April 2026

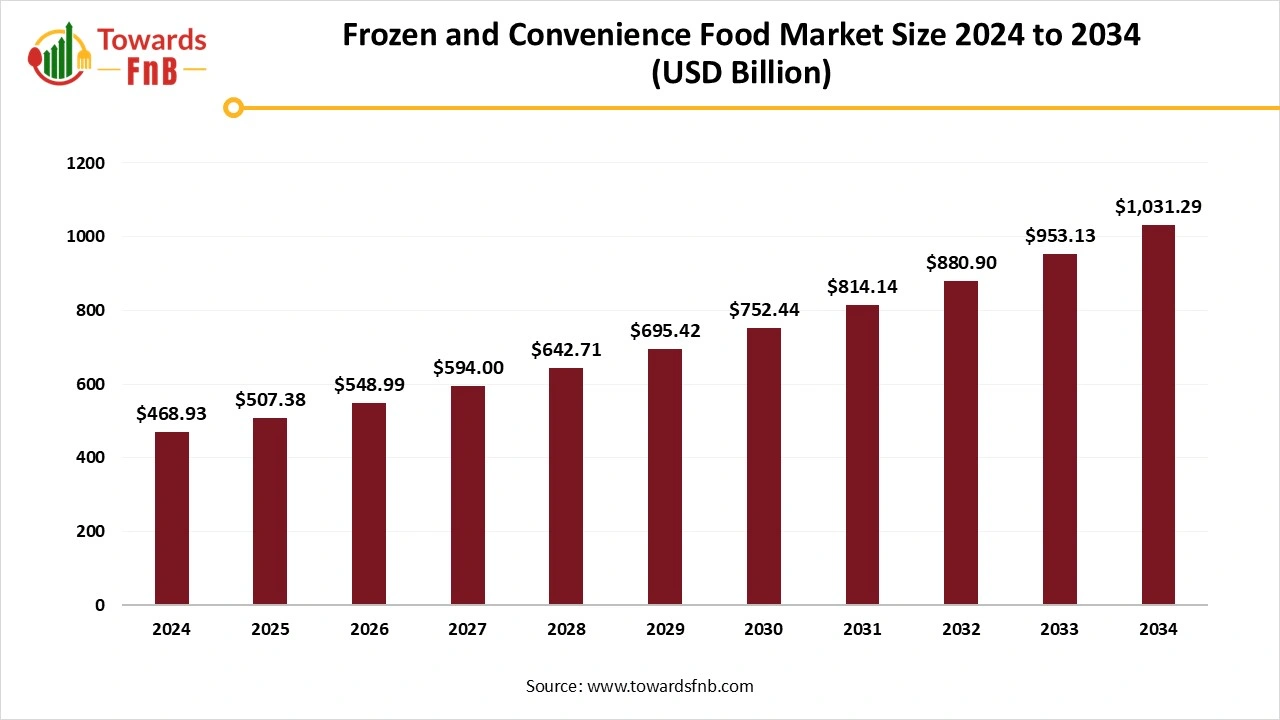

The global frozen and convenience food market size reached at USD 468.93 billion in 2024 and is anticipated to increase from USD 507.38 billion in 2025 to an estimated USD 1,031.29 billion by 2034, witnessing a CAGR of 8.2% during the forecast period from 2025 to 2034. The growth of the market is driven by the increasing demand for convenience food due to modern lifestyles and busy schedules, which may enhance consumer satisfaction.

| Study Coverage | Details |

| Growth Rate from 2025 to 2034 | CAGR of 8.2% |

| Market Size in 2025 | USD 507.38 Billion |

| Market Size in 2026 | USD 548.99 Billion |

| Market Size by 2034 | USD 1,031.29 Billion |

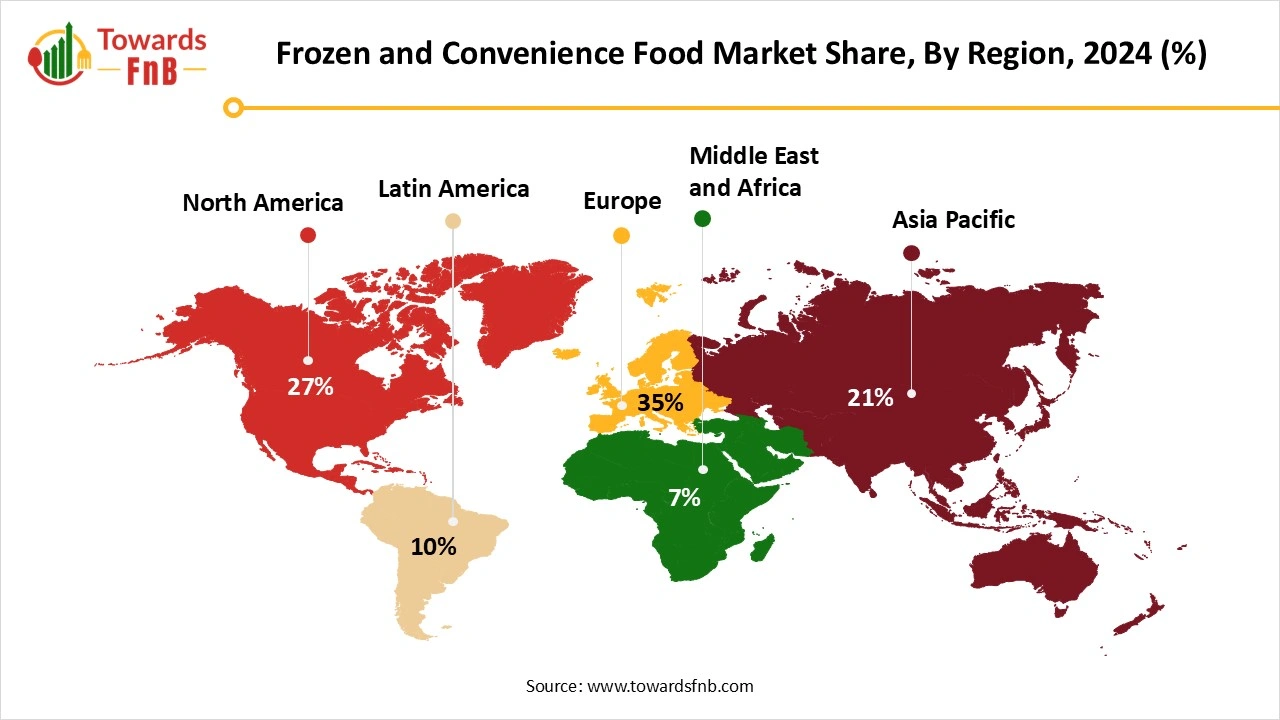

| Largest Market | Europe |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The global frozen and convenience food market covers the production, processing, distribution, and consumption of ready-to-cook (RTC), ready-to-eat (RTE), and semi-prepared food products designed for extended shelf life, ease of preparation, and time-saving convenience. This category includes frozen meals, snacks, bakery items, meat & seafood, fruits & vegetables, and packaged convenience foods. Market growth is driven by urbanization, rising dual-income households, demand for quick meal solutions, expansion of cold-chain logistics, and the adoption of Western dietary habits in emerging markets.

There are several major factors driving the frozen convenience food market growth, including rising customer moder and busy lifestyles, and increasing demand for ready-to-cook and ready-to-eat foods are expected to fuel growth of the market across the globe. In addition, rising need for frozen food including frozen snacks, frozen vegetables, frozen fruits and ready-to-cook foods is becoming a household initiative, which may accelerate the demand for market during the forecast period.

One of the major opportunities revolutionizing the market growth is the increasing technological advancements in frozen and convenience food. The rising advanced techniques including vacuum sealing, quick frozen (IQF) and cryogenic freezing focus on nutritional texture, taste, and value. In addition, due to the adoption of smart packaging, robotic automation, and AI-generated quality control, the production procedures are becoming more efficient and convenient in frozen and convenience food, which may present major growth opportunities in the global market. In addition, rising demand for personalization and data-driven innovation are also revolutionizing the frozen and convenience category, as technology becomes more advanced into customer life, which is further considered to revolutionize the growth of the frozen and convenience food market in the coming years.

One of the major factors restraining market growth is the increasing supply chain disruptions in frozen and convenience food. From manufacturing to the retail shelf, balancing the consistency of the cold chain is complicated. Any disruptions in the supply chain can lead to issues in food safety, product spoilage, and recalls. This can be vital for grocery stores, hypermarkets and supermarkets, which may create major hurdles in customers satisfaction. In addition, display and storage prices, regulatory compliance, and environmental effect are other challenging factors expected to restrain the growth of the frozen and convenience food market.

How Europe Dominates the Frozen and Convenience Food Market Revenue in 2024?

Europe dominated the global market revenue in 2024. The market growth in the region is attributed to the factors such as the increasing demand for convenient and time-saving food solutions, increasing high consumer spending power, increasing consumer awareness for nutritional value, increasing shrinking households and busy lifestyles, increasing consumer preference towards private-label and plant-based food options, expansion of product offerings and growing e-commerce and online retail platforms. UK, Germany and France are dominating countries driving the growth in Europe.

Germany dominated the market revenue in 2024, driven by the increasing high disposable incomes, increasing demand for online delivery services, increasing demand for sustainable and healthy options, increasing demand for meat/poultry, fish, potato products and fruit and increasing consumer demand for convenient and high-quality frozen foods.

")

Asia Pacific Frozen and Convenience Food Market Trends

Asia Pacific is expected to grow fastest during the forecast period. The market growth in the region is driven by factors such as the rising innovations in product offerings such as ethnic food and ready meals, increasing cold chain and retail infrastructure enhancing accessibility, growing working women population, growing rapid urbanization, increasing consumer changing lifestyles, increasing disposable incomes and increasing demand for frozen bakery products. China, India, Japan and South Korea are the fastest growing countries driving the market growth in the region.

How Frozen Meals & RTE Segment Dominates the Frozen and Convenience Food Market Revenue in 2024?

The frozen meals and RTE segment dominated the market in 2024. The segment growth in the global market is attributed to the rising technological advancements in processing and packaging methods, increasing rapid urbanization, increasing changing lifestyles, increasing demand for ready-to-eat frozen food, increasing demand for foodservices such as cafes, restaurants and hotels and increasing demand for on-the-go options such as RTE products, sandwiches, snacks and other frozen foods.

The Frozen Snacks and Plant-Based Alternatives Segment is Expected to Grow Fastest During the Forecast Period.

The segment growth in the market is driven by the increasing demand for sustainable choices, increasing changing and busy lifestyles, reduced waste and increasing longer shelf life, increasing affordability and convenience, increasing demand for clean-label and plant-based food products and increasing consumer awareness towards health and wellbeing.

Why RTC Segment Held the Largest Frozen and Convenience Food Market Revenue in 2024?

The ready-to-cook (RTC) segment dominated the market in 2024. The segment growth in the global market is driven by factors such as increasing focus on transparency and quality, increasing demand for ready-to -cook frozen food, increasing demand for direct-to-consumer and online platforms services, rising technological advancements in freezing and packaging technologies, increasing number of working populations, increasing rapid urbanization and changing lifestyles, increasing need for quick meal solutions and increasing dual-income households.

The Ready-to-Eat (RTE) Segment is Expected to Grow Fastest During the Forecast Period.

The segment growth in the global frozen and convenience food market is driven by factors such as increasing consumer preference towards modern eating habits, increasing demand for on-the-go options, increasing changing lifestyles and rapid urbanization. In addition, by offering unparalleled convenience for time-saving and busy consumers, ready-to-eat foods significantly enhance the growth of convenience and frozen food, which is further expected to drive the segment growth in the global market.

What Factors Help Supermarkets or Hypermarkets Segment Grow in 2024?

The supermarkets and hypermarkets segment dominated the frozen and convenience food market revenue in 2024. The growth of the market is attributed to the factors such as increasing demand for offline stores, increasing demand for high-quality and plant-based food products, increasing demand for bakery product, increasing product accessibility, increasing demand for convenience food and increasing consumer preference towards one-stop shopping experiences.

The Online/E-Commerce Platforms is Expected to Grow Fastest During the Forecast Period.

The segment growth in the global market is driven by factors such as increasing consumer preference towards online shopping, growing e-commerce platforms, increasing integration of internet connectivity and increasing demand for ready-to-eat options.

How Household/Residential Segment Dominates the Frozen and Convenience Food Market Revenue in 2024?

The household and residential segment dominated the global market in 2024. The growth of the market is driven by factors such as increase in dual-income households and working women population, increasing rapid urbanization, increasing changing lifestyles, and increasing demand for convenience and frozen foods. The ready-to-eat and frozen foods provide a easy and quick solution, with modern consumers having less time for traditional food preparation, which is further expected to drive the segment growth.

The Foodservice (QSRs, HORECA) Segment is Expected to Grow Fastest During the Forecast Period.

The foodservice segment such as restaurants, hotels, cafes and others play an important role in frozen and convenience food. To enhance the cost-efficiency, consistency and speed needed by their business models, these food service segments based on convenient and frozen products. In addition, enhanced speed and convenience, consistent quality, inventory management and rise of online food services such as Swiggy and Zomato, which are further expected to drive the market growth.

Raw Material Procurement

Packaging and Branding

Waste Management and Recycling

Conagra Brands, Inc.

Nestlé

By Product Type

By Category

By Distribution Channel

By End-User

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Frozen and Convenience Food Market