April 2026

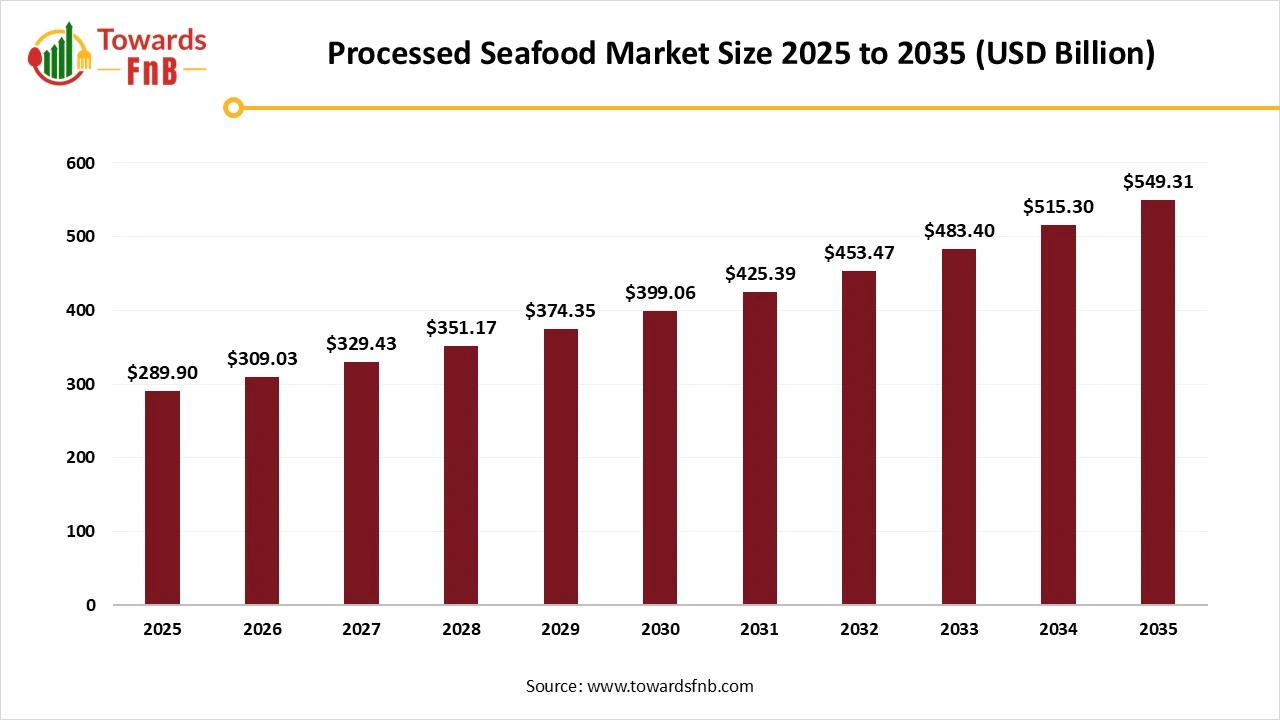

The global processed seafood market size estimated at USD 289.90 billion in 2025 and is predicted to increase from USD 309.03 billion in 2026 to nearly reaching USD 549.31 billion by 2035, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. The market is experiencing significant growth, driven by increasing demand for convenient, ready-to-eat, and healthy food options.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.6% |

| Market Size in 2026 | USD 309.03 Billion |

| Market Size in 2027 | USD 329.43 Billion |

| Market Size by 2035 | USD 549.31 Billion |

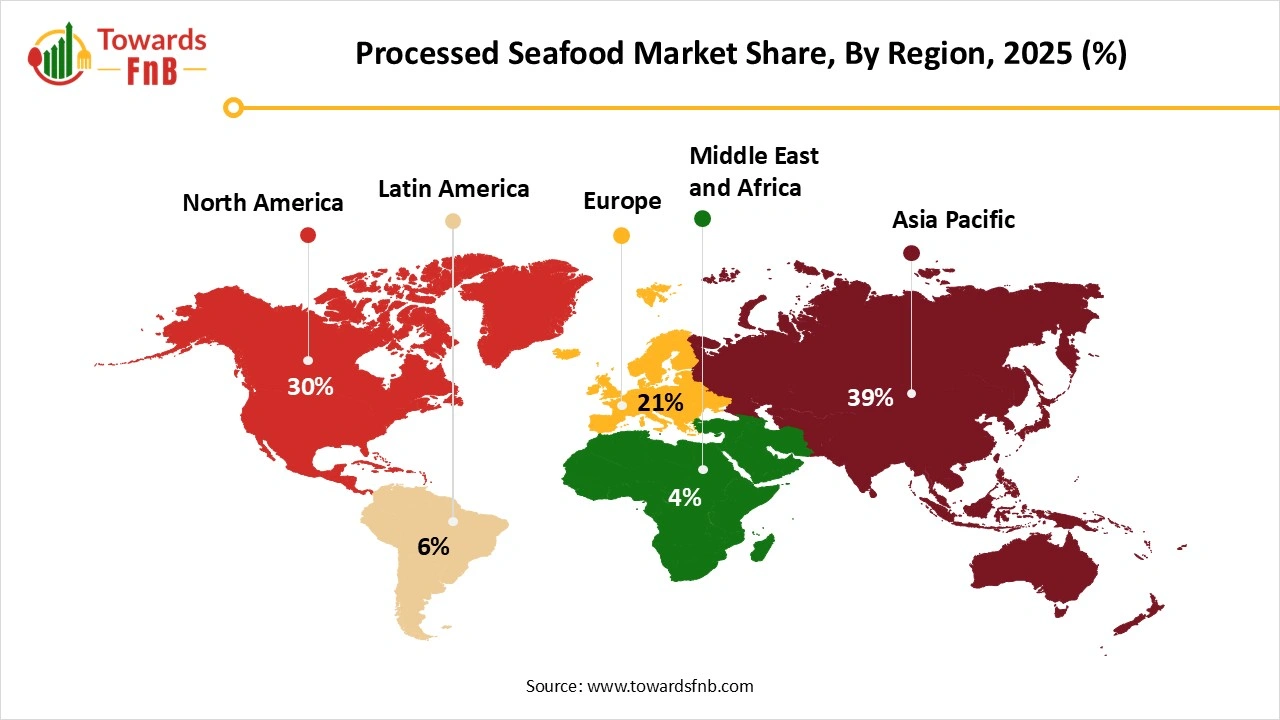

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The processed seafood market includes all fish and seafood that has been altered from its fresh state through methods like canning, freezing, smoking, drying, salting, or adding preservatives. This market is growing due to increased consumer demand for convenient, ready-to-eat, and ready-to-cook meals driven by busy lifestyles, as well as its extended shelf life and ease of storage. Products can be sold through various channels, including retail supermarkets, online stores, and food service, and include frozen, canned, and smoked varieties.

To satisfy consumer preferences for safe, minimally processed, and fresh-tasting seafood, the industry is transitioning from conventional heat-based methods to advanced techniques that more effectively maintain nutritional and sensory attributes. Innovations in processed seafood involve non-thermal techniques such as high-pressure Processing (HPP) and plasma technology for enhancing shelf-life and maintaining quality. The Fourth Industrial Revolution (Industry 4.0) has brought digital technologies that are changing supply chain management, quality assurance, and sustainability practices. Additional innovations emphasize advanced packaging technologies, including modified atmosphere and smart packaging, along with Industry 4.0 implementations like AI, robotics, and intelligent sensors for improved tracking and traceability from farm to table.

Raw Material Procurement

Processing

Packaging

Distribution

What Made the Asia Pacific Dominant Region in the Processed Seafood Market?

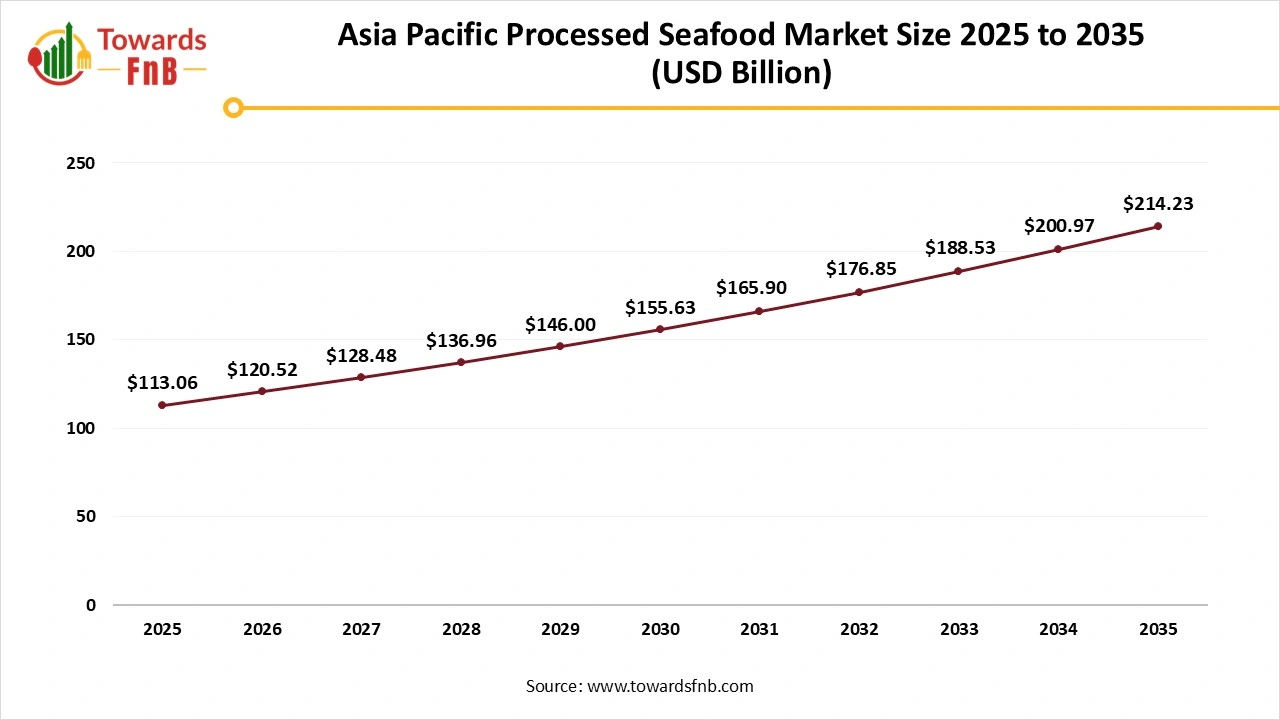

Asia Pacific dominated the market in 2025. The market in the Asia Pacific is a significant and expanding industry fueled by growing urbanization, increasing incomes of the middle class, and a demand for convenient, nutritious food choices. China plays a leading role as a significant consumer and exporter, bolstered by its robust aquaculture sector and processing skills. Important growth drivers consist of the development of cold chain facilities and the increasing demand for items such as frozen and canned seafood. The growing middle class throughout the Asia Pacific is fundamentally altering seafood consumption trends, as urban households increasingly focus on protein-rich diets and high-quality seafood options.

The Asia Pacific processed seafood market size estimated at USD 113.06 billion in 2025 and is predicted to grow from USD 120.52 billion in 2026 to nearly reaching USD 214.23 billion by 2035, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035.

China Processed Seafood Market

The expansion of China's market is mainly propelled by rising consumer interest in convenient, ready-to-eat items, driven by hectic lifestyles and urban development. Increasing disposable incomes and an expanding middle class have resulted in greater expenditure on quality and varied seafood choices. Moreover, governmental efforts encouraging sustainable fishing and aquaculture methods foster industry development. Improvements in processing technology and cold chain logistics have enhanced product quality and longevity, broadening market access.

North America Processed Seafood Market: Growth Drivers

The processed seafood market in North America has shown fastest expansion driven by a rising need for convenient, nutritious, and sustainably sourced food items. This industry has progressed due to a change in consumer habits toward healthier food selections, where seafood is viewed as a low-fat protein source abundant in Omega-3 fatty acids. The North American market, comprising the U.S. and Canada, has seen substantial expansion fueled by these elements. The increasing recognition of the health advantages of seafood and the heightened demand for ready-to-eat and frozen seafood items are key factors fueling this growth.

U.S. Processed Seafood Market

The U.S. processed seafood market is extensive and expanding, fueled by the need for protein packed, convenient, and nutritious food choices, particularly shrimp, salmon, and tuna. As the largest importer of fish and fishery products globally, the United States significantly influences aquaculture practices around the world. Main factors consist of rising consumer knowledge about the health advantages of seafood, the growth of retail and online shopping, and an increasing inclination towards sustainable and convenient meal options.

")

Europe Seafood Processing Industry: Regional Insights on Rapid Growth

The European market is a large and growing industry. This expansion is fueled by reasons such as a strong consumer inclination towards premium seafood with high protein content, a movement towards sustainable aquaculture practices, and a solid cold-chain logistics system. Active lifestyles result in an increased need for convenient, ready-to-eat, and easy-to-prepare processed seafood items. Major participants consist of Spain, France, and Portugal, with the market influenced by local production as well as substantial international commerce.

Spain Processed Seafood Market

Spain's processed seafood market is strong, fueled by elevated per capita consumption, a substantial processing sector, and significant demand for canned and frozen items. The market is the largest in Europe regarding processing, but it depends on imports to satisfy local demand. Spain imports more fish and seafood than it exports, obtaining these products from over one hundred nations globally. In 2024, Spain imported seafood products valued at $9.5 billion from various sources, an increase of nearly 3 percent compared to the prior year.

Expanding Processed Seafood Market of MEA

The processed seafood market in the Middle East and Africa (MEA) is expanding, fueled by urbanization, hectic lifestyles, and a rising need for convenience foods. Important market trends involve a transition from fresh to processed items such as canned, frozen, and smoked fish, along with the growth of contemporary retail, particularly supermarkets and hypermarkets. The market is experiencing significant growth in value-added products, bolstered by e-commerce that enhances accessibility.

UAE Processed Seafood Market

The processed seafood market in the UAE is seeing consistent expansion, fueled by rising demand for convenient and nutritious food choices stemming from population increases, tourism, and a desire for varied cuisines. The government is putting money into aquaculture and seafood production to reduce imports, but it still falls short of satisfying demand. The market is influenced by a combination of well-known local firms such as Al Islami Foods and global entities like Conagra Brands.

South America Processed Seafood Market Expansion

The expansion of the South America market is mainly fueled by rising consumer interest in convenient, ready-to-eat seafood offerings. Increasing disposable incomes and urban migration have resulted in a trend toward processed food, such as seafood, because of their convenience and extended shelf life. Improvements in technology for processing and packaging boost product quality and safety, drawing in more customers.

Brazil Processed Seafood Market

The processed seafood market in Brazil is driven by strong domestic consumption and increasing exports, particularly of farmed tilapia. Tilapia is the most important farmed fish, accounting for over 65% of domestic production. The industry is expanding with investments in aquaculture and processing technology. A rising middle class and a growing consumer trend toward healthy, high-protein diets are increasing domestic consumption of seafood.

Processed Seafood Market Share, By Species, 2025 (%)

| Segments | Shares (%) |

| Fish | 40% |

| Molluscs | 17% |

| Tuna | 12% |

| Shrimps | 10% |

| Crabs | 8% |

| Others | 13% |

Why did the Fish Segment Dominate the Processed Seafood Market?

The fish segment led the market in 2025, because of the broad accessibility of numerous fish species, their notable health advantages especially protein and omega-3 fatty acids, the adaptability in transforming them into convenient items, and the ongoing advancements in preservation techniques. Fish are readily accessible from extensive ocean resources and a quickly growing aquaculture sector.

The Shrimps Segment is Observed to Grow at the Fastest Rate During the Forecast Period.

Attributed to strong demand fueled by health trends, a desire for convenient and versatile ingredients, and innovations in aquaculture. Shrimp is a nutrient-dense food that is low in calories and high in protein, abundant in omega-3s and other essential nutrients, which makes it a favored option for health-focused individuals. Its adaptability in cuisine, the ease of processed goods, and the increasing worldwide output capacity of shrimp farming further enhance its market supremacy.

The market is witnessing growth in the tuna segment, driven by rising consumer demand for convenient, nutritious, and protein-packed food choices. Main factors consist of the increase in value-added items such as flavored and ready-to-eat tuna, advancements in packaging like single-serve pouches, and an escalating emphasis on health-oriented diets such as weight control and high-protein schemes.

Processed Seafood Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Frozen Seafood | 50% |

| Canned Seafood | 15% |

| Smoked Seafood | 10% |

| Dried Products | 5% |

| Others | 20% |

How did the Frozen Seafood Dominate the Processed Seafood Market?

Frozen seafood segment held the dominating share of the market in 2025. Frozen seafood is increasingly popular because of its extended shelf life, flavor, availability throughout the year, and preserved nutrition in contrast to fresh options. Innovations in freezing technology, cold chain logistics, and vacuum-sealed packaging have increased the appeal of frozen seafood in retail and foodservice industries.

Canned Seafood is Seen to Grow at a Notable Rate During the Predicted Timeframe.

The growing need for convenience food is notably propelling the expansion of the canned seafood sector, mirroring larger patterns in consumer preferences and market forces. Enhanced convenience, a rise in the appetite for animal-based protein, extended shelf life, and the cost-effectiveness of these products compared to alternatives (frozen and fresh) further boost the sales of canned items.

Smoked seafood segment is growing rapidly as consumers seek healthy, convenient, and high-quality food choices. Advancements in smoking methods and packaging are improving product quality, shelf life, and attractiveness. Techniques for cold smoking, hot smoking, and hybrid methods are being enhanced for better flavor and safety.

Processed Seafood Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Supermarkets/Hypermarkets | 60% |

| Convenience Stores | 12% |

| Specialty Stores | 8% |

| Online Retail | 15% |

| Retail | 5% |

Which Distribution Channel Dominated the Processed Seafood Market?

Supermarkets/hypermarkets segment dominated the market with the largest share in 2025, attributable to their convenience, extensive product range, ideal locations, and marketing efforts. They provide a comprehensive shopping experience for various groceries, featuring a wide range of processed seafood choices such as frozen, canned, and ready-to-cook items, accommodating different consumer preferences and hectic lifestyles. These retailers additionally utilize their extensive customer bases through in-store promotions, discounts, and sampling to boost sales.

Online Retail Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period.

Due to convenience, driven by convenience, home delivery, and a broader range of options that attract busy shoppers and individuals residing far from brick-and-mortar stores. The COVID-19 pandemic hastened this transition, and digital platforms have consistently fulfilled consumer needs for diversity, convenience, and thorough product details. The increase of strong cold-chain logistics and online payment systems additionally bolsters the expansion of this segment.

The specialty store segment is growing in the market as consumers seek convenient, healthy, and high-quality food choices offered by these retailers. Specialty shops respond to the need for premium, convenient, and enhanced products, and their concentration on particular niches helps them stand out from bigger retailers.

Prime Shrimp

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches/Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses/Risks

Opportunities

Threats

Recent News & Strategic Updates

By Species

By Product

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Processed Seafood Market