April 2026

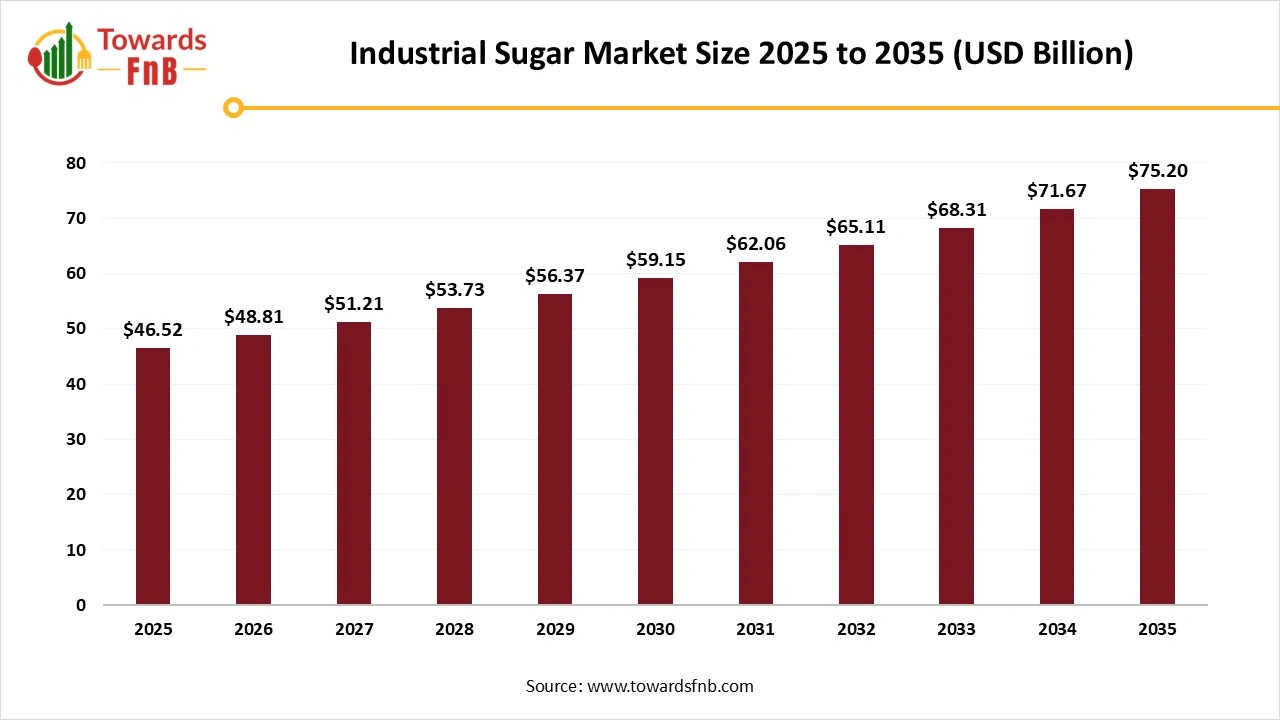

The global industrial sugar market size estimated at USD 46.52 billion in 2025 and is predicted to increase from USD 48.81 billion in 2026 to reach nearly USD 75.20 billion by 2035, with a CAGR of 4.92% during the forecast period from 2026 to 2035. The industrial sugar market is driven by rising consumption of processed foods and beverages worldwide.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 4.92% |

| Market Size in 2026 | USD 48.81 Billion |

| Market Size in 2027 | USD 51.21 Billion |

| Market Size by 2035 | USD 75.20 Billion |

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The industrial sugar market refers to the large-scale production and supply of sugar used as an ingredient in industrial food, beverage, pharmaceutical, and other manufacturing applications. Unlike retail sugar, industrial sugar is supplied in bulk and customized to meet the functional requirements of end-use industries such as sweetness, texture, fermentation, preservation, and color.

Industrial sugar is primarily derived from sugarcane and sugar beet and is available in multiple forms, such as white refined sugar, brown sugar, and liquid sugar. The global industrial sugar market’s growth is driven by rising demand from the food and beverages industry, expanding processed food consumption, and the development of high-purity and specialty sugar grades. Additionally, the increasing use of sugar in bioethanol production and pharmaceuticals is further expanding market opportunities.

The rise of technological advancements in the industrial sugar industry is driven by sustainability initiatives, automation, and digitalization. Major developments such as IoT and AI for automated mill operations and precision farming, advanced processing methods for better quality control, and blockchain for supply chain transparency. In addition, rising innovations in bioenergy production from genetic research and by-products are creating new revenue streams and improving crop resilience. Furthermore, a chain for supply chain transparency.

In addition, rising innovations in bioenergy production from genetic research and by-products are creating new revenue streams and improving crop resilience. Furthermore, AI-generated systems are used for precision agriculture, including reducing resource use and optimal harvest times. Cloud computing and IoT sensors also optimize production processes, monitor performance, and automate mill operations, which is expected to revolutionize the market growth.

Top exporters (who supply the market)

Top importers (who buy)

Recent structural drivers of trade flows

Price/stock implications

Raw Material Procurement

Packaging and Branding

Waste Management and Recycling

| Country / Region | Regulatory Body(s) | Key Regulations / Standards (High Level) | Focus Areas | Notable Notes |

| United States | U.S. Food and Drug Administration (FDA); United States Department of Agriculture (USDA); Environmental Protection Agency (EPA) | FDA Food Safety Modernization Act (FSMA) - Nutrition Labeling and Education Act (NLEA) - USDA Agricultural Marketing Service (sugar program & quotas) - EPA regulations for waste and emissions control | Food safety, labeling, and product traceability Import/export quotas and domestic pricing policies - Environmental sustainability and waste management | The U.S. sugar industry is governed by federal quotas and price support programs; labeling reforms target sugar disclosure; FSMA ensures compliance in processing facilities. |

| European Union | European Commission (DG SANTE, DG AGRI); European Food Safety Authority (EFSA); ECHA | Common Agricultural Policy (CAP) and Sugar Regime - REACH / CLP for chemicals used in processing - EFSA food safety and nutritional labeling directives (EU Regulation No. 1169/2011) | Food safety, additives, and labeling compliance Environmental impact and worker protection - Agricultural production quotas and trade regulation | The EU sugar industry transitioned from quota regime in 2017, strong focus on labeling transparency and sustainable sourcing under the Green Deal. |

| India | Food Safety and Standards Authority of India (FSSAI); Department of Food & Public Distribution; Ministry of Environment, Forest and Climate Change (MoEFCC) | FSS (Food Product Standards and Food Additives) Regulations, 2011 - Sugar Development Fund Act - National Biofuel Policy (for sugarcane diversion to ethanol) - State-level Pollution Control Board standards | Food safety and hygiene - Sustainable production and effluent control - Cane pricing and ethanol blending policies | India regulates sugar through dual frameworks: FSSAI ensures quality compliance while DFPD manages cane pricing and export quotas; ethanol programs impact sugar output. |

| Brazil | Ministry of Agriculture, Livestock and Supply (MAPA); National Health Surveillance Agency (ANVISA); Brazilian Institute of Environment (IBAMA) | National Bioenergy Policy (RenovaBio) - Environmental regulations for emissions and water use - ANVISA food labeling and additive rules | Sustainable cane cultivation and ethanol integration Environmental compliance in milling operations - Nutritional labeling and sugar reduction | Brazil’s RenovaBio encourages low-carbon sugarcane ethanol; integrated sustainability certification impacts sugar mill operations. |

| China | State Administration for Market Regulation (SAMR); Ministry of Agriculture and Rural Affairs (MARA); General Administration of Customs | National Food Safety Standards (GB standards) - Import licensing and tariff quota system - Environmental protection laws for sugar processing plants | Quality control and import inspections - Domestic production support and pollution control - Food safety certification | China imposes strict quality testing on imported sugar and maintains tariff rate quotas to balance domestic and foreign supply. |

| Australia / New Zealand | Food Standards Australia New Zealand (FSANZ); Department of Agriculture, Fisheries and Forestry | Food Standards Code (FSANZ) - Environmental Protection Acts (federal/state level) - Biosecurity and import inspection rules | Labeling accuracy and consumer information - Environmental and workplace safety compliance - Sustainable farming and trade facilitation | Strong focus on transparency in sugar labeling; strict biosecurity measures govern imports to protect domestic cane growers. |

| Middle East / Africa | Gulf Standardization Organization (GSO); South African Bureau of Standards (SABS); National Food Safety Authorities | Gulf Standards for Sugar and Sweeteners (GSO 1919) - National Food Control Acts and environmental codes - Import regulations and subsidies for local refiners | Food quality and purity compliance - Import dependency management - Industrial safety and environmental control | GCC countries import most of their sugar; SABS oversees local refining quality; regional policies encourage food security and domestic production. |

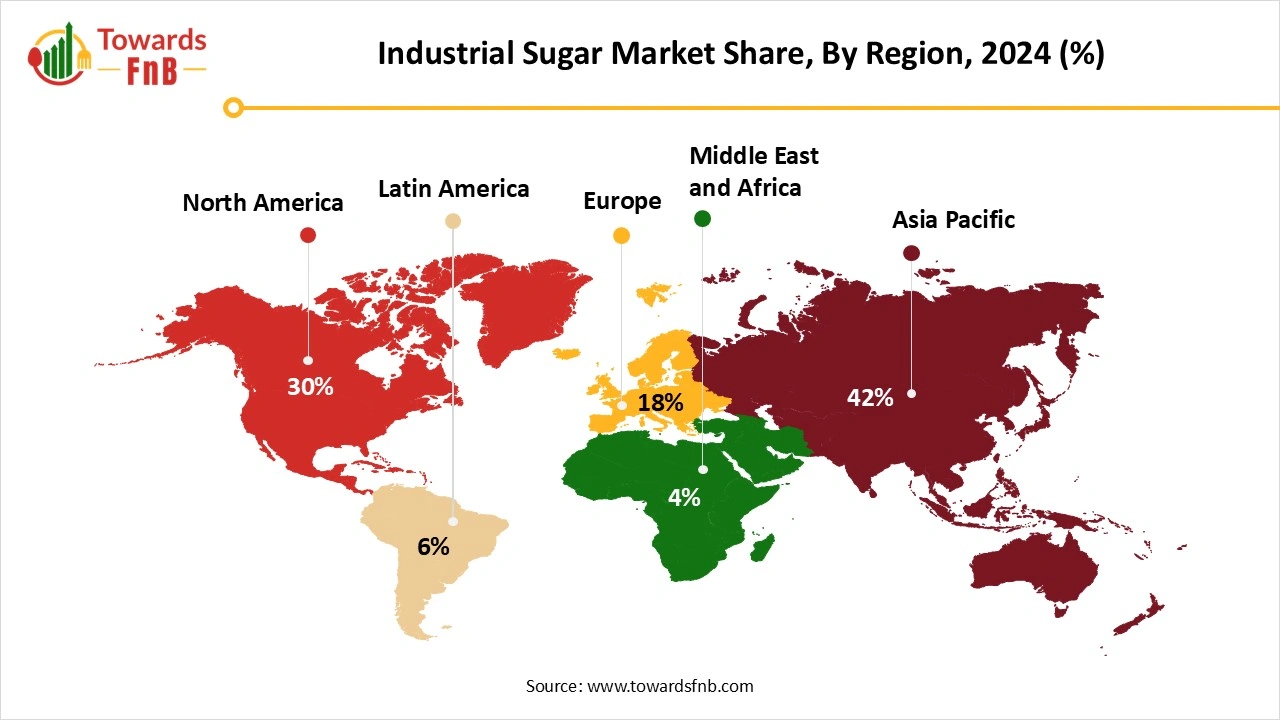

Why is Asia Pacific Dominating the Industrial Sugar Market?

Asia Pacific dominated the global market, accounting for 42% of revenue in 2025. The market growth in the region is driven by factors such as Strong demand from the food, beverage, and ethanol sectors, increasing presence of large sugar processing facilities, rising technological advancements in sugar manufacturing that improve product quality and efficiency, increasing demand for processed food and beverages, increasing rapid production of sugarcane in the region, rising urbanization and increasing disposable incomes. China, India, Japan and South Korea are dominating countries driving the market growth.

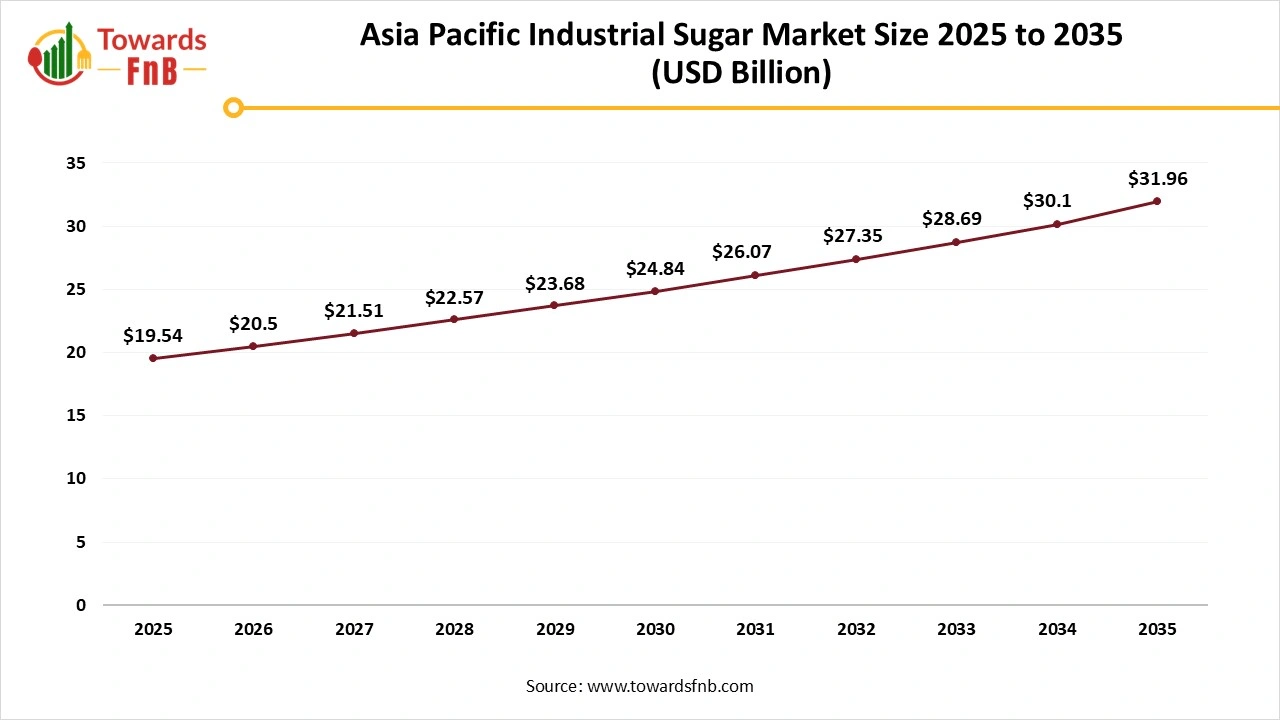

Asia Pacific Industrial Sugar Market Size 2025 to 2035

The Asia Pacific industrial sugar market size estimated at USD 19.54billion in 2025 and is predicted to increase from USD 20.5 billion in 2026 to reach nearly USD 31.96 billion by 2035, with a CAGR of 5.04% during the forecast period from 2026 to 2035.

India Industrial Sugar Market Trends

India dominated global revenue from industrial sugar in 2025. The market growth in India is attributed to factors such as rising consumer demand for processed food, increased government support for initiatives such as ethanol blending, higher sugarcane production, changing lifestyles, and rising investment in micro-irrigation and precision farming.

Africa and Middle East Region Is Expected to Grow Fastest During the Forecast Period

The market growth in the region is driven by factors such as the increasing demand for packaged and processed foods, such as beverages, dairy and baked products, increasing disposable incomes, rising rapid urbanization, the growing food and beverage industry and growing e-commerce platforms in the region. South Africa, UAE, Saudi Arabia and Kuwait are the major countries driving the market growth.

South Africa Industrial Sugar Market Trends

South Africa is expected to grow fastest during the forecast period and is a major player in the plant-derived and synthetic sugar markets. There are efforts to inspire manufacturers, wholesalers and local retailers to prioritize purchasing locally grown sugar in the country. The government is working on various supportive initiatives to increase domestic sugar consumption, stabilize the health promotions and provide support, further increasing the demand for sugar consumption in South Africa.

")

North America is Expected to Grow at a Notable Rate During the Forecast Period

The market growth in the region is driven by factors such as increasing demand for clean-label and organic products, rising consumer preference for government regulations and sugar substitutes, increased production of biofuels from sugarcane and corn, and rising demand for processed food and beverages, snacks, and confectionery. The U.S. and Canada are the major drivers of market growth in the region.

The U.S. Industrial Sugar Market Trends

The U.S. industrial sugar industry is expected to grow significantly, driven by the increasing demand for industrial beet sugar, the rise of the e-commerce industry for distribution, increasing demand for sugar in food and drinks, the growing processed food and beverage industry and increasing health-conscious consumers.

Latin America Industrial Sugar Market Trends

The market growth in the region is driven by the increasing large consumer base, growing rapid urbanization, growing food and beverage industry, increasing consumer changing and modern lifestyles, increasing demand for products such as beverages and confectionery, growing biofuel industry and increasing rapid consumption of sweeteners. Brazil, Mexico and Argentina are the major countries driving the market growth.

Mexico Industrial Sugar Market Trends

The country's market growth is driven by increasing demand for sustainable and alternative food products and by expanding food and beverage industries, especially convenience and processed foods. Other factors such as the growing fermentation applications in food and beverages and increasing prevalence of chronic diseases and government health campaigns, rising technological advancements, and increasing demand for baked goods and confectionery.

Industrial Sugar Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| White Sugar (Refined) | 53% |

| Brown Sugar | 12% |

| Liquid Sugar / Syrup | 15% |

| Raw Sugar | 13% |

| Specialty Sugar | 7% |

Why is White Sugar (Refined) Segment Dominating the Industrial Sugar Market?

The white sugar (refined) segment dominated the global market, accounting for 53% of revenue in 2025. While sugar plays an important role in the industrial sugar industry due to its long shelf life, high purity, and uniformity, which make it a reliable and versatile ingredient for food and beverage manufacturing. Its consistent performance and neutral flavor, along with its bright appearance and ease of processing, are major benefits that appeal to manufacturers looking for high-quality, predictable products. In addition, refined sugar makes industrial processes, such as confectionery production and baking, more efficient and ensures a predictable performance and uniform flavor across batches.

The Liquid Sugar/Syrup Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in the industrial sugar market is driven by factors such as enhancing shelf life, improving texture, preventing crystallization, increasing demand for ready-to-use format, cost-effectiveness, lower capital costs, reduced processing time, acting as a flavor enhancer, reducing processing time, capital costs and labor and reducing the need for dissolution.

The specialty sugar segment is expected to grow at a notable rate during the forecast period. Specialty sugars offer various advantages in the industrial sugar market by allowing specific functionalities in pharmaceutical products and food and beverages. These benefits include improving product quality, such as stability and shelf life, increasing consumer demand for specialized or healthier options, such as organic or low-GI sugars, and adding unique colors, textures, and flavors to products.

Industrial Sugar Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Sugarcane | 78% |

| Sugar Beet | 15% |

| Other Natural Sources | 7% |

Why is Sugarcane Segment Dominating the Industrial Sugar Market?

The sugarcane segment dominated the global market, accounting for 78% of revenue in 2025. Sugarcane offers industrial advantages through its raw materials, including ethanol, sugar, and byproducts such as molasses and bagasse. This versatility contributes to sustainable energy, generates employment and revenue, and supports a robust agro-based industry. In addition, sugarcane provides export value through its processed products and is a major revenue-generating crop, contributing substantially to agricultural GDP. Its processing and cultivation create various direct and indirect employment opportunities in rural areas, further supporting factory workers and farmers.

The Sugar Beet Segment is Expected to Grow Fastest During the Forecast Period

Sugar beets offer various benefits in the industrial sugar market, including valuable byproducts such as bioethanol for fuel and pulp for animal feed, a locally grown and non-GMO alternative to cane sugar and a source of high-purity sucrose for food and beverages. In addition, sugar beet helps in a huge range of industrial applications, from baking to beverages, particularly where appearance and consistency are crucial.

The other natural sources segment is expected to grow at a notable rate during the forecast period. The segment growth in the global market for industrial sugar is driven by factors such as increasing government policies on refined sugar, increasing consumer preference towards organic and natural ingredients, increasing consumer awareness towards health and wellness, increasing focus on sustainability, increasing disposable incomes, and rising technological advancements and product innovation.

Industrial Sugar Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Food & Beverage | 61% |

| Bakery & Confectionery | 9% |

| Dairy & Frozen Desserts | 8% |

| Beverages | 7% |

| Pharmaceuticals | 5% |

| Personal Care & Cosmetics | 1% |

| Biofuel | 3% |

| Chemical Industry | 4% |

| Others | 2% |

How is the Food and Beverage Segment Dominating the Industrial Sugar Market?

The food and beverage segment dominated the global market, accounting for 61% of revenue in 2025. Segment growth in the global market is driven by factors such as the increasing use of both specialty and traditional sugars, technological advancements, government support for sugar cultivation, and consumer preference for ready-to-drink products and convenience. In addition, a growing global population, rapid urbanization, changing consumer lifestyles and increasing demand for processed foods and beverages.

The Biofuel (Ethanol Production) Segment is Expected to Grow Fastest During the Forecast Period

The biofuel production helps manage sugar surplus, improves financial health and mitigates sugar price volatility. This also creates demand for sugar crops and enables more timely payments to farmers. By using byproducts such as molasses, biofuel production enhances better waste management and reduces greenhouse gas emissions, which is expected to drive the market growth.

The pharmaceuticals segment is expected to grow at a notable rate during the forecast period. The segment growth in the industrial sugar market is driven by factors such as increasing consumer awareness towards health and wellness, increasing use in pharmaceuticals, increasing demand for innovative products across the biofuel and food and beverage industries, increasing prevalence of chronic diseases, growing population across the globe, and increasing demand for specific pharmaceutical-grade sugars used in injectable solutions and tablet formulations.

Tetra Pak India

Nestlé

By Type

By Source

By Application

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Industrial Sugar Market