April 2026

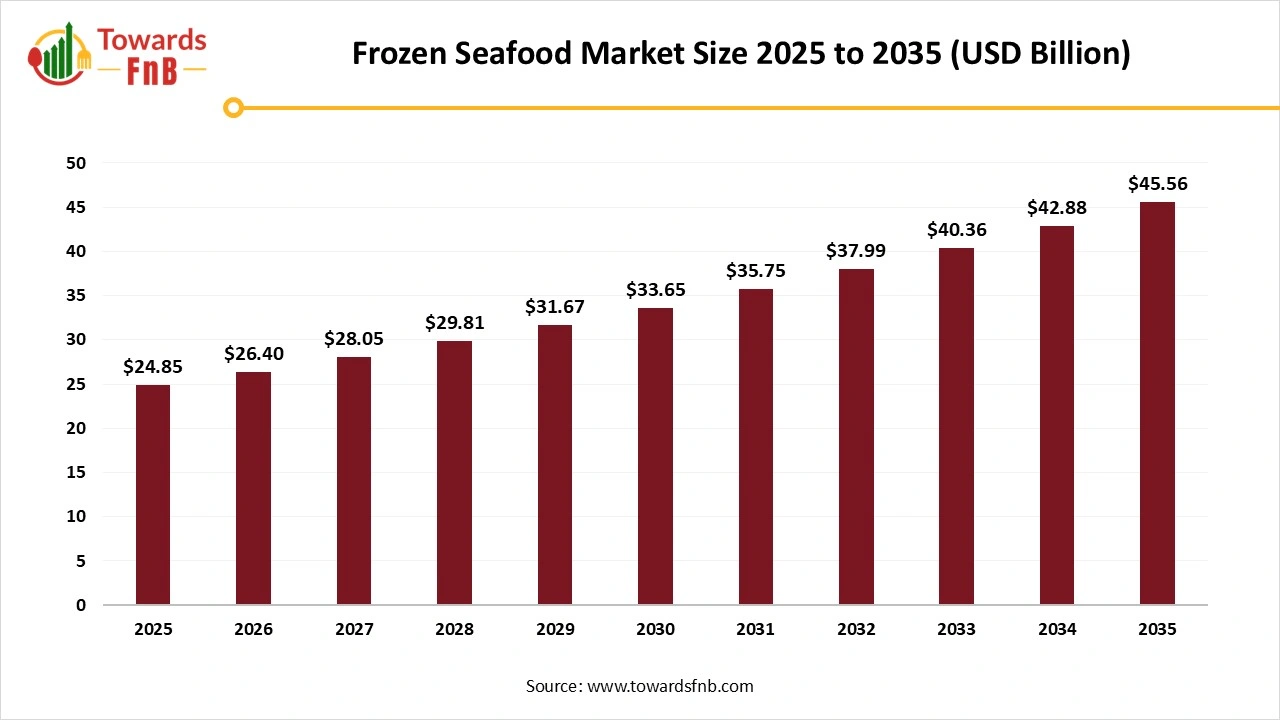

The global frozen seafood market size estimated at USD 24.85 billion in 2025 and is predicted to increase from USD 26.40 billion in 2026 to nearly reaching USD 45.56 billion by 2035, growing at a CAGR of 6.25% during the forecast period from 2026 to 2035. The market is driven by increased health consciousness, the demand for convenient and sustainable protein sources, and innovations in freezing and packaging.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.2% |

| Market Size in 2026 | USD 26.40 Billion |

| Market Size in 2027 | USD 28.05 Billion |

| Market Size by 2035 | USD 45.56 Billion |

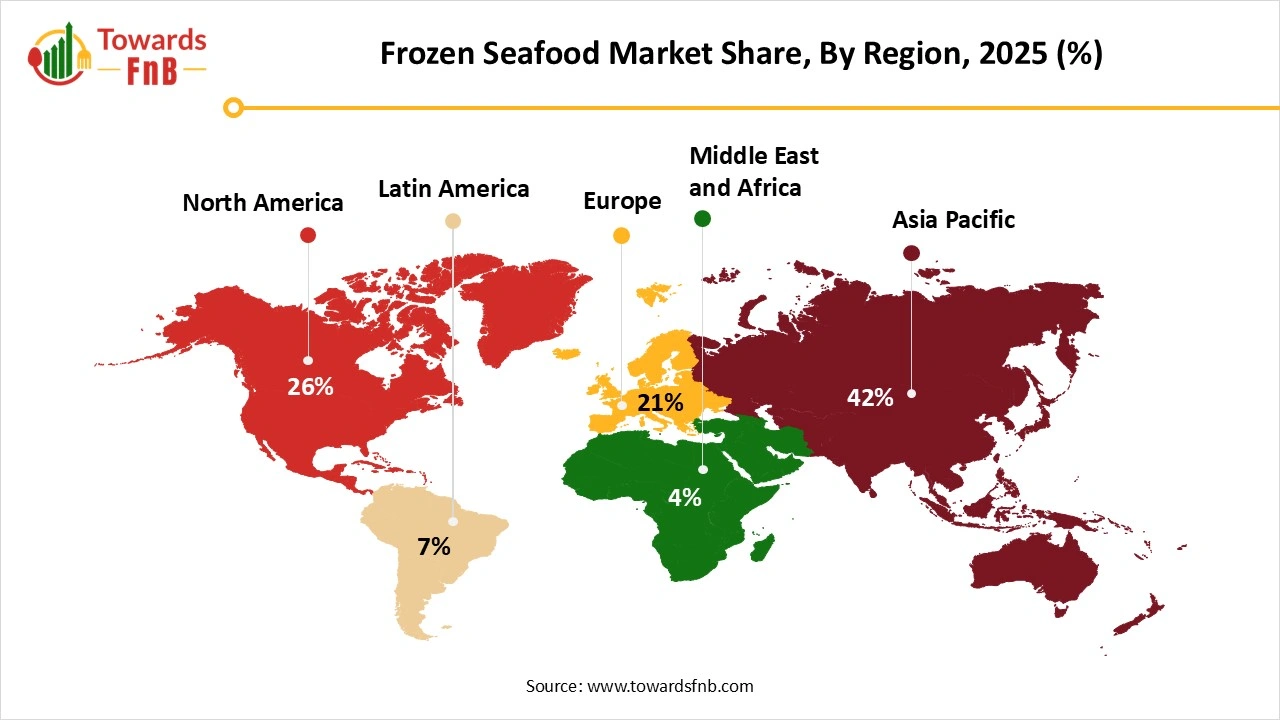

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

An important driver for market growth is the rising consumer demand for convenient, ready-to-cook protein meals. Market for seafood products preserved through freezing including fish, shrimp, crab, lobster, mollusks, and processed seafood products. It covers catching, processing, freezing, packaging, distribution, and retail across supermarkets, food service, and e-commerce, driven by rising seafood consumption, convenience, longer shelf-life, and global cold chain expansion.

Recent developments in fish freezing and cold chain technologies have significantly enhanced the retention of quality, safety, and nutritional value in seafood. Conventional methods for assessing freshness tend to be invasive and require considerable time, whereas advanced sensor technologies now allow for non-invasive, real-time tracking of spoilage markers like volatile compounds and biochemical alterations. This review emphasizes advanced freezing techniques such as Individually Quick Freezing (IQF), super-chilling, cryogenic, and ultrasound-assisted freezing, which improve texture, minimize nutrient loss, and prolong shelf life. Moreover, intelligent sensors, IoT systems, and enhanced packaging are revolutionizing cold chain logistics through better traceability and quality management.

Market potential exists in the premium frozen seafood sector, featuring organic-approved, wild-caught, and pre-marinated options. In South Korea, Spain, and China, consumers desire frozen gourmet and exotic seafood options. Items like sushi-grade tuna or marinated octopus, eel, and tapas-style shellfish, which mimic dining experiences at restaurants in a home setting, are highly sought after. Shoppers are more inclined to invest in premium, innovative goods and are seeking out diverse dining experiences. Market companies need to concentrate on tackling these consumer views via focused marketing and product development to take advantage of the increasing demand for convenience and grow their market share.

The frozen seafood market encounters specific obstacles regarding adequate cold storage facilities and transportation infrastructure in numerous developing and underdeveloped nations globally. Insufficient cold storage and transportation systems could hinder the continued expansion of the market. Insufficient cold storage and transport capabilities at retail can exacerbate seafood waste, particularly in developing countries like those in South and Southeast Asia.

Raw Material Procurement

Processing of Frozen Seafood

Packaging of Frozen Seafood

Logistic and Distribution

| Country/Region | Primary Regulatory Authority | Key Regulations and Standards |

| United States | Food and Drug Administration (FDA) National Oceanic and Atmospheric Administration (NOAA) |

Hazard Analysis and Critical Control Point (HACCP): Seafood importers and processors must implement HACCP plans to control hazards. Temperature Control: Retail-level storage temperature should be at or below 40°F (4.4°C). For frozen products, indefinite storage is safe, but quality can degrade over time. |

| European Union | European Commission, Directorate-General for Health and Food Safety (DG SANTE) Member State competent authorities |

Hygiene Regulations (EC) No 853/2004 and 854/2004: Establish specific hygiene rules for food of animal origin, including requirements for establishment approval, identification marking, and import controls. Temperature Control: Frozen fishery products must be maintained at a temperature of not more than -18°C during transport and storage. Short, upward fluctuations of up to 3°C are permissible. |

| Canada | Canadian Food Inspection Agency (CFIA) Health Canada |

Safe Food for Canadians Regulations (SFCR): Importers must hold a license and have a preventive control plan in place, similar to HACCP. Frozen seafood must be safe for consumption and accurately labeled. Quality and Grading: The Canadian Grade Compendium defines grading standards for various fish, such as frozen Atlantic smelts. |

| Japan | Ministry of Health, Labour and Welfare (MHLW) Ministry of Agriculture, Forestry and Fisheries (MAFF) |

Food Sanitation Act: Regulates food safety and import procedures, including standards for raw consumption seafood. Microbiological and Compositional Standards: Sets specific standards for frozen fish and shellfish intended for raw and non-raw consumption, such as limits on aerobic bacteria, E. coli, and Vibrio parahaemolyticus. Import Certification: A certificate of radioactive testing may be required for certain imports, particularly after the Fukushima disaster. |

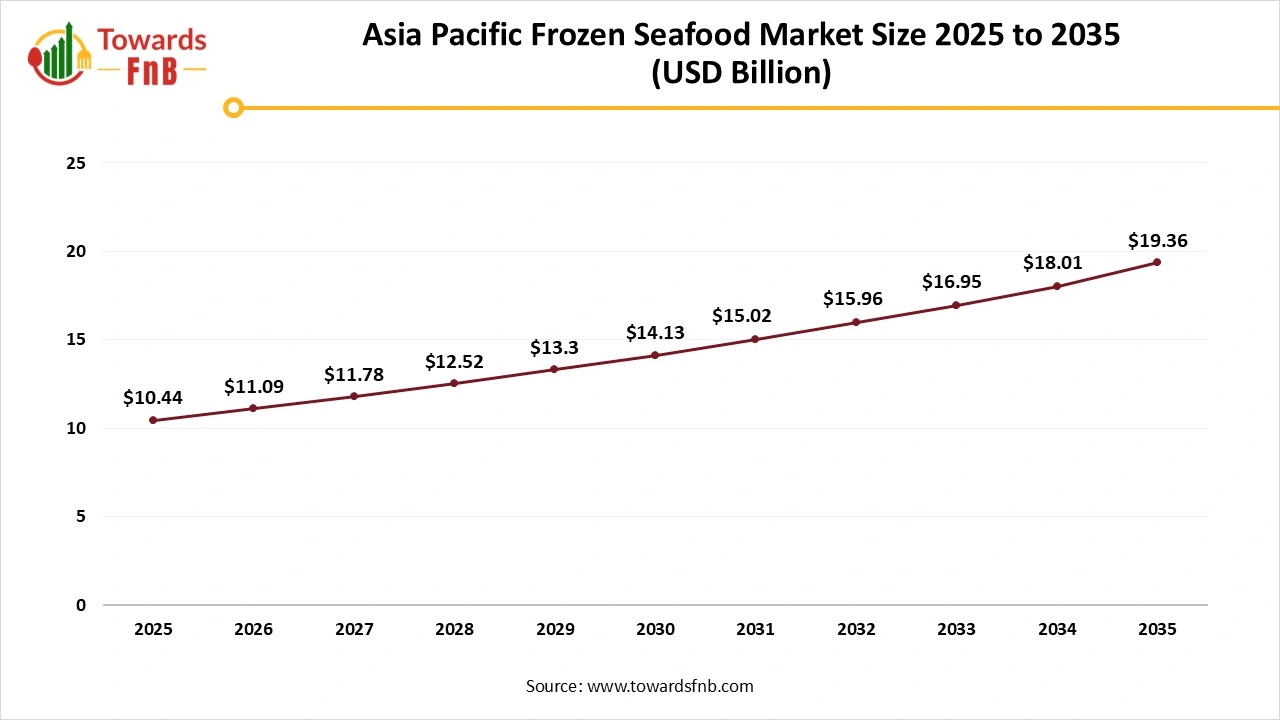

Asia Pacific Dominated the Frozen Seafood Market in 2025

Fueled by rising disposable incomes and growing aquaculture output. Government programs that enhance cold-chain infrastructure through digital economy initiatives bolster market growth potential in the area. The area is home to some of the largest seafood producers globally, such as China, Japan, and India, thanks to its extensive coastlines and rich marine resources. The significant fishing operations in these nations satisfy both local and global demand. Furthermore, this region excels in aquaculture production, catering to the significant demand for fish and shellfish. With the population increases in countries such as China and India, a larger number of people are relying on seafood products as a primary protein source. Additionally, the development of new facilities meets the seafood market's demand by boosting production capability and enhancing processing efficiency, guaranteeing a reliable supply of fresh and frozen products.

Asia Pacific Frozen Seafood Market Size 2025 to 2035

The Asia Pacific frozen seafood market size was calculated at USD 10.44 billion in 2025 with projections indicating a rise from USD 11.09 billion in 2026 to approximately USD 19.36 billion by 2035, expanding at a CAGR of 6.37% throughout the forecast period from 2026 to 2035.

China Frozen Seafood Market

By 2030, China is expected to account for 40% of the worldwide increase in seafood consumption, with a rise exceeding 5.5 million metric tons. China’s economic success, along with its population of 1.4 billion consumers and a strong preference for seafood, makes it the most promising growth market for seafood. The rise of upper-middle-class consumer segments and the growth of e-commerce platforms will lead to an increased demand for higher-value seafood over the long term. Imported frozen seafood, like shrimp, salmon, and cod, is typically less expensive and more consistently accessible throughout the year than the fresh, usually seasonal, domestic alternatives

North America Expects the Significant Growth During the Forecast Period

The rising demand for convenience food like ready-to-eat (RTE) and ready-to-cook (RTC) items, along with growing health awareness among consumers, currently serves as the primary factors propelling the frozen seafood market in North America. The RTE and RTC items decrease the cooking time and are attracting interest from individuals with fast-paced and demanding lives. The growing awareness among consumers regarding the health advantages of seafood related to heart and eye health, along with lifestyle changes, is contributing to a higher demand for these products.

")

U.S. Frozen Seafood Market

The seafood market in the U.S. is fueled by growing consumer knowledge of the health advantages, including high protein levels, omega-3 fatty acids, and vital nutrients linked to eating seafood. With the rise of health-focused eating habits, an increasing number of Americans are adding seafood to their meals. This trend is additionally driven by increasing culinary variety and the rising popularity of international cuisines that prominently include seafood. Improvements in freezing methods, including flash freezing and cryogenic freezing, have greatly enhanced the flavor, consistency, and nutritional quality of frozen food, addressing previous beliefs about them being inferior.

Frozen Seafood Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Frozen Fish | 40% |

| Frozen Shrimp & Prawns | 20% |

| Frozen Crab & Lobster | 15% |

| Frozen Mollusks | 10% |

| Ready-to-Cook / Processed Seafood | 15% |

Which Product Type Segment Dominated the Frozen Seafood Market in 2025?

Frozen fish segment led the frozen seafood market in 2025. The increasing demand for chemical-free fish with extended shelf life has driven advancements and innovations in the seafood sector. Freezing prolongs the product's shelf-life by inhibiting spoilage. Restaurants, cafes, and hotels today offer fish in different forms and preparations. The rising trend of meal kits, convenience foods, and healthy snacks drives the demand for frozen fish.

Ready-to-Cook/Processed Seafood Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Ready-to-cook seafood snacks such as dried fish, smoked salmon, and shrimp chips are gaining popularity due to their high protein levels and benefits for heart health. The increase in urban populations, along with more hectic lifestyles, is driving the need for ready-to-eat options that need little preparation. Advancements in preservation methods and flavor variety are increasing product attraction, while sustainable sourcing efforts are boosting consumer confidence.

Which Species Dominated the Frozen Seafood Market in 2025?

Shrimp/prawns segment held the dominating share of the frozen seafood market in 2025. Shrimp provides a low-fat, lean source of premium protein abundant in omega-3, fatty acids and crucial nutrients, which makes it very appealing. The increase in online shopping and cooking at home is anticipated to enhance sales of frozen shrimp. Prawn denotes a decapod crustacean that is part of the suborder Dendrobranchiata. It serves as an excellent source of vitamins, omega-3 fatty acids, protein, and minerals like zinc and selenium. Innovations in aquaculture technology and supportive trade regulations also enhance the steady global demand.

Salmon Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Fresh and frozen salmon became an important part of people's daily meals because of its distinct texture and delicious flavor. It serves as a favored nutrition source, abundant in micronutrients, minerals, marine omega-3 fatty acids, superior protein, and various vitamins, which lower the likelihood of numerous other health problems. Numerous companies experienced significant expansion in farmed salmon products worldwide.

Which Distribution Channel Segment Dominated the Frozen Seafood Market in 2025?

Supermarkets/hypermarkets segment dominated the market with the largest share in 2025. Supermarkets and hypermarkets are the primary conventional retail formats for distributing seafood, including frozen items, to customers. They offer a wide variety of frozen seafood in different types like fish, shellfish and brands, addressing various consumer tastes and requirements. Their vast networks of stores and convenient sites allow a wide range of customers to easily access frozen seafood.

Online/E-Commerce Platforms Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Driven by the ease of home delivery, a broader selection of products including niche and premium choices, and the growing inclination towards time-saving, ready-to-cook meal options. The COVID-19 pandemic expedited this transition by pushing consumers to shop online, while improvements in cold chain logistics and packaging-maintained product quality and freshness during transportation. Additionally, shoppers are more frequently purchasing online to make health-minded selections and to minimize the potential for food waste linked to fresh seafood purchases.

Frozen Seafood Market Share, By End User, 2025 (%)

| Segments | Shares (%) |

| Household Consumers | 50% |

| Foodservice / Hospitality Industry | 30% |

| Institutional Buyers | 20% |

Which End User Segment Held the Largest Share of the Frozen Seafood Market in 2025?

Household consumers segment held the largest share of the market in 2025, driven by a rising demand for convenience, health advantages, and extended shelf life. Elements like urban development, increased pace of life, heightened nutritional awareness, and the rise of e-commerce and retail stores have rendered frozen seafood a convenient, available, and favored option for home consumers, particularly due to the proliferation of ready-to-cook products. Increasing urban populations with hectic lifestyles and limited time prefer convenient food choices such as frozen seafood, making it a practical selection for everyday meals.

Foodservice/Hospitality Industry Segment is Observed to Grow at the Fastest Rate During the Forecast Period.

Due to the requirement for consistent quality, reliable pricing, and availability throughout the year, which frozen seafood meets, restaurants and hotels rely on it. Primary elements boosting this expansion encompass the strong need for convenience, particularly from fast food restaurants and catering providers, along with the rising appeal of value-added items such as pre-marinated or individually quick-frozen fillets.

Frozen Seafood Market Share, ByPackaging Type, 2025 (%)

| Segments | Shares (%) |

| Vacuum Packaged | 40% |

| Tray / Box Packaging | 25% |

| Bag Packaging | 20% |

| Bulk Packaging | 15% |

Which Packaging Type Segment Held the Largest Share of the Frozen Seafood Market in 2025?

Vacuum packaged segment dominated the market in 2025, fueled by consumer demand for extended shelf-life and premium products, as vacuum packaging prevents oxidation and microbial growth. The growth of online food delivery and e-commerce also boosts the demand for packaging that maintains product integrity during shipping. Additionally, vacuum packing prolongs the freshness and quality of seafood, reducing food waste and improving convenience for consumers, which attracts an expanding demographic focused on healthy and convenient frozen choices.

Bulk Packaging Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Driven by rising demand from foodservice and B2B customers who prioritize cost-effectiveness, longer shelf life for bulk orders, and improved efficiency in storage and transportation. Improvements in freezing methods and packaging materials guarantee quality and freshness during extended storage and shipping, while online shopping and convenience-oriented consumers also propel the market.

Young’s Seafood

Scott & Jon

Birds Eye

By Product Type

By Species

By Distribution Channel

By End-User

By Packaging Type

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Frozen Seafood Market