April 2026

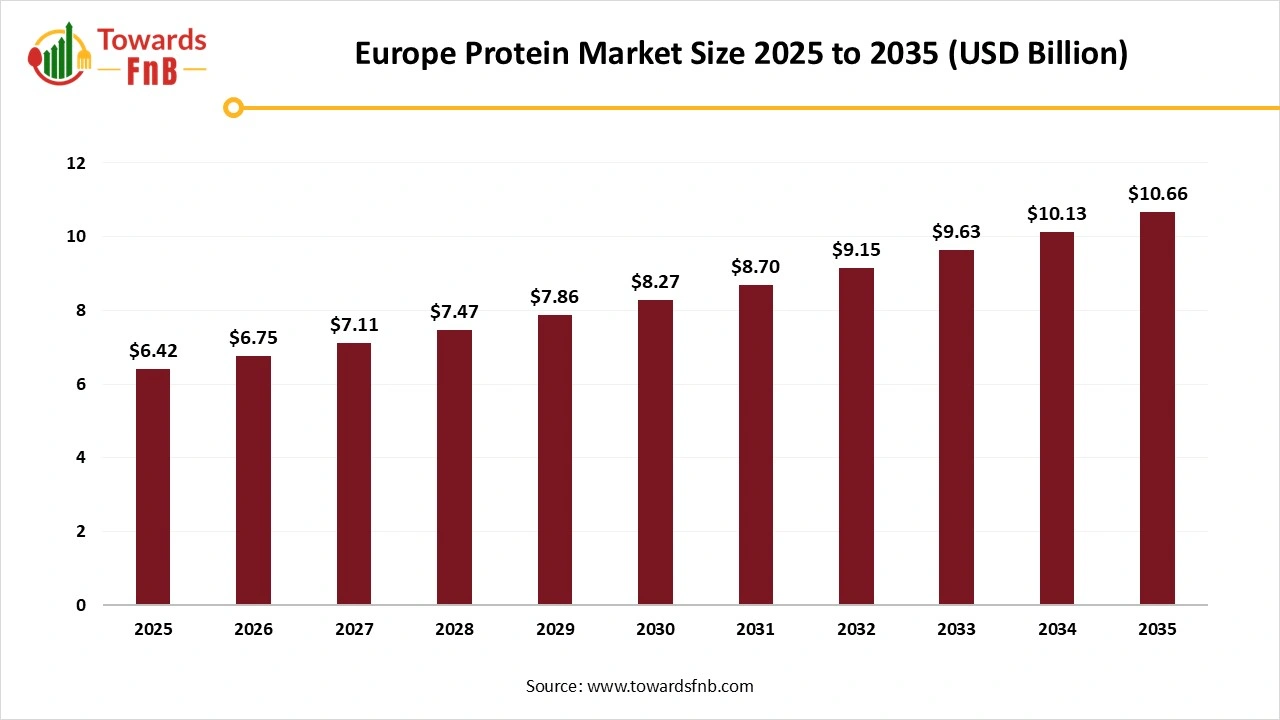

The Europe protein market size stood at USD 6.42 billion in 2025 and is expected to rise from USD 6.75 billion in 2026 to nearly reaching USD 10.66 billion by 2035, growing at a CAGR of 5.2% during the forecast period from 2026 to 2035. The market is witnessing rapid transformation, driven by shifting consumer preferences, regulatory evolution, and technological advancements. With demand rising across health, wellness, and sustainability segments, both traditional and novel protein sources.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.2% |

| Market Size in 2026 | USD 6.75 Billion |

| Market Size in 2027 | USD 7.11 Billion |

| Market Size by 2035 | USD 10.66 Billion |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The Europe protein market includes production, distribution, and consumption of various types of protein ingredients across food, beverage, dietary supplements, animal feed, and pharmaceutical applications. These proteins are derived from diverse sources including animals, plants, and emerging alternatives such as insects and microbial fermentation.

The market is driven by rising consumer awareness of health, nutrition, and fitness; increasing adoption of plant-based diets; aging populations; and demand for high-performance nutrition. Sustainability concerns, ethical food sourcing, and innovation in alternative protein are reshaping the landscape, especially under Europe's stringent regulatory and environmental frameworks.

Europe’s protein market is expanding robustly, driven by growing health consciousness, clean label demands, and plant-based trends. Traditional animal proteins remain dominant, but consumer interest in alternative and functional protein is accelerating. The market spans multiple sectors, including food and beverages, supplements, clinical nutrition, and animal feed. Regulatory support for sustainable, clinical nutrition, and animal feed. Regulatory support for sustainable protein sourcing and carbon labeling is shaping market behavior. Major carbon labeling is shaping market behavior. Major players are investing heavily in protein extraction technologies, product reformulation, and hybrid protein innovation. With a diverse consumer base and rising innovation, Europe stands as a key global protein market.

The rising emphasis on preventive healthcare and active lifestyles is a primary driver of protein consumption. Consumers are increasingly seeking foods and supplements that promote muscle growth, immune health, and weight management. The aging population is also turning to protein for maintaining muscle mass and vitality. Simultaneously, younger demographics are adopting protein-centric diets as part of fitness and beauty regimens. As protein is seen as a critical macronutrient, brands are reformulating products to include higher and better-quality protein content. This growing awareness is fueling demand across both mainstream and specialized channels.

A major growth opportunity lies in the development of next-generation alternative proteins. Fermentation-derived, insect-based, and cultivated meat proteins are drawing investor and consumer attention. Regulatory clarity in the EU is opening doors for novel protein approvals and market entry. Start-ups and food tech companies are partnering with retailers and food service giants to bring alt-protein innovations to market. With environmental concerns at the forefront, consumers are open to exploring sustainable options. Education and sensory enhancement will play a critical role in boosting adoption. Europe’s push for climate-smart nutrition positions it as a launchpad for global alt-protein expansion.

Despite growth, the market faces several challenges, especially regarding consumer trust, taste barriers, and regulatory constraints. Novel proteins like insects and lab-grown meat face resistance due to cultural perceptions and safety concerns. Strict EU regulations and labelling requirements delay the approval and commercialization of alternative proteins. High production costs of isolates and fermentation. Moreover, fragmented supply chains and raw material volatility impact pricing and product availability. Achieving taste parity with traditional proteins remains a major R&D hurdle. Addressing these challenges will require strong public-private collaboration and transparent communication.

Why Germany is Leader in the European Protein Market?

Germany dominated the Europe protein market in 2025, due to its advanced food processing industry, strong retail penetration, and health-conscious population. The country has a well-established market for dairy, meat, and emerging plant-based protein. With increasing demand for vegan and clean-label options, Germany has become a hotspot for innovation in soy, pea, and oat protein-based products. Consumer education campaigns and environmental awareness have boosted adoption of sustainable alternatives. Major food and beverage players are launching protein-fortified yogurts, snacks, and meat substitutes to cater to the evolving demand. The functional protein segment, particularly in beverages, is also gaining ground.

Innovation and policy shape leadership. Germany’s dominance is further supported by robust R&D ecosystems, government support, and collaboration with universities and startups. Regulatory transparency and food labeling standards enhance consumer trust. This rise of organic and non-GMO protein products has resonated with ethical consumer adopting high-protein diets for fitness and health. Demand is surging across age groups. Local brands are expanding exports across the EU and beyond, contributing to the country’s market strength. Germany’s continued leadership hinges on its ability to balance tradition with technological disruption.

How Northern Surge is Rising Consciousness of the Consumer?

Netherlands & Nordic Countries fastest growing in the Europe protein market in 2025, These nations are known for early adoption of sustainable food solutions and innovation in agri-tech. High consumer awareness around health, animal welfare, and climate impact is fueling the transition towards plant-based and alternative proteins. Dutch and Nordic startups are pioneering the use of fermentation, precision farming, and algae proteins. Government initiatives and favourable funding policies support protein innovation ecosystems. Export-oriented strategies are also boosting the visibility of Nordic protein brands globally.

In the Netherlands, Wageningen University acts as a key hub for protein research and development. Nordic countries are integrating circular economy principles into protein production, such as using by-products for protein extraction. Retailers are rapidly expanding shelves for protein-rich foods, from dairy alternatives to insect-based products. The surge in demand for organic, traceable proteins is reshaping supply chains. Consumers in these regions are also more open to trying novel formats like protein crisps, cultured dairy, and hybrid meats. As innovation meets sustainability, the Netherlands and Nordic regions are setting new standards for protein evolution.

Europe Protein Market Share, By Source, 2025 (%)

| Segments | Shares (%) |

| Animal-Based Proteins | 50% |

| Plant-Based Proteins | 30% |

| Alternative Proteins | 20% |

Why Animal-Based Proteins Dominate the Europe Protein Market?

Animal-based proteins dominated the market in 2025, These proteins offer complete amino acid profiles and are widely used in sports nutrition, clinical nutrition, and mainstream food applications. Their well-established safety, availability, and functional performance make them a preferred choice among manufacturers. Whey protein, in particular, remains a gold standard for absorption and muscle recovery. Dairy cooperatives and meat producers are innovating with fortified and functional protein formats. Despite sustainability concerns, animal-based proteins maintain a strong consumer base, especially among athletes and older adults.

Europe’s heritage in dairy and meat production supports continued dominance of animal protein. These products are now being reformulated to fit low-fat, organic, and grass-fed trends. Emerging high-protein dairy snacks, cold cuts, and ready meals are expanding category reach. Functional applications like protein-enriched medical foods and drinks are also seeing a rise. As clean-label expectations grow, producers are enhancing transparency in sourcing and production practices. Continued dominance will depend on balancing nutritional integrity with environmental responsibility.

The Alternative Proteins Segment Expects the Fastest Growth in the Europe Protein Market During the Forecast Period

spurred by sustainability, ethics, and innovation. Pea, soy, rice, fava bean, algae, mycoprotein, and insect-based proteins are gaining consumer and regulatory acceptance. These proteins offer eco-friendly solutions with lower carbon footprints and water usage. Advances in texture, flavor masking, and nutritional completeness are closing the gap with animal-based proteins. Startups are driving product diversity across burgers, dairy alternatives, snacks, and protein drinks. Institutional investments and public-private research partnerships are fueling rapid expansion.

Under this segment, Algae Protein if the fastest growing segment, Fermentation-derived proteins, including precision-fermented dairy, are gaining significant momentum. Insect protein is increasingly being used in sports bars, pet food, and baked goods. Educational campaigns and influencer marketing are helping normalize these novel sources. As climate concerns and flexitarian diets rise, alternative proteins are becoming central to Europe’s food transformation. The next decade will likely see them gain a strong foothold across all age groups and categories.

Europe Protein Market Share, By Product Form, 2025 (%)

| Segments | Shares (%) |

| Isolates | 45% |

| Concentrates | 40% |

| Hydrolysates | 15% |

Why do Concentrates Dominated the Europe Protein Market?

Concentrates dominated the Europe protein market in 2025, They are cost-effective, versatile, and widely used in bakery, dairy, and convenience food. Whey and plant-based concentrates are used extensively in meal replacements and fitness blends. Their natural taste and simpler processing appeal to clean-label seekers. Concentrates also meet regulatory requirements for fortification in public health nutrition programs. Brands are leveraging them in everyday products to increase protein content without altering taste or texture significantly.

The appeal of concentrates lies in their affordability and ease of integration into mass-market foods. European bakeries and dairy producers are incorporating concentrates to meet consumer protein expectations. Their mild flavor profile and good solubility make them suitable for smoothies, cereals, and yogurt. In the plant-based sector, pea and soy concentrates are widely adopted due to their functional benefits. With protein becoming a mainstream dietary expectation, concentrates remain a go-to ingredient across segments. Ongoing innovation in blend optimization ensures their continued market relevance.

The Isolates Segment Expects the Fastest Growth in the Europe Protein Market During the Forecast Period

Due to their high purity and targeted applications. These refined proteins, with 90%+ content, are used in clinical, sports, and medical nutrition where exact dosing matters. Whey, soy, and pea isolates are preferred for their rapid absorption and low allergenicity. As personalization becomes a key market theme, isolates offer better digestibility and minimal impurities. Food tech companies are also using isolates in high-protein snacks and fortified beverages. The rise in lactose intolerance and veganism is further boosting plant-based isolate demand.

Isolates are central to the premium and performance nutrition market. Athletes and aging populations seek high-efficiency proteins that support muscle maintenance and recovery. The clinical nutrition segment uses isolates for muscle wasting, diabetes management, and immune support. Startups are innovating with flavored isolates, RTD shakes, and blend formulations for specific needs. Their clean taste and functional superiority make isolates ideal for health-conscious consumers. As demand for high-protein, low-calorie solutions grows, isolates are gaining strong momentum in both B2C and B2B channels.

Europe Protein Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Food & Beverages | 50% |

| Dietary Supplements | 16% |

| Sports & Performance Nutrition | 11% |

| Animal Feed | 14% |

| Pharmaceuticals & Medical Nutrition | 9% |

How Food and Beverages is Leading the Europe Protein Market?

Food & beverages dominated the market in 2025, From protein-enriched bread and dairy to plant-based RTDs and snacks, innovation is constant. Traditional categories are being redefined with functional protein that enhance nutritional profiles. Manufacturers are reformulating products to meet EU labeling standards for high-protein claims. Protein content is becoming a key purchasing factor for health-conscious and flexitarian consumers. This segment benefits from strong retail and online distribution networks.

Protein is no longer limited to shakes and bars it’s now in soups, pasta, spreads, and even desserts. Flavor innovation and sensory enhancement have improved product appeal across age groups. Foodservice outlets are also incorporating high-protein options into menus. Hybrid protein formulations are gaining traction in bakery and frozen food. As convenience meets health trends, food and beverage applications will continue to lead growth. With consumer expectations rising, this segment will drive product differentiation across the board.

proteins also allow manufacturers to improve yield, reduce waste, and enhance sensory experience across product categories. Their natural origin supports sustainability messaging and product transparency. In beverages, hydrolyzed wheat proteins provide nutritional value without altering flavor profiles. In pasta and noodles, they offer firmness and elasticity. Functional beverages and powdered meal replacements also using wheat proteins to deliver clean energy and satiety. This sector’s volume and diversity ensure the continued dominance of food and beverage processing in wheat protein consumption.

The Sports & Performance Nutrition Segment Expects the Fastest Growth in the Europe Protein Market During the Forecast Period

Driven by lifestyle changes and the rise of recreational fitness. Consumers are embracing protein-centric products to support muscle recovery, endurance, and body toning. RTD protein drinks, recovery bars, and protein gummies are growing in popularity across genders and age groups. The inclusion of natural sweeteners, flavors, and adaptogens is enhancing appeal. Vegan and allergen-free protein blends are becoming the norm in this space. Digital fitness influencers and athlete endorsements are amplifying category demand.

The market is moving beyond professional athletes to cater to gym-goers, weekend hikers, and aging fitness enthusiasts. High-protein breakfast products and hydration-protein hybrids are also emerging. Functional protein targeting joint health, stamina, and metabolism are gaining traction. Personalized fitness nutrition kits and subscription services are booming in urban Europe. Brands are investing in science-backed formulations and clinical validation to build credibility. With fitness as a lifestyle choice, sports nutrition will remain a high-growth, innovation-rich segment.

Revo Foods

By Source

By Product Form

By Application

By Country

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Europe Protein Market