholesale/commodity exchanges segment held the largest share of the market in 2025. Purchasing and selling in large quantities significantly lowers the cost per unit for handling, storage, and transportation. Buying in bulk reduces risk for both purchasers and vendors. By consolidating the trade of substantial volumes, these markets provide stability and efficiency that smaller exchanges are unable to achieve.

Specialty Natural/Organic Retailers Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Flourishing by creating a tailored shopping experience that profoundly connects with their specific consumer demographic. These consumers emphasize health, environmental sustainability, and ethical manufacturing and are prepared to spend extra on goods that reflect their beliefs.

Supermarkets & grocery chain segment expanding rapidly, driven by consumer needs for convenience, reliability, and diversity, bolstered by sophisticated logistics and procurement strategies. They serve contemporary lifestyles with packaged, processed, and ready-to-eat legume items that smaller, conventional outlets cannot rival.

Heura

HARI&CO

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches/Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

By Type

By Product Form

By End-User Industry

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Legumes Market