April 2026

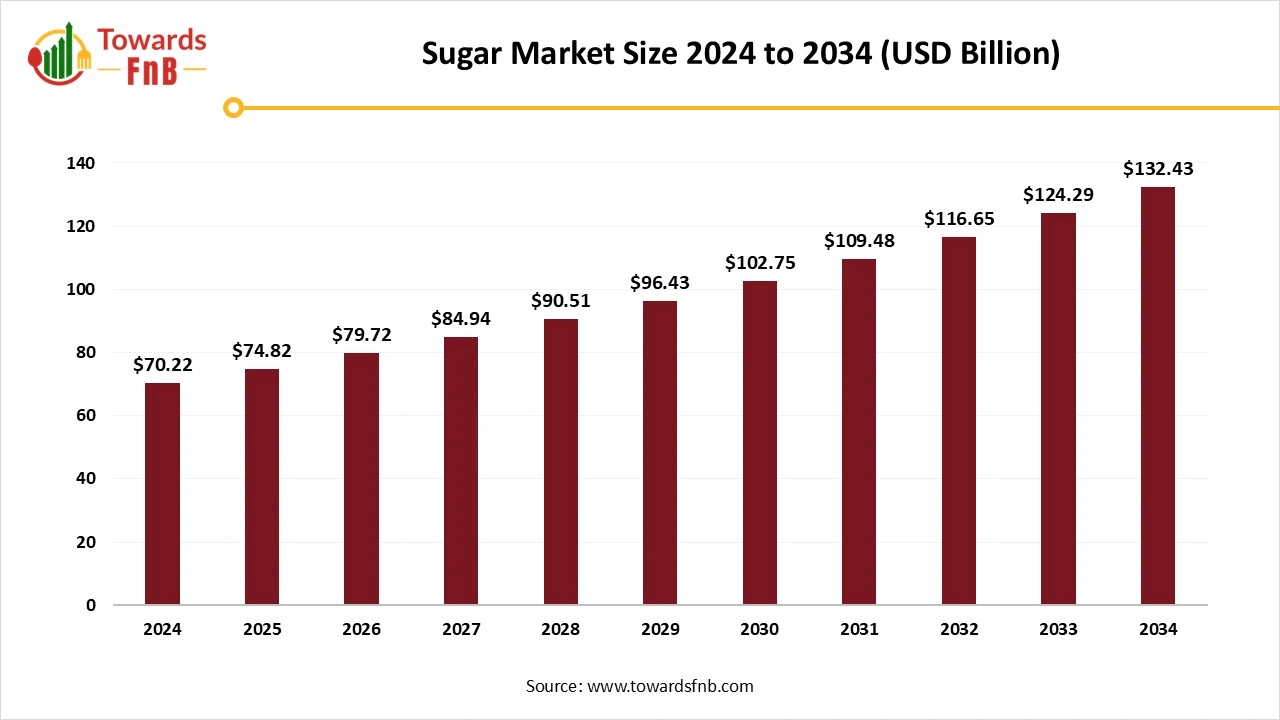

The global sugar market size stood at USD 74.92 billion in 2025 and is expected to grow steadily from USD 79.86 billion in 2026 to reach nearly USD 141.96 billion by 2035 with a CAGR of 6.6% during the forecast period from 2026 to 2035. The market is expanding significantly due to rising demand from the food and beverage industry and increasing consumption of processed and convenience foods.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.6% |

| Market Size in 2026 | USD 79.86 Billion |

| Market Size in 2027 | USD 85.14 Billion |

| Market Size by 2035 | USD 141.96 Billion |

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The sugar market dynamics are shaped by strong drivers such as rising demand from the food and beverage sector, increased consumption of confectionery, bakery, and soft drinks, along with the growing use of sugar in ethanol production for biofuels. However, the market is constrained by factors such as a global shift in consumer preferences toward low-calorie sweeteners, tighter government regulations on sugar content, and growing health concerns about diabetes and obesity. However, there are also a lot of opportunities due to the growing demand in emerging economies for the growing use of pharmaceuticals and personal care products, and technological advancements in sustainable sugar production and processing techniques.

Sugar consumption is rising in countries like Brazil, India, and Southeast Asia due to urbanization, population growth, and rising disposable incomes. This presents opportunities for market expansion. The demand for sweetened drinks and desserts is also being driven by urban lifestyles and the expanding cafe culture. In certain areas, governments are making investments in sugarcane farming, which helps to boost output even more

Sugar prices are very prone to fluctuations. In 2025, supply uncertainties and price swings on the global market caused raw sugar futures to hit multi-year highs in the first quarter. For producers and traders, financial planning and risk management are made more difficult by this volatility. In addition, the Brazilian real's decline versus the U.S.A. dollar in late 2024 highlighted the intercedence of global markets and helped to lower global sugar prices.

Raw Material Procurement

Packaging and Branding

Waste Management and Recycling

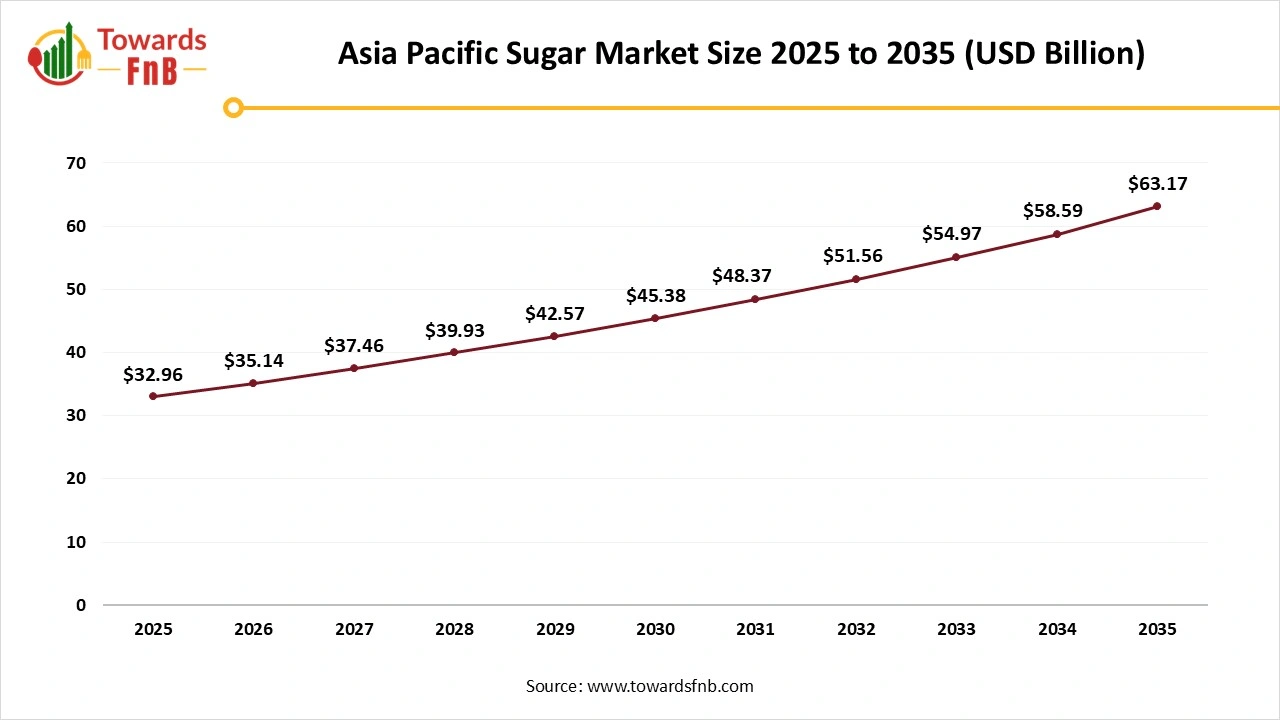

Asia Pacific Dominated the Sugar Market in 2025 and is Expected to Sustain its Growth During the Forecast Period

The region's dominance is driven by a large amount of sugarcane being grown well, established processing facilities, and high consumption in the food and beverage industries. The region's leadership is being reinforced by growing investments in sophisticated farming methods as well as by the growing urban population and demand for processed food. Production efficiency is also being increased by the incorporation of contemporary milling technologies, growing exports, and encouraging government policies. Additionally, growing consumer preferences for specialty sugars and conventional sweeteners guarantee consistent long-term growth in the area.

Asia Pacific Sugar Market Size and Growth 2025 to 2035

The global sugar market size was valued at USD 32.96 billion in 2025 and is expected to grow steadily from USD 35.14 billion in 2026 to reach nearly USD 63.17 billion by 2035 with a CAGR of 6.72% during the forecast period from 2026 to 2035.

North America Expects Significant Growth in the Sugar Market During the Forecast Period

Driven by the growing food and beverage industries, growing disposable incomes, and growing consumer demand for sweetened products. Because consumers are looking for more indulgent and convenient products, the regions' bakery confectionery and beverage segments are especially contributing to this growth. Sugar intake is also increased by seasonal and celebratory demand peaks. Market penetration is accelerated by the growth of organized retail chains and e-commerce platforms, which also guarantee greater accessibility and availability of sugar products.

Sugar Market Share, By Source, 2025 (%)

| Segments | Shares (%) |

| Sugarcane | 78% |

| Sugar Beet | 22% |

What Made the Sugarcane Segment Dominate the Sugar Market in 2025?

Sugarcane segment held the largest share of the market in 2025, driven by its cost-effectiveness, established cultivation methods, and high yield. The market's dominance in cane sugar production and consumption is guaranteed by the extensive processing infrastructure. Further increasing sugarcane in tropical regions, and the extensive availability of sugarcane in tropical regions, and the extensive processing infrastructure. Further increasing sugarcanes economical value are by products like bagasse and molasses which are extensively utilized in bioenergy and molasses which are extensively utilized in bioenergy and animal feed. Maintaining high output and quality standards is also aided by investments in contemporary harvesting and milling technologies.

Sugar Beet Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Driven by the need for locally produced sugar, technological developments in beet cultivation, and expansion in temperate regions. Its rapid growth can be attributed to its shorter harvesting cycle and suitability for sustainable farming methods. Growth of further accelerated by the subsidies and research initiatives that governments which are providing to support sugar beet cultivation higher sugar beet cultivation. Higher sugar recovery rates are also made possible by improved processing methods, increasing its competitiveness with sugarcane.

Sugar Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Refined Sugar | 56% |

| Raw Sugar | 27% |

| Organic / Specialty Sugar | 17% |

Which Product Type Segment Dominated the Sugar Market in 2025?

Refined sugar segment held the dominating share of the market in 2025 due to its long shelf-life, consistent quality, and extensive use in the food and beverage sector. Its dominant position worldwide is maintained by well-established refining procedures and a strong consumer preference for granulated or white sugar. It maintains its dominance by lowering impurities and energy consumption through ongoing improvements in refining techniques. Stable demand across regions is guaranteed by redlined sugars' dependability for use in domestic and industrial settings.

Organic/Specialty Sugars Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Driven by the need for clean-label or minimally processed products, growing disposable incomes, and growing health consciousness. Health-conscious consumers are increasingly purchasing products like brown raw sugar, a specialty sugar. Additionally, producers are launching fortified and flavored sugar products to target specific markets. Organic certification schemes and sustainability projects increase value and foster customer confidence.

Sugar Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Granulated | 72% |

| Powdered / Liquid | 28% |

Which Form of Sugar Dominated the Sugar Market in 2025?

Granulated segment dominated the market with the largest share in 2025 because it is adaptable, simple to use in homes and in the production of food, and compatible with a wide range of recipes and industrial procedures. Since it is standardized, it is the most widely consumed form of sugar in the world. Because it ensures consistent mixing and baking results, granulated sugar is also preferred for automated industrial processes. Both industrial and consumer needs are effectively met by its bulk and retail packaging.

Powered and Liquid Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Driven by the need for early-use formats in the grocery, bakery, and beverage industries. Rapid adoption is facilitated by their practicality and simplicity of integration into industrial processes. Liquid sugar is used in syrups, sauces, and soft drinks, while powdered sugar is used more in confections and bakery toppings. To preserve quality while in transit, manufacturers are spending money on cutting-edge storage and transportation systems.

Why did the Food & Beverages Segment Dominate the Sugar Market in 2025?

Food & beverages segment held the largest share of the market in 2025 because sugars are necessary for processed foods, baked goods, confections, and beverages. This industry is the main source of sugar consumption worldwide. Processed foods and sweetened beverages are consistently in demand due to urbanization and population growth. Recipe and flavoring innovations also help to maintain the demand for sugar in a variety of culinary applications.

The Pharmaceuticals & Personal Care Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Especially in mouthwash lozenges and syrups. Growing personal care markets, functional food innovations, and rising consumption of health products are the main drivers of growth. Increased emphasis on regulatory compliance and product safety is also encouraging adoption. In specialty formulations, sugar derivatives such as sorbitol and xylitol are also being utilized more frequently.

Which Industry Segment Dominated the Sugar Market in 2025?

Industrial sugar segment led the market in 2024 as it is extensively used in bulk manufacturing of processed foods, beverages, and other sugar-sweetened products. Large-scale processing and steady industrial demand maintain its leading share. The segment benefits from long-term contracts with manufacturers, ensuring predictable demand. Continuous investments in production efficiency and quality control help sustain market leadership.

Specialty/Organic Sugar Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Because consumers are becoming more interested in high-end health health-conscious, and ethically sourced goods. Specialty sugar, low GI, and organic varieties are included in this category to appeal to specific markets. Adoption is further fueled by rising awareness of social responsibility and environmental sustainability. Additionally, innovations in labeling and packaging increase the visibility of products and their appeal to consumers.

Supplyco

Louis Dreyfus Company

By Source/Crop

By Product Type

By Form

By End Use/Application

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Sugar Market