April 2026

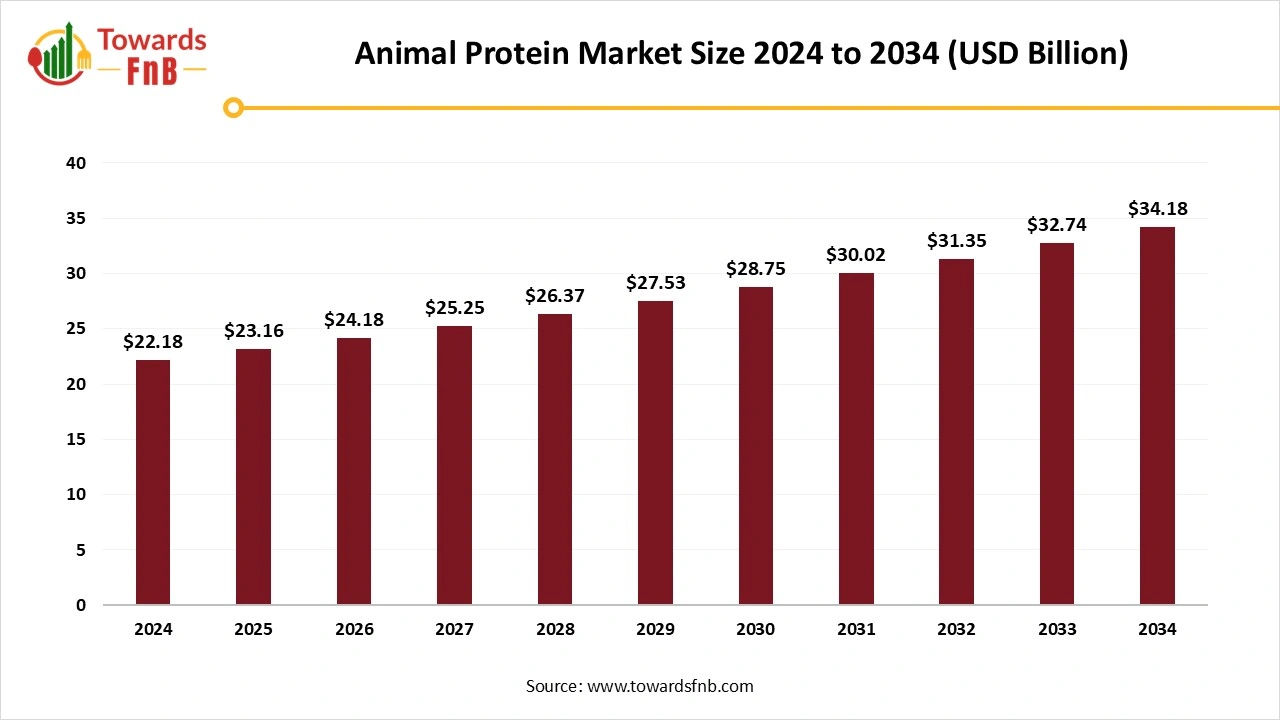

The global animal protein market size was reached at USD 22.18 billion in 2024 and is anticipated to increase from USD 23.16 billion in 2025 to an estimated USD 34.18 billion by 2034, witnessing a CAGR of 4.42% during the forecast period from 2025 to 2034. The market remains a cornerstone a global nutrition, meeting rising demand for high-quality protein through meat, poultry, dairy, eggs, and seafood.

| Study Coverage | Details |

| Growth Rate from 2025 to 2034 | CAGR of 4.42% |

| Market Size in 2025 | USD 23.16 Billion |

| Market Size in 2026 | USD 24.18 Billion |

| Market Size by 2034 | USD 34.18 Billion |

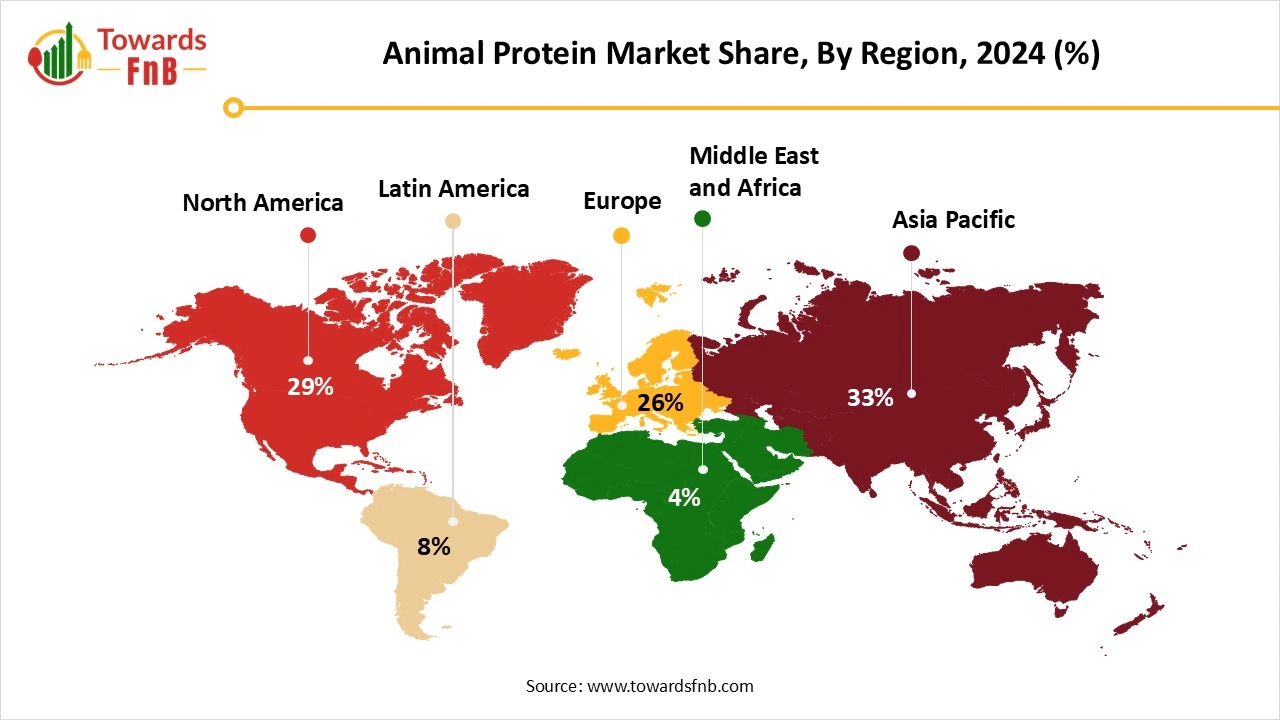

| Largest Market | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The animal protein market refers to the global industry engaged in the production, processing, and commercialization of protein derived from animal sources. This includes protein sourced from meat, poultry, dairy, eggs, fish, and insects, and is used for human consumption, animal feed, and industrial applications (e.g., pharmaceuticals, cosmetics). The market also includes functional and processed protein ingredients like hydrolysates, concentrates, and isolates.

The market is experiencing consistent growth, driven by rising global meat consumption growth, driven by rising global meat consumption and growing middle-class populations, particularly in Asia and Africa. Poultry remains the most consumed meat type due to its affordability and shorter production cycles, while demand for high-end proteins like beef and seafood is expanding in premium markets. The market also sees increasing diversification, with value-added and organic animal protein products gaining traction. Export markets are booming, especially for countries with a strong animal husbandry sector.

Emerging economies present a vast opportunity for growth in the animal protein market. Rapid urbanization, rising disposable incomes, and evolving food habits are creating new consumer bases for meat, dairy, and eggs. Companies entering these markets with affordable, locally adapted protein products can gain first-move advantages. Investment in local processing facilities and cold storage infrastructure is enhancing distribution capacity. Demand for protein-rich infant and elderly nutrition is also expanding the market scope. With the right strategies, businesses can tap into these underrepresented regions to drive long-term growth.

Despite strong demand, the animal protein market faces key challenges around sustainability, environmental impact, and shifting consumer perceptions. Concerns over greenhouse gas emissions, land use, and water consumption are putting pressure on producers to adopt greener practices. The rise of plant-based and cultured meat alternatives is based and cultured meat alternatives is intensifying competition, especially among environmentally conscious consumers.

Disease outbreaks such as avian flu or African swine fever can severely disrupt supply chains and reduce consumers' confidence. Regulatory hurdles and trade disputes further complicate global market stability. To stay competitive, industry players must innovate while responding transparently to sustainability and health concerns.

Why is Aisa Pacific the Animal Protein Powerhouse of Today?

Asia Pacific dominated the market in 2024, driven by its vast population, rising incomes, and shifting dietary preferences. The region accounts for a significant portion of global meat, dairy, and seafood consumption, especially in countries like China, India, Indonesia, and Vietnam. Rapid urbanization has increased the demand for packaged and processed protein products. Government initiatives supporting livestock modernization and cold-chain development are enhancing supply capabilities. As traditional diets evolve to include more protein-rich foods, poultry and fish consumption are particularly surging. The combination of strong demand and improving infrastructure continues to anchor Asia-Pacific as the dominant market.

")

India is emerging as the key player in Asia pacific, especially among urban and health-conscious consumers. Poultry and dairy remain the primary protein sources, with eggs and fish gaining popularity. Growth is supported by expanding retail networks, foodservice penetration, and government support for animal husbandry. However, regional dietary diversity and cultural preferences still shape market dynamics. With a young population and increasing focus on nutrition, India’s role in the animal protein market is set to become even more significant.

How North America is a Fast-Moving Frontier for Animal Protein Innovation?

North America expects the fastest growth in the animal protein market during the forecast period, supported by a high-protein dietary culture and innovation-driven production systems. Consumer demand for leaner, antibiotic-free, and organic meat and dairy products is rising sharply. Advanced animal genetics, feed optimization, and AI-driven farm management are pushing productivity to new levels. The region also benefits from a robust cold-chain infrastructure and high consumption of processed and ready-to-eat protein foods. Exports from North America, especially beef and poultry, are growing steadily in Asia and the Middle East. While mature in some segments, the market’s evolution toward premiumization and sustainability is driving its fast-paced growth.

The U.S. represents the key player in North America, with consistently high per capita meat consumption. Consumers are shifting toward grass-fed, hormone-free, and ethically raised animal proteins. Retailers and foodservice chains are expanding premium and clean-label offerings to meet changing preferences. Technological adoption in farming and processing ensures high efficiency and supply resilience. With a growing focus on health, wellness, and sustainability, the U.S. market is rapidly diversifying while remaining highly influential.

Why Poultry Protein is Dominating The Animal Protein Market?

Poultry protein segment dominated the market in 2024, due to its affordability, accessibility, and widespread cultural acceptance. Compared to red meats, poultry has a shorter production cycle and requires fewer resources, making it cost-effective for producers. Health-conscious consumers favor chicken and eggs for their lean profile and high-quality amino acid content. The rise of quick-service restaurants and ready-to-cook meals has further accelerated poultry demand. Nations like the U.S., China, and Brazil are global leaders in poultry production and exports. In both developed and emerging economies, poultry remains the top choice for animal-based protein.

The poultry segment is also witnessing rapid innovation in packaging, processing, and enrichment. Antibiotic-free, organic, and free-range poultry products are gaining popularity among conscious consumers. Technological advancements in hatchery automation and disease control are improving yield and animal welfare. As flexitarian diets grow, poultry stands out as a compromise between meat lovers and health seekers. The wide culinary adaptability of poultry across cultures further boosts its dominance. Overall, poultry remains a highly scalable and consumer-favored protein source.

The Insect Protein Segment Expects the Fastest Growth in the Animal Protein Market During the Forecast Period.

Driven by its sustainability, nutrient density, and low environmental footprint. Crickets, mealworms, and black soldier flies are being farmed at scale for both human consumption and animal feed. With growing environmental concerns, insects offer an efficient alternative, requiring less land, water, and feed compared to traditional livestock. High in protein, fiber, and micronutrients, insect-based powders are finding their way into protein bars, snacks, and supplements. Regulatory bodies in Europe and Asia are increasingly approving insect-based ingredients for commercial use. As stigma fades, consumer curiosity and acceptance are steadily rising.

Insects are also gaining attention in pet food and aquaculture, where sustainability and hypoallergenic traits are valued. Large companies and startups alike are investing in vertical insect farming and automation technologies. In Asia-Pacific and Africa, where entomophagy has cultural roots, market penetration is growing even faster. Government and academic support is helping establish standards and safety regulations. Educational campaigns and influencer-led promotions are helping shift consumer perception. With climate resilience and resource efficiency, insect protein is positioned as a future-forward protein revolution.

Why Solid Segment is Leading The Animal Protein Market?

Solid protein segment dominated the market in 2024, due to its widespread use in meat, dairy, and egg-based food products. From whole cuts of meat to cheese and powdered eggs, solids offer longer shelf life, ease of handling, and culinary flexibility. They are widely distributed through retail, foodservice, and industrial channels, making them accessible across consumer tiers. Solid protein formats also allow for value addition such as seasoning, marination, or dehydration. Consumers often associate solid forms with authenticity and freshness. This format remains central to traditional eating habits across cultures.

In industrial applications, solids like casein, whey powder, and meat meals are used in protein-enriched snacks and formulations. The versatility of solid proteins makes them a staple in sports nutrition and baking industry. Processed cheese, jerky, and protein bars rely on solid forms for texture and stability. Packaged solid proteins have grown post-COVID, as consumers stock longer-lasting essentials. Retailers also favor solids for attractive merchandising and reduced spoilage risk. Solid form remains the most practical and profitable format for producers and consumers alike.

The Liquid Segment Expects the Fastest Growth in the Animal Protein Market During the Forecast Period.

Driven by convenience, portability, and formulation ease. Products like protein shakes, drinkable yogurts, and bone broths are becoming popular among busy consumers and fitness enthusiasts. Liquid protein enables faster absorption and is ideal for clinical, elderly, or recovery-based nutrition. It also supports innovation in ready-to-drink (RTD) and meal replacement markets. Advancements in emulsification and UHT processing are improving shelf life and flavor. Brands are launching fortified and flavored options to appeal to broader demographics.

Liquid proteins are also penetrating specialty categories like prenatal supplements and pediatric nutrition. The growth of e-commerce and personalized nutrition is boosting demand for subscription-based liquid protein kits. Foodservice outlets now offer protein-rich beverages as part of functional menus. As demand grows for on-the-go nutrition, liquid forms offer a perfect blend of health, speed, and taste. Emerging regions are also embracing liquid dairy and protein beverages as household staples. This format is fast becoming a staple in well-oriented lifestyles.

Why Processed Segment is Dominating The Animal Protein Market?

The processed segment dominated the market in 2024, due to lifestyle shift toward convenience, shelf stability, and time-saving solutions. From sausages and deli meats to cheese slices and protein powders, processing enhances usability and variety. Food manufacturers rely on processing to create consistent textures, flavors, and nutrient profiles. It also ensures safety by eliminating pathogens through heat or chemical treatments. The rise of ready-to-eat and frozen food further accelerates demand for processed protein. With longer shelf lives and greater customizability, processed formats remain highly favored.

Urbanization and dual-income households are driving processed protein consumption, especially in developing economies. Modern retail channels emphasize processed formats for better packaging and portioning. Innovations in processing, such as sous vide, fermentation, and smoke infusion, are elevating flavor and nutrition. Clean-label and low-sodium processed meats are expanding choices for health-conscious buyers. Industrial users also depend on processed proteins for consistent input in bakery, snack, and functional food formulations. Processed protein is no longer just practical, it is evolving to be premium and personalized.

The Protein Ingredients Segment Expects the Fastest Growth in the Animal Protein Market During the Forecast Period.

Due to their role in functional foods, supplements, and fortified products. Isolates, concentrates, and hydrolysates from whey, casein, egg, or meat are being integrated into health beverages, bakery goods, infant formulas, and clinical nutrition. The ingredient format allows for flexible dosing and seamless mixing into various matrices. Their high digestibility and targeted amino acid profiles make them ideal for performance and medical nutrition. Food and beverage companies increasingly use protein ingredients to meet clean-label, high-protein demands. The market is also expanding into sports nutrition and personalized dietary products.

As consumers seek protein-enriched food beyond traditional meals, ingredients offer limitless formulation possibilities. Ingredient-grade proteins also enjoy regulatory clarity and consistent supply. R&D investment is driving innovations like microencapsulation and flavor masking. The trend of "protein fortification" is expanding from beverages to breakfast cereals, snacks, and soups. As industry shifts from volume to functionality, protein ingredients are becoming a strategic growth engine. These ingredients allow manufacturers to adapt to evolving consumer health trends with speed and precision.

Why Food And Beverages Is Dominating the Animal Protein Market?

The food and beverages segment dominated the market in 2024, due to its versatility and sugar-like taste. It is being widely used in baked goods, snacks, beverages, dairy, and frozen dessert. With rising demand for sugar reduction in mainstream products, manufacturers are rapidly turning to allulose. Its ability to mimic sugar's taste and texture without calories makes it ideal for both indulgent and functional products. It’s also heat-stable, which is a big advantage in food processing. From reformulated classics to innovative launches, allulose is now a kitchen essential for many brands.

The Nutraceuticals & Dietary Supplements Segment Expects the Fastest Growth in the Market During the Forecast Period.

As consumers look for palatable options in wellness products, allulose provides sweetness without compromising health goals. It is being integrated into protein powders, meal replacement shakes, gummies, and fiber blends. Its low glycemic index aligns perfectly with blood sugar management supplements. Formulators appreciate its solubility, stability, and ability to mask the unpleasant tastes of actives. With functional nutrition booming, allulose is becoming a vital tool in supplement formulation.

How Is Human Consumption Leading The League?

The human consumption segment dominated the animal protein market in 2024, accounting for most of the meat, dairy, and egg production. From daily meals to high-performance diets, animal protein remains a key source of essential amino acids and micronutrients. Its consumption is deeply rooted to the traditions that human follow.

The Industrial Use Segment Expects the Fastest Growth in the Market During the Forecast Period.

Animal by-products such as bone meal, gelatin, and collagen are being repurposed for high-value industrial uses. Pet nutrition, especially premium and functional formulations, is driving demand for high-quality protein ingredients. In agriculture, animal proteins are used to enrich livestock feed for improved growth and immunity. Biomedical applications of collagen and gelatin are expanding in wound care, tissue engineering, and drug delivery.

Why did Direct (B2B) Segment Held The Largest Animal Protein Market Share In 2024?

The direct (B2B) segment dominated the market in 2024, due to its ability to replace sugar without affecting product quality. Major brands are reformulating everything from soft drinks to cookies to cater to health-conscious consumers. Allulose helps meet sugar-reduction targets without sacrificing flavor, making it ideal for mass-market reformulations. Its performance in texture, browning, and sweetness gives it a competitive edge over many alternatives. The global push toward low-calorie diets continue to fuel adoption in this segment. As consumer palates evolve, food and beverage applications remain the engine of demand.

The Indirect Segment Expects the Fastest Growth in the Market During the Forecast Period.

Online grocery, health stores, and specialty retailers are reshaping how consumers access animal protein products. E-commerce platforms allow niche protein formats like collagen peptides or exotic meats to reach broader audiences. Subscription-based delivery of protein kits, frozen meals, and RTD shakes is gaining traction. These channels offer convenience, variety, and personalization that resonate with modern consumers.

FDA

By Source

By Form

By Processing Level

By Application

By End User

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Animal Protein Market