April 2026

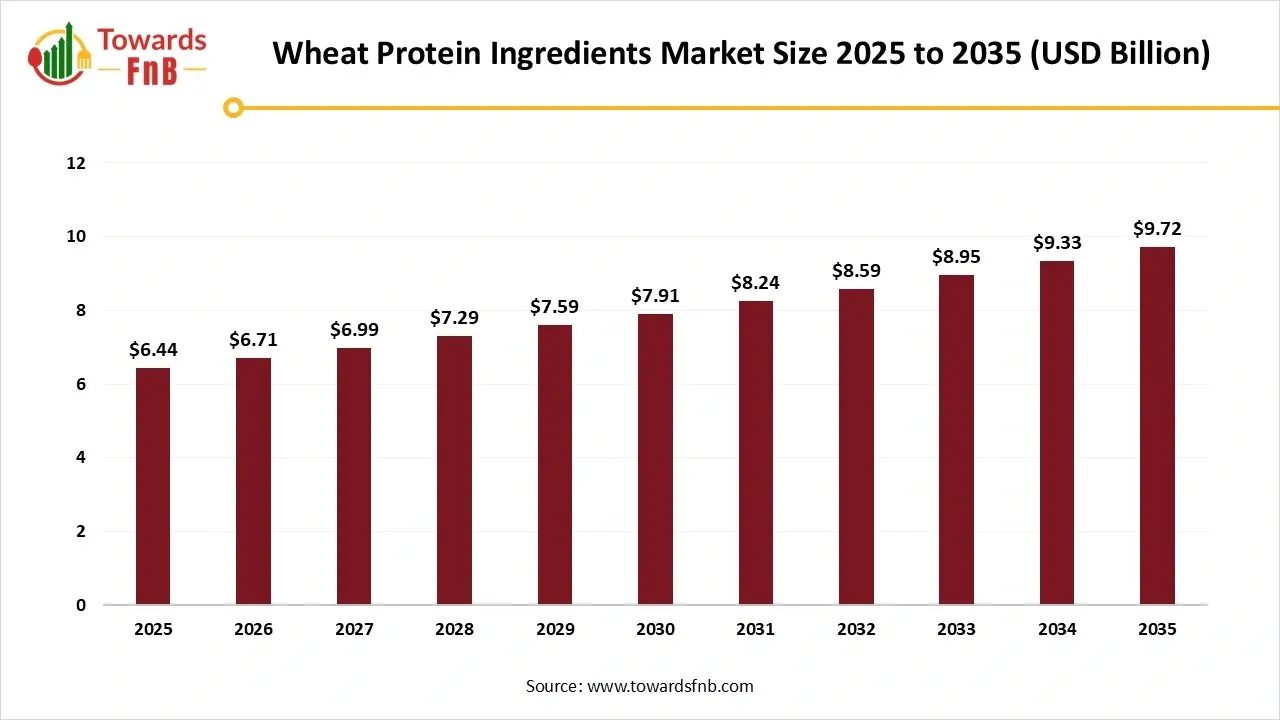

The global wheat protein ingredients market size reached at USD 6.44 billion in 2025 and is expected to rise from USD 6.71 billion in 2026 to nearly reaching USD 9.72 billion by 2035, growing at a CAGR of 4.2% during the forecast period from 2026 to 2035. The wheat protein ingredients market is rising in demand from the food, personal care, and pharmaceutical sectors. Wheat proteins are transforming from staple grain extracts into high-value functional ingredients.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 4.2% |

| Market Size in 2026 | USD 6.71 Billion |

| Market Size in 2027 | USD 6.99 Billion |

| Market Size by 2035 | USD 9.72 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Wheat protein ingredients refer to plant-based protein products derived from wheat, primarily composed of gluten, gliadin, glutenin, and albumins. These ingredients are widely used in the food & beverage industry, sports nutrition, bakery, and personal care due to their excellent viscoelastic and emulsifying properties, as well as being a functional protein alternative in vegetarian and vegan diets. The market includes both concentrated and hydrolyzed forms of wheat protein, each suited for different applications based on solubility, functionality, and end-use.

The wheat protein ingredients market is experiencing a robust surge in demand driven by evolving consumer preferences toward plant-based and allergen-conscious diets. Functional food manufacturers are turning to wheat protein isolates, concentrates, and hydrolysates for their binding, elasticity, and nutritional properties. The bakery, meat alternative, and sports nutrition sectors are among the primary adopters. Additionally, wheat proteins are increasingly being utilized in skincare formulations and pharmaceutical excipients due to their natural origin and biocompatibility.

Customer Analysis (Target Audience and Techniques To Attract Customers)

| 18-25 (Generation Z) | 30-40 age group |

| These consumers are more conscious about taste, health, and clear nutrition. Young adults are also more likely to follow flexitarian, vegan or dairy-limited diets. | These consumers go for high-protein and functional food as part of their routines. Meanwhile, families with young children and seniors are adopting caviar drinks for digestive health. |

Wheat protein ingredients hold immense untapped potential in emerging markets and alternative application sectors. Asia-Pacific, Latin America, and Middle East regions are witnessing rising awareness of clean-label, protein-rich diets. There’s growing demand in personal care and nutraceuticals for natural, plant-based actives where wheat protein fits perfectly. Technological advancements in enzymatic hydrolysis and fractionation are improving taste, solubility, and application flexibility. Additionally, regulatory moves supporting plant-based innovation are encouraging investment in wheat-based protein processing. As R&D continues to create next-gen formulations, the market is primed for expansion across sectors beyond food.

Despite its strengths, the wheat protein ingredients market faces several limitations that could hinder growth. One major restraint is its relatively lower digestibility compared to some other plant proteins, which may deter sports and clinical nutrition applications. Moreover, gluten presence in many wheat protein variants makes them unsuitable for the growing celiac and gluten-sensitive population.

Supply chain volatility in wheat farming due to climate fluctuations and geopolitical tensions can impact raw material availability and pricing. The extraction and processing technologies required are capital-intensive, creating entry barriers for smaller producers. Additionally, competition from soy, pea, and rice protein alternatives remains fierce. Overcoming these challenges will require innovation, education, and supply resilience.

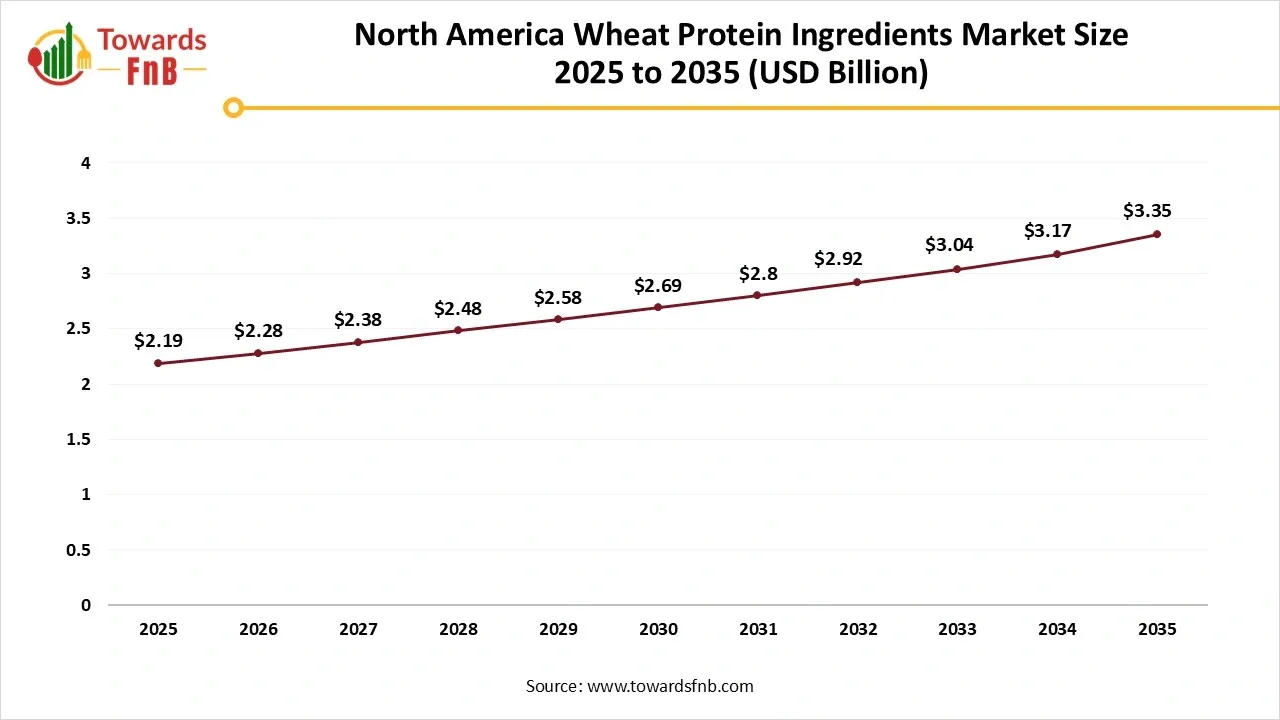

How North America is Leading With Clarity and Performance

North America dominated the market in 2025, driven by a mature health-conscious consumer base and strong demand for high-protein, low-fat foods. Major food manufacturers in the region have integrated wheat proteins into bakery goods, cereals, snacks, and vegan alternatives. The market is also supported by widespread gluten awareness and clear product labeling regulations, enabling companies to segment and target both general and niche demographics. Continuous innovation in plant-based meat and dairy alternatives adds momentum. Strong distribution channels, including retail and e-commerce, ensure product accessibility and visibility. North America's leadership is further cemented by sustained investment in clean-label ingredient development and reformulation.

North America Wheat Protein Ingredients Market Size 2025 to 2035

The North America wheat protein ingredients market size was valued at USD 2.19 billion in 2025 and is expected to rise from USD 2.28 billion in 2026 to nearly reaching USD 3.35 billion by 2035, growing at a CAGR of 4.34% during the forecast period from 2026 to 2035.

The U.S. represents the dominance in North America; it stands as the epicenter of wheat protein demand, fueled by rising health trends, fitness culture, and functional foods. American consumers are not just looking for protein; they are demanding multifunctionality, taste, and transparency. Wheat protein is widely used in high-protein pasta, baked goods, plant-based burgers, and even nutrition bars. Government support for sustainable agriculture and protein diversification also encourages adoption. With a thriving ecosystem of startups and legacy brands alike, the U.S. continues to redefine wheat protein applications. Furthermore, advancements in wheat fractionation and gluten-free processing technologies are expanding the ingredient's reach into more health-conscious subsegments.

Why Asia Pacific is Fastest Growing?

Asia Pacific expects the fastest growth in the market during the forecast period, due to rising urbanization, evolving diets, and growing disposable incomes. Consumers are increasingly aware of plant-based nutrition, especially in countries like China, India, Japan, and South Korea. The region's expanding food processing industry is adopting wheat protein for its affordability and functional properties. Moreover, beauty and personal care sectors are starting to embrace natural proteins for skincare, giving wheat derivatives new ground. Governments are promoting healthier eating habits through nutritional campaigns, indirectly favoring high-protein product formulations. With both consumer interest and industrial investment rising, Asia-Pacific is on a fast trajectory to rival Western markets.

India is emerging as the key player in Asia pacific, the market is gaining traction as consumers become more health-focused and protein-aware. Traditionally reliant on lentils and dairy for protein, urban India is now embracing packaged foods, meat substitutes, and nutritional products enriched with wheat protein. The growing middle class is driving demand for high-protein snacks, protein-rich breakfast cereals, and sports nutrition blends. India's strong wheat cultivation base offers local sourcing advantages, making wheat protein a cost-effective option for manufacturers. Personal care brands are also beginning to use hydrolyzed wheat proteins in shampoos and creams, tapping into the clean beauty trend. With regulatory support for nutraceuticals and plant-based foods, India is set to become a regional hotspot for wheat protein innovation.

")

How is the Wheat Protein Ingredients Market Growing in Europe?

Pulses, grains, and oilseeds are the main commodities widely traded and grown within Europe. The industry is a crucial staple of food and feed, which are mainly supplied by approximately generating countries and multinational companies. Organic crops and the products with the nutritional advantages that count on ancient grains have targeted specific ethnic groups, which offer perfect possibilities for medium and small-sized suppliers from developing countries.

The market dependence and size on external suppliers create a market with an attention-grabbing focus for suppliers from making countries. The European countries that offer the most possibilities with an overall scenario are Italy, Spain, the Netherlands, France, and Germany.

Trend of Wheat Protein Ingredients Market in Germany:

The users are becoming more conscious about wellness and health, concentrating on high-protein, clean-label foods and low-fat. Wheat proteins, which are rich in amino acids, serve functional health advantages, making them a preferred choice in protein-filled food and beverages. With a growing number of fitness athletes and enthusiasts, wheat protein is gaining in depth in terms of performance and sports nutrition products. It delivers an amount-effective alteration to soy and whey protein in the protein bars and powders.

Wheat Protein Ingredients Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Wheat Gluten | 38% |

| Wheat Protein Isolate | 20% |

| Textured Wheat Protein | 16% |

| Hydrolyzed Wheat Protein | 14% |

| Wheat Starch with Protein Content | 12% |

Why is Wheat Gluten the Binding Force of Functional Foods?

Wheat gluten segment dominated the wheat protein ingredients market in 2025, due to its exceptional elasticity, binding, and viscoelastic properties, making it indispensable in bakery and processed food applications. It enhances dough strength, provides chewiness, and improves moisture retention, making it a staple in breads, pastas, and imitation meats. Its widespread availability and cost-effectiveness contribute to high adoption, especially in emerging economies. Manufacturers also favor wheat gluten for its compatibility with other proteins and ease of incorporation into existing formulations. Its natural origin and clean-label appeal further bolster its position in the food processing sector. As demand for plant-based functional ingredients grows, wheat gluten continues to be the workhorse of the industry.

Beyond food, wheat gluten is also utilized in pet food, animal feed, and biodegradable packaging applications. Its high protein content and flexible processing profile make it attractive for sustainable, eco-friendly solutions. Additionally, advancements in wheat strain breeding have resulted in higher-yield, gluten-rich variants optimized for industrial use. Market players are focusing on non-GMO and organic wheat gluten production to cater to premium product segments. However, challenges around gluten sensitivity continue to prompt innovation in gluten-reduced formulations. Despite this, wheat gluten’s functional versatility secures its leading role across applications.

The Wheat Protein Isolate Segment Expects the Fastest Growth in the Market During the Forecast Period

Due to its high purity, neutral flavor, and versatile application across functional foods, sports nutrition, and clean-label products. Its refined amino acid profile and improved digestibility make it an attractive option for consumers avoiding soy or dairy proteins. It offers emulsification, film-forming, and gelling properties, enabling use in snacks, beverages, and protein bar. Increasing demand from gluten-sensitive yet non-celiac consumers is driving interest in isolates with reduced gluten content. The fitness and wellness industries are also fueling their rise due to the surge in vegan protein blends. With superior solubility and minimal aftertaste, isolates are quickly becoming a preferred choice for new product development.

Wheat Protein Ingredients Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Dry | 66% |

| Liquid | 34% |

Why did Dry Segment Dominated the Wheat Protein Ingredients Market in 2025?

Dry segment dominated the market in 2025, due to their long shelf life, ease of handling, and application flexibility. These forms are ideal for large-scale food production environments where consistency and stability are critical. Dry protein formats are widely used in bakery, pasta, snacks, and processed foods due to their stable functionality during cooking and baking. They offer manufacturers the ability to precisely dose protein content and maintain quality across production batches. Additionally, dry forms are preferred in global trade due to reduced transportation costs and extended storage viability. Their popularity spans across regions, making them a go-to format for food and beverage companies.

Furthermore, dry wheat protein’s compatibility with other plant proteins allows it to be blended seamlessly for improved texture and nutritional balance. Advances in spray-drying and microencapsulation enhancing solubility and functionality in dry formats. Powdered wheat proteins are also favored in high-protein cereals, meal replacements, and powdered sports drinks. This versatility extends to personal care applications, where dry hydrolyzed forms are used in shampoos and facial masks.

The Liquid Segment Expects the Fastest Growth in the Wheat Protein Ingredients Market During the Forecast Period

Due to its superior bioavailability, ready-to-use nature, and efficiency in manufacturing lines. It eliminates the need for rehydration or pre-mixing, making it highly appealing for convenience-driven industries. Liquid formats are increasingly used in RTD beverages, infant formulas, cosmetic emulsions, and food coatings. Their smooth texture and rapid solubility make them ideal for high-end functional foods and nutraceuticals. With fewer processing steps, liquid protein also offers environmental benefits like reduced energy usage. The demand for liquid plant-based ingredients is surging as consumers seek fast, functional nutrition.

This segment is also being boosted by innovations in enzymatic hydrolysis and cold-processing techniques that preserve protein integrity. Liquid protein is being adopted in hair care and skincare formulations due to its ability to penetrate and repair at the cellular level. In food manufacturing, it provides better dispersion in batters and sauces, enhancing consistency. Brands are also using it to create vegan egg substitutes and non-dairy creamers. As cold-chain logistics improve in emerging markets, liquid wheat protein is gaining wider accessibility. It is rapidly becoming the preferred format for high-efficiency, high-performance product formulations.

Wheat Protein Ingredients Market Share, By Concentration, 2025 (%)

| Segments | Shares (%) |

| 75–90% Protein | 52% |

| >90% Protein | 28% |

| <75% Protein | 20% |

Why do 75-90% is Dominating the Wheat Protein Ingredients Market?

75–90% segment dominated the market in 2025, due to their optimal balance of functionality, nutrition, and affordability. These concentrates retain essential amino acids while offering improved water absorption and dough conditioning. They are highly versatile in bakery, breakfast cereals, and sports nutrition segments. Manufacturers prefer them for their ease of processing, cost-efficiency, and broader regulatory approvals. They offer better solubility than gluten and provide sufficient protein density for most food applications. These traits make them ideal for both large-scale food processors and mid-sized clean-label brands.

The mid-protein range also allows compatibility with flavor systems and carbohydrate matrices in energy bars and vegan snacks. These concentrates are being used to fortify school meals, senior nutrition products, and functional beverages. In the pet food industry, they serve as digestible, protein-rich additives. Consumer trust in plant-derived mid-concentration proteins continues to rise, especially in gluten-tolerant markets. This category also seeing innovation in slow-release protein systems for athletic performance. As mass-market demand surges, 75–90% concentrates remain the most commercially viable segment.

The >90% Segment Expects the Fastest Growth in the Wheat Protein Ingredients Market During the Forecast Period

Due to high-purity isolates are sought after for their bioavailability, digestibility, and minimal carb or fat content. Their clean taste and fast absorption make them ideal for sports drinks, meal replacements, and clinical nutrition formulas. The healthcare and nutraceutical sectors are increasingly incorporating >90% wheat protein in products tailored for elderly care, metabolic support, and vegan diets. This level of concentration is also favored in premium skincare and dermatological products due to its high peptide density. As consumers demand more from every gram of protein, ultra-pure wheat proteins are becoming a symbol of efficacy.

Manufacturers are investing in specialized filtration and refinement technologies to meet the rising demand. These products are also entering premium functional food channels such as keto, paleo, and high-performance diet markets. In vegan bodybuilding supplements, >90% wheat protein rivals whey in terms of efficacy and amino profile.

Which Application Segment Dominated the Wheat Protein Ingredients Market in 2025?

Bakery & confectionery segment dominated the market in 2025, due to their structural and textural enhancing properties. Wheat proteins improve dough elasticity, shelf life, and moisture retention key traits in breads, cookies, and pastries. The segment benefits from consumer trust in wheat-based formats and long-standing culinary traditions. Confectionery products use wheat proteins for stabilizing fillings, improving chewiness, and extending shelf life in protein bars and candies. Innovation in protein-fortified baked goods is further propelling market growth. Even in gluten-sensitive markets, partial wheat protein usage remains widespread for texture and binding.

Artisanal and functional bakery brands are embracing wheat proteins to create clean-label, high-protein offerings. In premium pastries and gluten-reduced treats, it helps maintain consistency without compromising mouthfeel. With rising demand for protein-rich breakfast options, wheat proteins are becoming a key part of muffins, pancakes, and biscuits. The confectionery space is also leveraging wheat protein to meet the protein-snacking trend. Functional chocolates and nougats are adopting wheat protein hydrolysates to boost nutritional value. This application continues to evolve with hybrid innovations merging indulgence and wellness.

The Meat Analogs Segment Expects the Fastest Growth in the Market During the Forecast Period

Driven by the global shift toward plant-based diets. Wheat protein, especially gluten and isolates, replicates meat-like textures and binding properties without synthetic additives. It enables juicy, fibrous textures in plant-based sausages, burgers, and nuggets. Consumer demand for sustainable, ethical, and allergen-aware meat substitutes is at an all-time high. With wheat proteins offering umami retention and structure, they are becoming central to new product development. From flexitarians to vegans, meat analogues are finding favor across demographic lines.

Wheat Protein Ingredients Market Share, By End Use, 2025 (%)

| Segments | Shares (%) |

| Food & Beverage Processing | 58% |

| Nutraceuticals | 18% |

| Cosmetics & Personal Care | 14% |

| Animal Nutrition | 10% |

Why Food and Beverages Processing Dominate the Wheat Protein Ingredients Market?

food and beverages processing segment dominated the wheat protein ingredients market in 2025, driven by their functional performance and nutritional value. These proteins enhance texture, binding, and stability in a wide range of products from bakery to beverages. Wheat protein is a crucial ingredient in developing clean-label, allergen-aware, and plant-based foods. Its role in protein fortification has become increasingly vital as consumers demand healthier alternatives. Ready-to-eat meals, high-protein snacks, and breakfast items are utilizing wheat proteins for their mild taste and adaptability. From multinational FMCGs to local food processors, wheat proteins are a mainstay in innovative formulation.

Wheat proteins also allow manufacturers to improve yield, reduce waste, and enhance sensory experience across product categories. Their natural origin supports sustainability messaging and product transparency. In beverages, hydrolyzed wheat proteins provide nutritional value without altering flavor profiles. In pasta and noodles, they offer firmness and elasticity. Functional beverages and powdered meal replacements also using wheat proteins to deliver clean energy and satiety. This sector’s volume and diversity ensure the continued dominance of food and beverage processing in wheat protein consumption.

The Nutraceutical Surge Expects the Fastest Growth in the Market During the Forecast Period

Wheat protein isolates and hydrolysates are increasingly used in protein powders, energy drinks, and amino acid supplements aimed at muscle recovery and weight management. As consumers seek plant-based nutrition without allergens like soy or dairy, wheat protein fills a crucial gap. It offers high bioavailability and supports lean muscle mass, gut health, and metabolic functions. The clean-label movement and preference for "food-as-medicine" are accelerating demand in this space. Additionally, fortified snack bars, gummies, and sachets with wheat protein are becoming popular among health-conscious youth and seniors.

Why Direct Sales (B2B) Dominated the Wheat Protein Ingredients Market?

Direct Sales (B2B) segment dominated the wheat protein ingredients market in 2025, due to bulk purchases by food manufacturers, supplement brands, and ingredient processors. These direct channels enable tailored supply contracts, better pricing, and consistent quality assurance, which are crucial in large-scale production. Companies rely on direct sourcing to maintain traceability and meet stringent industry standards. In addition, partnerships with contract manufacturers and private label producers are fueling stable long-term agreements. The direct model supports custom formulation, co-development, and technical support services that retailers cannot match. It also provides the scale and logistics required by global and regional food conglomerates.

The Retail Sales (B2C) Expects the Fastest Growth in the Market During the Forecast Period

As protein powders, bars, and ready-to-drink formulations reach mainstream audiences, retail platforms offer easy accessibility and variety. Consumers are exploring wheat protein products for fitness, lifestyle, and dietary preferences, often via health-focused retail chains or online stores. With clearer product labeling and transparent ingredient sourcing, trust in wheat protein is growing rapidly at the consumer level. E-commerce has amplified reach with D2C brands offering personalized, subscription-based protein products. The convenience of doorstep delivery and growing awareness via digital marketing are accelerating retail sales.

Why did Texturization Segment Hold the Largest Wheat Protein Ingredients Market Share in 2025?

Texturization segment dominated the wheat protein ingredients market in 2025, driving the use of wheat protein in food and beverage applications. Its ability to create fibrous, chewy, and elastic textures makes it essential in bakery, meat substitutes, and processed foods. In bakery, it enhances dough strength, elasticity, and crumb structure. In meat analogues, it replicates the texture and mouthfeel of traditional meats, offering a satisfying sensory experience. Wheat protein also contributes to stability, water absorption, and resistance to crumbling in dry and frozen food items. This versatility makes texturization the primary reason why manufacturers prefer wheat protein over other alternatives.

The Foaming Expects the Fastest Growth in the Market During the Forecast Period

It can stabilize air bubbles and create light, voluminous textures without synthetic foaming agents. This property is highly desirable in vegan whipped creams, protein-enriched shakes, and bakery batters. As consumers seek clean-label formulations, wheat protein provides a natural way to add froth and fluffiness. Beverage companies are utilizing wheat protein to create latte foams, frothy teas, and protein cold brews. Additionally, aerated functional desserts like mousse and ice cream benefit from its stable foaming capacity.

Roquette

By Product Type

By Form

By Concentration

By Application

By End Use Industry

By Distribution Channel

By Functionality

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

March 2026

February 2026

February 2026

Wheat Protein Ingredients Market