April 2026

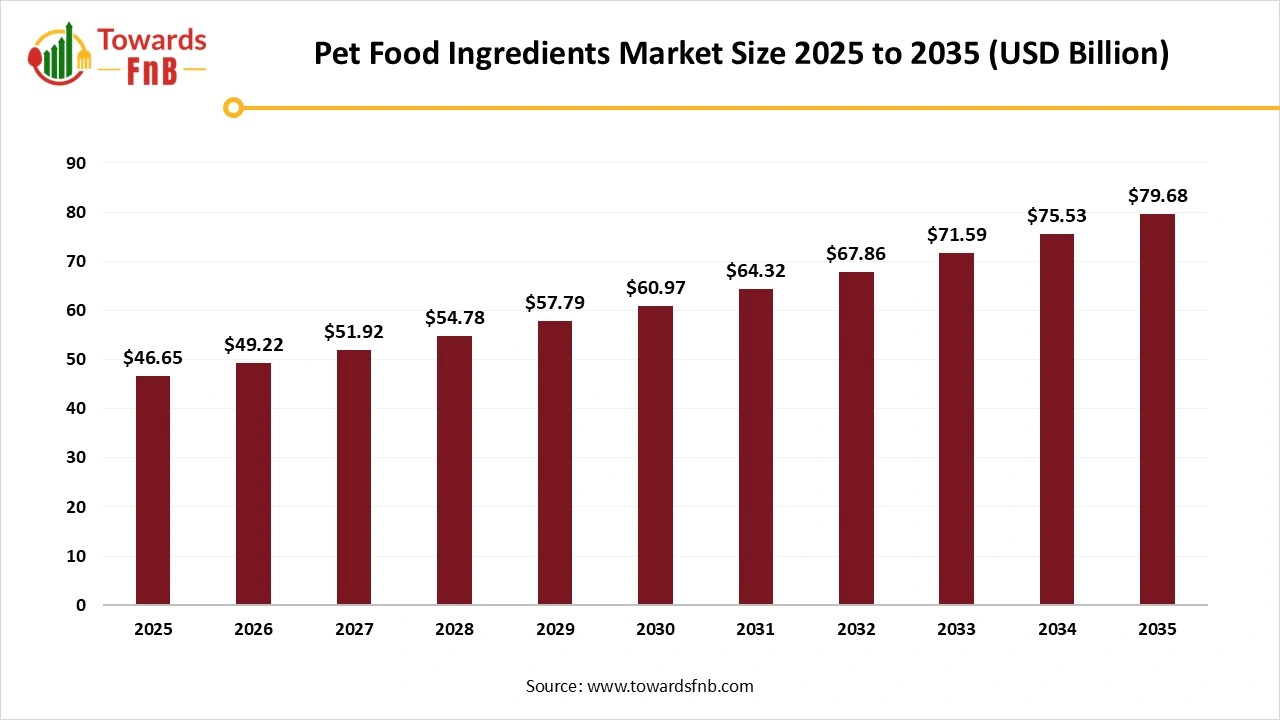

The global pet food ingredients market size reached at USD 46.65 billion in 2025 and is anticipated to increase from USD 49.22 billion in 2026 to an estimated USD 79.68 billion by 2035, witnessing a CAGR of 5.5% during the forecast period from 2026 to 2035. Market is driven by rising pet ownership and consumer demand for high-quality, transparent, and specialized pet nutrition.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.5% |

| Market Size in 2026 | USD 49.22 Billion |

| Market Size in 2027 | USD 51.92 Billion |

| Market Size by 2035 | USD 79.68 Billion |

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The pet food ingredients market is the sector of the food industry that supplies raw materials used to produce pet food. This market includes everything from animal and plant-based protein to carbohydrates, fats, vitamins, minerals, and functional additives like probiotics and omega fatty acids. Demand for these ingredients is driven by trends like rising pet ownership, premiumization of pet foods, and a greater focus on pet health and nutrition.

Improvements in technology, including AI and automation, are set to transform the processes of pet food manufacturing. These technological innovations are anticipated to improve efficiency, safety, and quality in pet food production. Investment in innovative ingredient production methods, including cell culturing, precision fermentation, microbial biomass fermentation, and plant molecular farming, has significantly increased in the food and feed industry over the last ten years. Core technologies encompass AI and data analytics for customized formulations, omics technologies for comprehensive nutritional understanding, and sophisticated processing techniques such as sous vide, freeze-drying, and cold pressing to maintain nutrient integrity. Sustainable development is also focusing on new protein sources like microbial and insect proteins.

Raw Material Procurement

Processing of Pet Food Ingredients

Packaging of Pet Food Ingredients

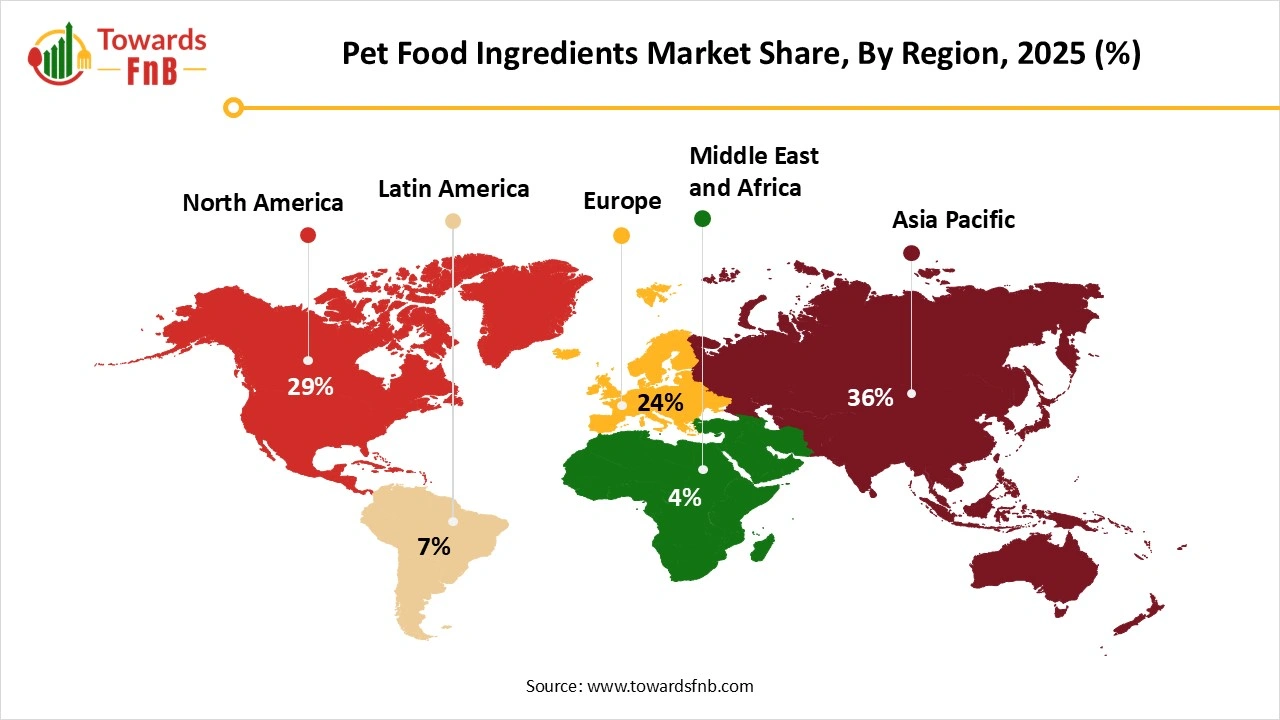

Asia Pacific: Market Leader in Pet Food Ingredients

Asia Pacific dominated the pet food ingredients market in 2025. The rise in pet ownership drives the need for pet food ingredients as consumers emphasize high-quality components for their pets diets. This evolving preference not only boosts manufacturers' sales but also drives them to innovate and expand their product offerings, thus enhancing the pet food ingredients market in the area. In Asia Pacific nations (APAC), 32% of families have a dog, whereas 26% possess a cat. Data indicates that in Asia-Pacific nations, K-9s dominate with 32%, surpassing 26% of cat owners. To understand these percentages better, Asia-Pacific encompasses densely populated countries such as China, Japan, the Philippines, South and North Korea, Pakistan, India, Bangladesh, among others. This increasing trend in pet ownership emphasizes the demand for diverse and nutritious ingredients in pet food. The rise in disposable income within the Asia-Pacific area marks considerable market expansion as people and households see increased earnings.

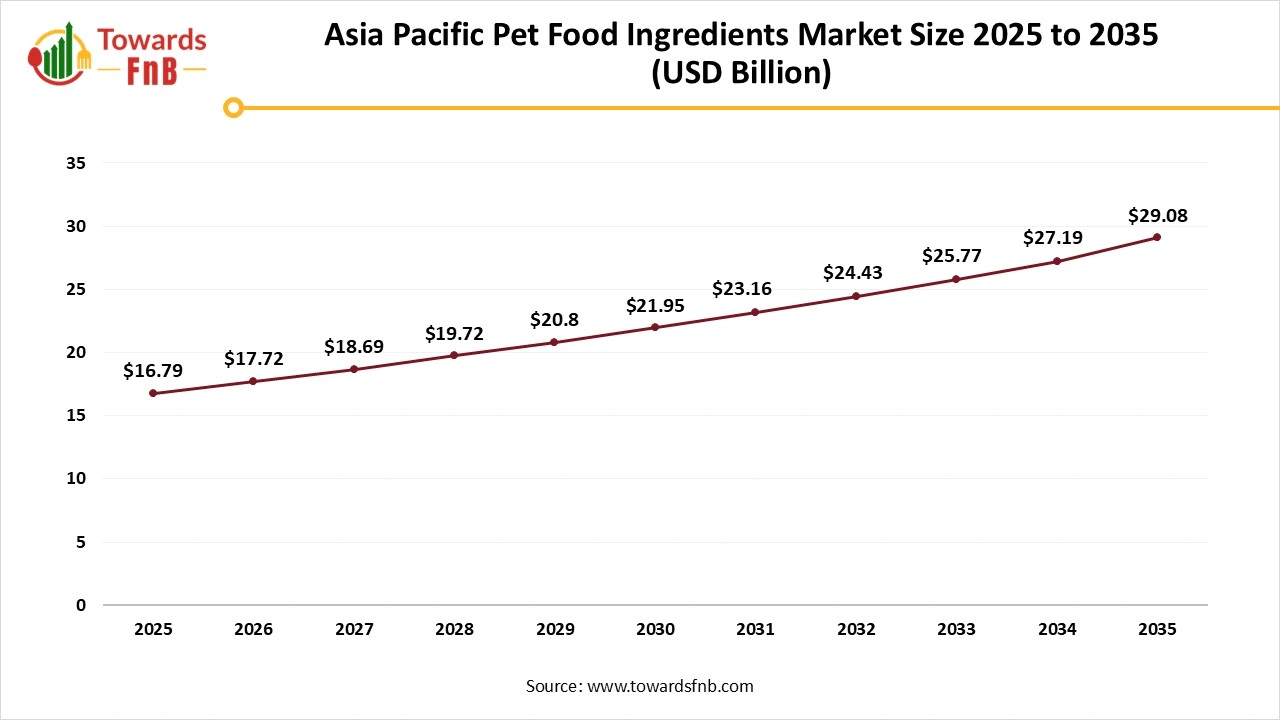

Asia Pacific Pet Food Ingredients Market Size 2025 to 2035

The Asia Pacific pet food ingredients market size was calculated at USD 16.79 billion in 2025 with projections indicating a rise from USD 17.72 billion in 2026 to approximately USD 29.08 billion by 2035, expanding at a CAGR of 5.65% throughout the forecast period from 2026 to 2035.

India Pet Food Ingredients Market

The Indian market is growing swiftly, fueled by a rise in pet ownership, higher disposable income, and a change in perceptions regarding pet care and nutrition. The rise of urban living and evolving lifestyles has prompted numerous families and young professionals to get pets, particularly in major cities like Delhi, Mumbai, Bengaluru, and Hyderabad. In response to the growing demand in India's pet food sector, local brands are progressively investing in product development by integrating traditional Indian elements like turmeric, giloy, ashwagandha, and moringa into pet nutrition.

Europe to Witness the Fastest Growth

Europe is expected to grow at the significant rate at the forecast period. Momentum is driven by the premiumization trend, the humanization of pets, and demographic changes favoring single-person households that allocate consistent discretionary spending to companion animal nutrition. Functional ingredients like probiotics, omega fatty acids, and joint-support blends are increasingly found in mainstream SKUs, supporting a value combination that leans towards elevated price levels. Trends like organic, natural, and grain-free diets are gaining popularity, encouraging ingredient suppliers to innovate in these sectors.

")

Germany Pet Food Ingredients Market

The demand for ingredients in pet food in Germany is robust and expanding, fueled by a significant pet population and rising consumer emphasis on quality, health, and sustainability. According to the most recent report from the Food Export Association of the Midwest USA and Food Export USA-Northeast, the German food processing sector generated approximately USD 239 billion in 2022, with pet food making up 7% of this income. This illustrates the significance of pet food in the market, highlighting its role in the broader economy and encouraging innovation and investment in the realm of pet food ingredients.

North America: High Growth Potential and Rising Pet Ownership

The North America pet food ingredients market has experienced significant expansion in recent decades, influenced by various elements that mold consumer choices and the changing requirements in the pet food sector. The market's growth can be mainly linked to evolving pet ownership patterns, a rise in pet humanization, and heightened awareness of pet health issues. Pet owners increasingly consider their pets as part of the family, leading to a preference for superior, natural, and nutritious food components. The need for high-quality pet foods that utilize superior ingredients has increased, creating a competitive market for novel ingredient sourcing and processing methods.

United States Pet Food Ingredients Market

The United States secures market dominance by developing a robust pet food industry framework and advanced nutritional technology, incorporating specialized ingredients throughout pet food products. The nation's growth rate indicates well-established industry connections and the adoption of advanced ingredient technology, facilitating the extensive implementation of functional nutritional systems in production plants. Expansion focuses on key pet food processing hubs such as Missouri, Ohio, and California, where advanced processing technologies highlight established ingredient usage that attracts producers looking for reliable nutritional features and effective operational strategies.

Latin America: Emerging Market Dynamics

The market for pet food ingredients in Latin America is expanding notably, fueled by higher pet adoption rates, increasing disposable incomes, and trends in pet humanization. Latin America ranks as the third-largest market for U.S. exports of dog and cat food, importing $162.0 million in 2024, which is an 11-percent rise from 2023. As the area's economy continues to stabilize from the COVID-19 pandemic, an increase in demand for imported dog and cat food is anticipated. With the rising demand for dog and cat food in Latin America, consumers are progressively pursuing high-quality pet food selections.

Brazil Pet Food Ingredients Market

The market for pet food ingredients is undergoing significant changes influenced by shifting consumer preferences and heightened consciousness about pet wellness. In Brazil, pet owners are becoming more selective regarding the ingredients in their pets diets, resulting in a demand for superior quality and more natural elements. This trend is evident in the increasing demand for organic and high-quality products, as pet owners aim to offer their animals diets that align with their own health-focused preferences. Moreover, the growth of e-commerce platforms has revolutionized the marketing and sale of pet food ingredients, facilitating increased accessibility and diversity.

Middle East & Africa: Growth Prospects in an Untapped Market

The rise of urban areas in nations such as the UAE, Saudi Arabia, and South Africa is greatly influencing the expansion of the pet food ingredients sector. With the rise of urban populations, the rates of pet ownership rise, boosting the need for various high-quality pet food options. The trend of humanizing pets, seeing them more as family members, is widespread in the MEA region. Consumer behavior varies greatly by region. In the countries of the Gulf Cooperation Council (GCC), consumers generally prefer premium imported pet food brands, placing great importance on quality and safety.

South Africa Pet Food Ingredients Market

The rising trend of households viewing pets as family members, known as pet humanization, is driving market expansion in South Africa. Additionally, urban transformations significantly influence pet adoption trends in the nation, with individuals in developed regions increasingly acquiring pets for companionship. Moreover, the rapid expansion of retail infrastructure and online shopping is increasing the market share of pet food in South Africa.

Pet Food Ingredients Market Share, By Ingredient Type, 2025 (%)

| Segments | Shares (%) |

| Specialty Proteins | 18% |

| Amino Acids | 38% |

| Mold Inhibitors | 4% |

| Gut Health Ingredients | 12% |

| Phosphates | 7% |

| Vitamins | 5% |

| Acidifiers | 3% |

| Antimicrobials & Antibiotics | 5% |

| Minerals | 2% |

| Antioxidants | 6% |

Why did the Amino Acids Segment Dominate the Pet Food Ingredients Market?

The amino acids segment led the pet food ingredients market in 2025, owing to their essential role in pet health, serving as the foundation for protein synthesis, muscle growth, and immune function. They are crucial for overall growth, development, and the protection of important organs and tissues, rendering them an essential part of a balanced diet for pets. The demand is also driven by pet owners prioritizing premium, high-quality pet foods.

Gut Health Ingredients Segment is Observed to Grow at the Fastest Rate During the Forecast Period

This growth is attributed to the humanization of pets, heightened awareness among owners regarding the connection between gut health and overall wellness, and the necessity for functional, scientifically-supported ingredients. Consumers are progressively looking for items that address particular health issues such as digestion, immunity, and nutrient absorption, perceiving gut health as essential to a pet's overall wellness, akin to human nutraceuticals.

The specialty proteins segment is experiencing significant growth throughout the forecast period, due to their importance in creating high-protein diets and addressing pets specific health requirements, such as muscle development, weight control, and hypoallergenic needs. The trend of "high-protein" is trending in human food and has made its way into the pet food industry. Proteins from insects, plants, and lab cultivation are becoming popular, particularly in North America and Europe where high-end pet nutrition trends are prominent.

Pet Food Ingredients Market Share, By Pet, 2025 (%)

| Segments | Shares (%) |

| Dog | 65% |

| Cat | 25% |

| Others | 10% |

Which Pet Held the Largest Share of the Pet Food Ingredients Market?

The dogs segment held the dominating share of the pet food ingredients market in 2025, because of the increased worldwide dog population, their greater food intake, and pet owners' strong inclination toward high-quality, health-oriented, and specialized dog foods. In the United States, there are around 78 million pet dogs that are owned and cared for by Americans. The growing trend of pet humanization and higher disposable incomes have boosted the demand for premium dog food, leading to an increase in the market for specific ingredients such as proteins, probiotics, and various functional additives.

The Cats Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Fueled by a rise in cat ownership in cities, a heightened demand for specialized and premium cat food, and an increasing awareness of specific feline health requirements. Currently, cat ownership worldwide surpasses that of dogs, with a higher percentage of men owning cats (52% male compared to 48% female). Cats thrive in apartments, leading to a rise in their adoption, which subsequently boosts the demand for high-quality, functional ingredients that meet their specific dietary needs, including those related to digestive and urinary health.

Charm Pet Food

IFF

Leaft Foods

DuPont

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches/Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

Recent News & Strategic Updates

By Ingredient Type

By Pet

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Pet Food Ingredients Market