April 2026

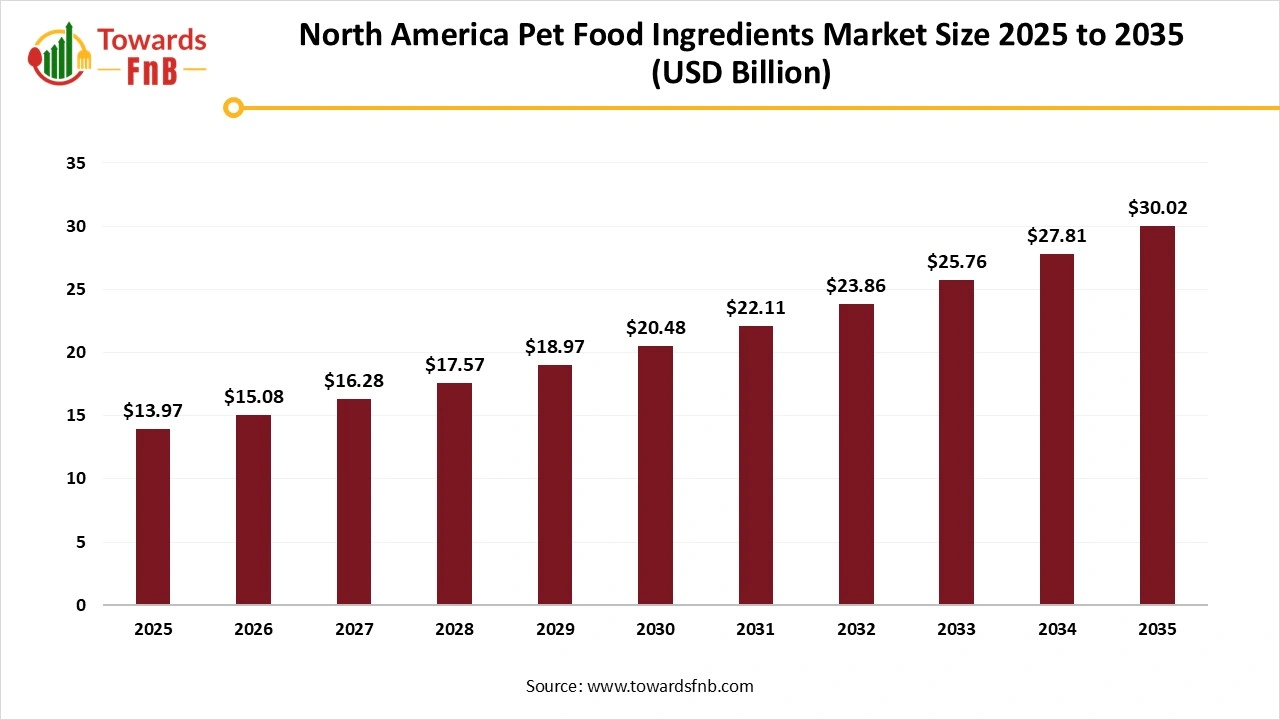

The North America pet food ingredients market size reached at USD 13.97 billion in 2025 and is predicted to increase from USD 15.08 billion in 2026 to nearly reaching USD 30.02 billion by 2035, growing at a CAGR of 7.95% during the forecast period from 2026 to 2035. The market is driven by increasing preference towards natural ingredients as pet owners focus on wellness and health for their pets.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 7.95% |

| Market Size in 2026 | USD 15.08 Billion |

| Market Size in 2027 | USD 16.28 Billion |

| Market Size by 2035 | USD 30.02 Billion |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

North America pet food ingredients market is experiencing major growth driven by increasing consumer awareness towards pet health and wellness and consumer preferences towards pet nutrition. Pet owners are seeking high-quality ingredients and becoming more discerning that enhance health and wellness for their animals. As consumers focus on transparency in production and sourcing, this trend is reflected in the increasing demand for organic and natural components. In addition, these trends show an increasing and dynamic landscape for the pet food market, driven by a focus on sustainability, safety, and quality.

North America pet food ingredients market is also driven by factors such as increasing health trends and pet ownership rates, increasing consumer focus on sustainability, increasing demand for transparency in ingredient sourcing in product formulations, increasing consumer shift towards natural ingredients, increasing consumer trend towards health and wellness and increasing demand for dietary preferences. In addition, increasing demand for protein-rich, grain-free and organic ingredients, increasing regulatory standards and increasing awareness of pet nutrition and health are further expected to drive the pet food ingredients market in North America.

The technological advancements in the pet food ingredients industry in North America are enhancing production efficiency, palatability and nutrition through innovations such as novel sustainable ingredients, advanced processing methods and AI-driven formulation. Major areas of progress such as improving ingredient processing via methods such as extrusion and freeze-drying, developing new protein sources such as plant-based proteins and cultivated meat and using AI to predict recipe compositions. These technologies allow the creation of clean-label, functional and personalized products to meet increasing pet owner demands, further revolutionize the growth of the pet food ingredients market in North America.

Raw Material Procurement

Packaging and Branding

Waste Management and Recycling

| Country | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| India | Food Safety and Standards Authority of India (FSSAI) | Food Safety and Standards (Packaging and Safety Regulations) and Licensing and Registration of Food Businesses) | The pet food ingredients market focuses on protein-rich and premium pet food industries, enhance pet’s health and wellness and sustainability and health and wellness. The market also focuses on consumer health, dietary supplements and functional foods due to rich nutritional profile. | Pet food ingredients are highly utilized in the natural and protein-rich food ingredients for their capacity to enhance the efficiency, consistency and quality of high-quality pet food products, to enhance consumer immune system and health and wellness. |

Why North America Revolutionizing Growth of the Pet Food Ingredients Market?

The market growth in the region is driven by factors such as increasing focus on functional ingredients such as omega fatty acids and probiotics for pet wellness, increasing focus on pet health and wellness, increasing demand for specialized, natural and premium ingredients, increasing disposable income, increasing trend towards a humanization-of-pets and increasing pet ownership. In addition, growing large number of pet food manufacturers and increasing number of millennial pet owners. The U.S. and Canada are the major countries driving the market growth in the region.

The U.S. Pet Food Ingredients Market Trends

The U.S. dominated the North America pet food ingredients market revenue in 2025. The market growth in the U.S. is driven by factors such as the increasing consumer preference towards minimally processed, fresh and human-grade foods, increasing demand for alternative and novel proteins, increasing focus on pet health, increasing humanization of pets, increasing demand for functional and premium ingredients and increasing research and development activities on ingredient formulation, processing and sourcing.

The Canadian pet food ingredients market is growing strongly, driven by rising pet ownership, premiumization, and an emphasis on clean-label, natural ingredients. Canadians increasingly demand high-quality proteins, such as locally sourced meat and novel proteins like duck or bison, along with functional additives like probiotics, omega-3s, and botanical extracts. Sustainability and ethical sourcing are central concerns, pushing manufacturers toward traceable supply chains.

North America Pet Food Ingredients Market Share, By Category, 2025 (%)

| Segments | Shares (%) |

| Conventional Ingredients | 75% |

| Rendered Ingredients | 25% |

Why Conventional Segment Dominating the North America Pet Food Ingredients Market?

The conventional segment dominated the market revenue in 2025. Conventional ingredients provide major benefits such as, essential nutrients and protein for organ function, immune system and muscle, which may enhance overall pet health. They also provide high effective and cost-effectiveness at creating palatable and balanced food with improved shelf life and texture. These ingredients are processed into the highly used fats, vegetables, cereals and meats found in various pet food. In addition, conventional ingredients contribute to a pet's health and wellness, leading to major advantages such as improved cognitive function, good energy levels and healthy coat in older pets, further increase the demand for conventional ingredients in North America.

The Rendered Ingredients Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in North America pet food ingredients market is driven by various benefits such as essential nutrients such as phosphorus and calcium at a low cost, concentrated, high-quality protein, enhance pet health and development, reducing the need for water and land and reducing waste to landfills. Rendered products such as poultry meal and meat meal are high in protein, which is crucial for tissue and muscle development, pet health and immune function. In addition, rendered ingredients make pet food more affordable for consumers, and offer a stable and concentrated of nutrients at a low cost, further drive the market growth in North America.

North America Pet Food Ingredients Market Share, By Ingredient, 2025 (%)

| Segments | Shares (%) |

| ADX | 80% |

| Antimicrobials | 20% |

How is ADX Segment Dominating the North America Pet Food Ingredients Market?

The ADX segment dominated the market revenue in 2025. The segment growth in the global market is driven by various benefits such as preserve nutritional value in pet food, extend shelf life, prevent oxidation, increasing demand for premium, clean-label and natural pet food, improved performance and efficacy, maintain nutritional value and prevent spoilage. In addition, leading to its major market position, its huge acceptance stem from continuous consumer reliance and trust on nutritional adequacy.

The Antimicrobials Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in North America pet food ingredients market is driven by factors such as rising development of new antimicrobial compounds, increasing awareness of pet food safety, extended shelf life, increasing need to prevent spoilage, increasing demand for preservative-rich and safer products, increasing pet ownership, increasing spending on pet healthcare, rising technological advancements and increasing concern about antibiotic resistance.

North America Pet Food Ingredients Market Share, By Use Case, 2025 (%)

| Segments | Shares (%) |

| Dog Food | 60% |

| Cat Food | 30% |

| Fish Food | 10% |

What Factors Help Dog Food Segment to Grow in 2025?

The dog food segment dominated the North America pet food ingredients market in 2025. The segment growth in the global market is driven by factors such as the increasing focus on pet’s gut health, increasing awareness of pet health, growing e-commerce platforms, increasing disposable incomes, increasing demand for functional, natural and high-quality ingredients, increasing humanization of pets and pet ownership, increasing awareness of health and nutrition, increasing focus on specialized ingredients and rising technological advancements in food manufacturing.

The Cat Food Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in the market is driven by factors such as increasing demand for cat food and its ingredients, growing numbers of cat adoptions across the globe, increasing demand for specialized, premium and high-quality food, increasing greater focus on pet premiumization and health, rise in cat ownership, increasing pet humanization of pets and increasing demand for specialized and functional ingredients that support specific health goals, including long-term well-being, digestion and immunity.

The fish food segment is expected to grow at a notable rate during the forecast period. The segment growth in the pet food ingredients in North America is attributed to the factors such as increasing demand for natural and sustainable products, increasing high nutritional value of fish ingredients, increasing focus on pet nutrition and health, increasing consumer trend towards humanization, rising awareness of nutritional benefits, increasing demand for functional and specialized diets and expansion of online retail channels and e-commerce platforms.

Why is Direct Segment Dominating the Pet Food Ingredients Market?

The direct channels segment dominated the market in 2025. Direct channels segment in the pet food ingredients offer benefits such as the ability to offer high levels of customization, direct consumer engagement and greater control over product formulation and pricing. This model allows brands to leverage convenient delivery options such as subscription services, respond directly to their needs for personalized and high-quality nutrition and build stronger relationships with consumers. Direct channels give brands full control over branding, product quality and pricing. Manufacturers can optimize inventory management and streamline their supply chain, by cutting out intermediaries, further expected to drive the market growth.

The Indirect Segment is Expected to Grow Fastest During the Forecast Period

The market growth in the North America pet food ingredients market driven by factors such as enhanced focus on major competencies such as ingredient innovation and production, lower upfront costs by avoiding the need for direct sales infrastructure and expanded market reach through intermediaries networks. In addition, intermediaries can handle sales and logistics efficiently and provide valuable local market expertise. Manufacturers can connect with a diverse and larger consumer base, by leveraging retailers, wholesalers and other partners.

Charm

Health ingredients provider IFF

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches / Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

Recent News & Strategic Updates

By Category

By Ingredient

By Use Case

By Distribution Channel

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

North America Pet Food Ingredients Market