April 2026

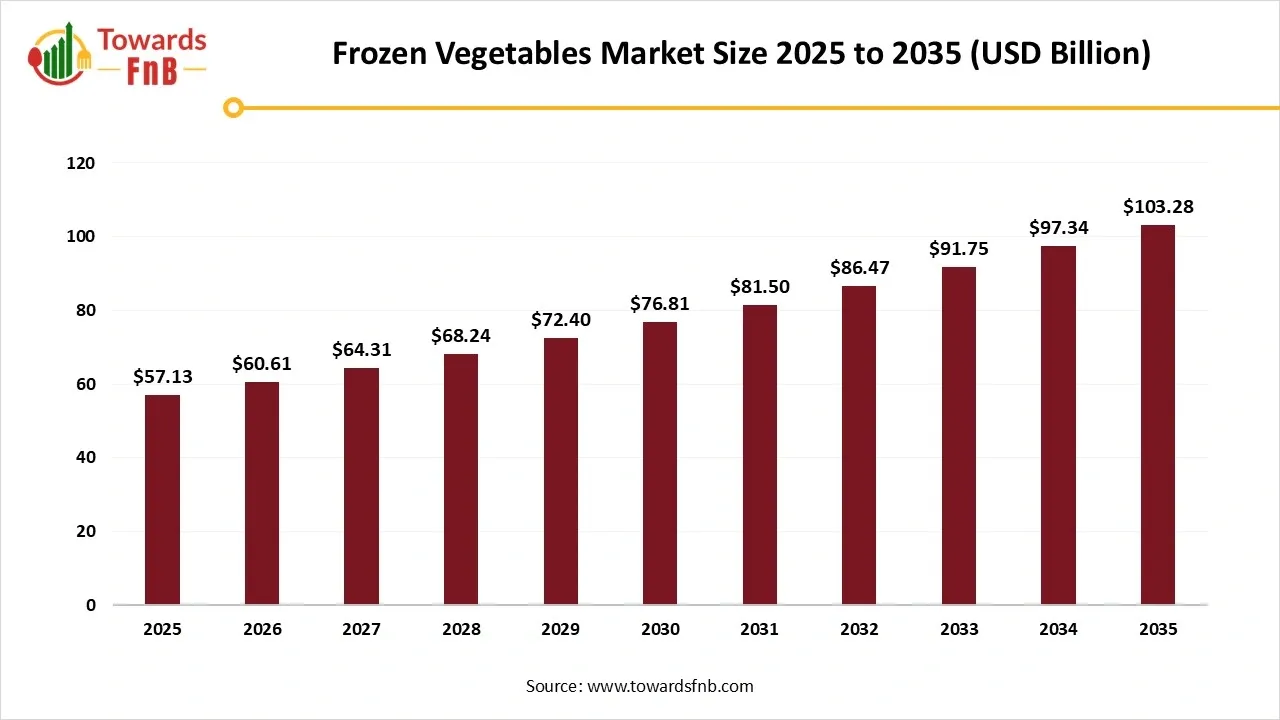

The global frozen vegetables market size reached at USD 57.13 billion in 2025 and is anticipated to increase from USD 60.61 billion in 2026 to an estimated USD 103.28 billion by 2035, witnessing a CAGR of 6.1% during the forecast period from 2026 to 2035. The availability all year around and the protection against uncertain price surges expands the market reach of frozen food products.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.1% |

| Market Size in 2026 | USD 60.61 Billion |

| Market Size in 2027 | USD 64.31 Billion |

| Market Size by 2035 | USD 103.28 Billion |

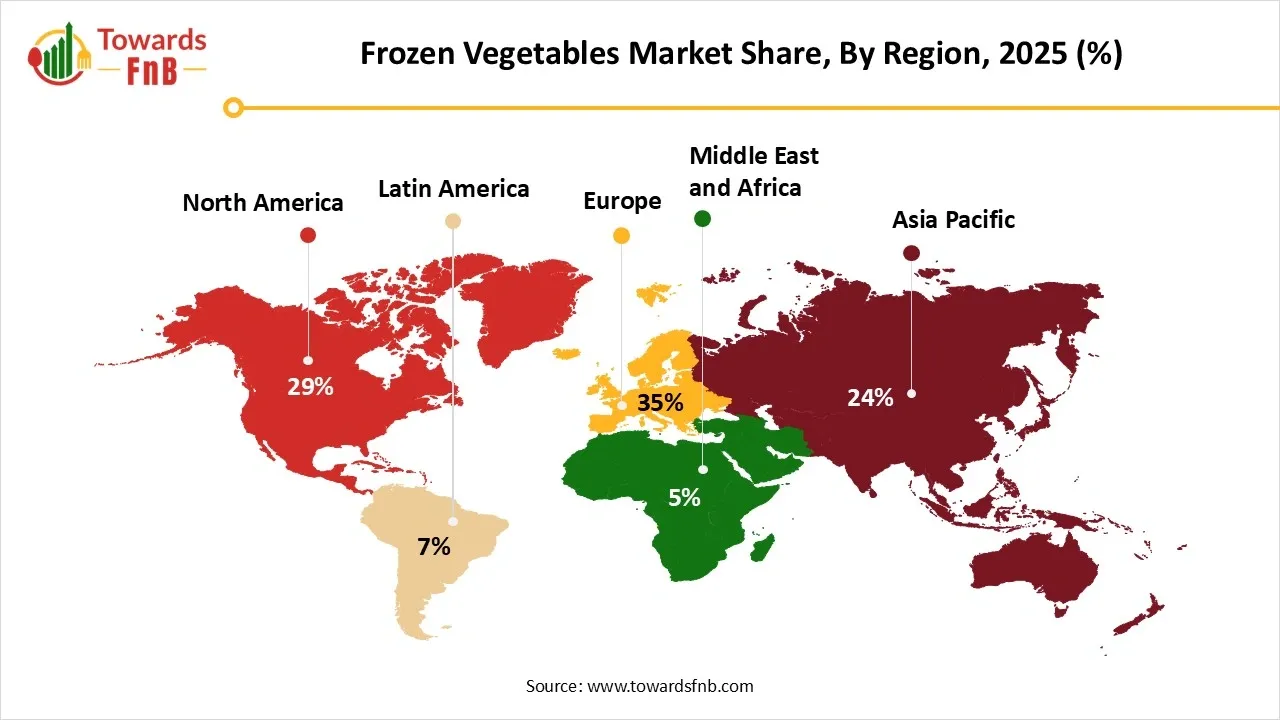

| Largest Market | Europe |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Frozen vegetables are vegetables that have been cleaned, cut, blanched, and quickly frozen at their peak ripeness to preserve their nutritional value, texture, and flavour. They are stored and distributed in a frozen state to extend shelf life and maintain quality until consumption. The frozen vegetables market encompasses different types of chilled and preserved vegetables, such as frozen spinach, frozen broccoli, frozen peas, frozen cauliflower, frozen mixed vegetables, and other vegetables. The increased demand for fast meal preparations and ready-to-eat meals by vegans and vegetarians raises the importance of the frozen food industry. The greater preferences for seasonal vegetables and organic food are creating new opportunities in the frozen vegetable industry. Frozen veggies are considered as the future of nutrient-rich intake. These vegetables allow us to achieve portion control and nutrient-rich meal preparations.

In March 2024, BigBasket announced the launch of a frozen foods brand named Precia in collaboration with Sanjeev Kapoor to meet the growing demand for convenient and high-quality meal solutions. (Source: Retail.com-From The Economic Times)

Frozen Vegetable Products by Ardo Group

| Sr. No. | Name of the Product |

| 1 | Diced peppers green |

| 2 | Diced aubergines |

| 3 | Cut green beans 0.5 inch |

| 4 | Sliced bamboo |

| 5 | Diced broccoli |

| 6 | Courgettes diced |

| 7 | Diced peppers yellow |

| 8 | Diced celeriac Organic |

| 9 | Cut leeks Organic |

| 10 | Diced onions Organic |

(Source: ardo)

New Policy Initiatives of India in Agriculture Sector

| Sr. No. | Name of the Program | Benefits |

| 1 | Clean plant Programme | Approved by the Union Cabinet in August 2024 with allocation of Rs. 1765.67 Crore. |

| 2 | Digital Agriculture Mission | Approved by the Union Cabinet in September 2024 by allocating Rs. 2817 Crore and the central share of Rs. 1940 Crore. |

| 3 | Progressive expansion of Agriculture Infrastructure Fund Scheme | Approved by the Union Cabinet in August 2024 to establish a strong agricultural infrastructure. |

| 4 | National Mission on Edible Oils – Oilseeds (NMEO-Oilseeds) | Approved by the Union Cabinet in October 2024 with an amount of Rs.10,103 Crore. |

| 5 | National Mission on Natural Farming | Approved by the Union Cabinet in November 2024 with an amount of Rs.2481 Crore. |

(Source: PIB.GOV)

The growing consumer preferences towards health, sustainability, and convenience help exporters to align their market strategies with emerging needs. The increased export volumes are driven by partnerships with international retail chains and food service companies. The collaborations between companies are increasingly focusing on the development of co-branded products which leads to increased consumer trust in foreign markets. With the expanding urbanization and changing lifestyles, regions such as Latin America, Africa, and Southeast Asia witness a significant demand for frozen food products.

The various issues such as temperature control, seasonal fluctuations, and logistics impact agricultural production to distribution and retail, which also cause a complex flow of goods. Efficient logistics can result in great losses in the quality of products and costs. These factors raise the importance of a strong supply chain strategy in the frozen vegetables market.

How Europe Dominated the Frozen Vegetables Market in 2025?

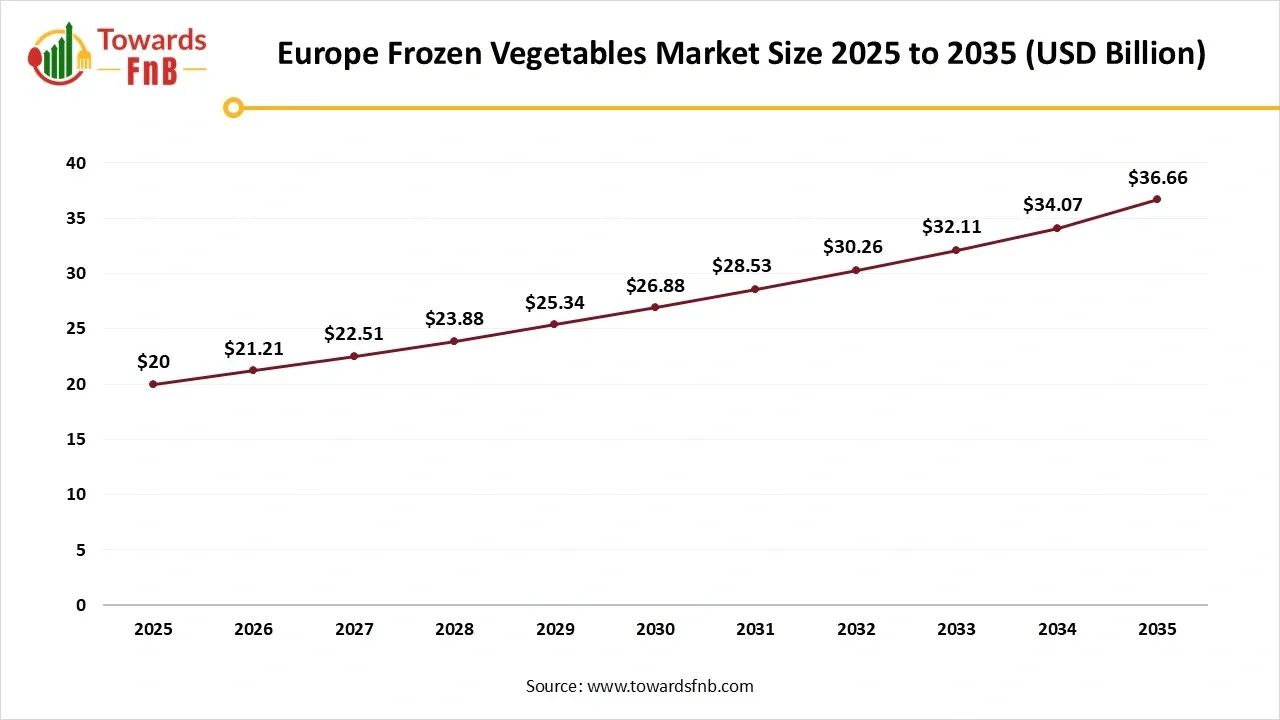

Europe dominates the frozen vegetables market in 2025. Europe remains an interesting market for frozen vegetables due to the increased imports and increased import prices over the past few years. Research suggests that this European market will increase at a significant annual growth rate over the next five years. The major rationales behind the market’s growth rate are increased convenience and consumption of ready-to-eat frozen food. The growing popularity of vegan and vegetarian food across Europe drives the increased consumption of both fresh and frozen vegetables. Europe is the largest producer of chilled and preserved vegetables in the world, due to which it holds a large share of internal trade in the total imports.

Europe Frozen Vegetables Market Size 2025 to 2035

The Europe frozen vegetables market size was valued at USD 20 billion in 2025 and is anticipated to increase from USD 21.21 billion in 2026 to an estimated USD 36.66 billion by 2035, witnessing a CAGR of 6.25% during the forecast period from 2026 to 2035.

However, Germany and France are the most fascinating markets for preserved vegetables among all other European countries. The United Kingdom is also an interesting market because it ranks first in imports from developing countries. Belgium is the largest producer and exporter, while it sources some frozen edibles from other countries. Several other top European markets are Italy, Portugal, Sweden, Spain, and the Netherlands.

How does Belgium Represent itself as the Leading European Producer of Frozen Vegetables?

Belgium is the largest producer, exporter, and re-exporting country of frozen vegetables in Europe. The major export destinations for frozen staples from Belgium are France, Germany, the United States, the United Kingdom, and the Netherlands. Belgium's exports of these products increased by 10% every year over the past five years. Belgium's production of frozen staples has expanded mainly in the regions of West Flanders and East Flanders, which focuses majorly on beans, spinach, carrots, cauliflower, peas, and Brussels sprouts.

What Makes Asia Pacific the Fascinating Market for Frozen Vegetable Producers and Suppliers?

Asia Pacific is expected to grow at the fastest CAGR in the frozen vegetables market during the forecast period. The leading Asian Pacific countries like Singapore totally rely on imports of food products. The food laws in Singapore mainly focus on ensuring a continuous foreign supply of safe agricultural food and related products. The Singapore Food Agency (SFA) is responsible for all food-related regulations in the country under the Ministry of the Environment and Water Resources. The major growth factors for the Asia Pacific region are the growing demand for food products, competitive advantages for industries, government support, and favorable opportunities. India is the largest producer of spices, milk, fruits, vegetables, meat, and poultry. The enhanced accessibility to natural resources offers several advantages to industries in the food processing sector. The presence of diverse agro-climatic conditions and many raw materials offers several opportunities for food processing industries.

In June 2024, the Ministry of Food Processing Industries announced the approval of 41 mega food parks, 76 agro-processing clusters, 399 cold chain projects, 588 food processing units, 52 operation green projects, and 61 projects related to the creation of backward and forward linkages under Pradhan Mantri Kisan SAMPADA Yojana (PMKSY). (Source: IBEF)

What are the Government Initiatives of India in the Food Processing Sector?

The Government of India launched the Pradhan Mantri Kisan SAMPADA Yojana (PMKSY) scheme, aiming to establish well-developed and modern infrastructure and streamline supply chain management from agriculture to the retail sector across the food processing area. This scheme focuses on increasing farmers’ returns, doubling their incomes, creating jobs in rural areas, decreasing farming wastage, enhancing food processing levels, and boosting exports of processed food. It has also launched the ‘Integrated Cold Chain and Value Addition Infrastructure” scheme to create continuous cold chain facilities like pre-cooling, storage, and distribution from agriculture to consumers. In the Union Budget 2025-26, there was an allocation of Rs. 4,364 crore (US$ 505.70 million) to the Ministry of Food Processing Industries (MoFPI).

")

What Made North America the Agricultural Powerhouse?

North America is seen to grow at a notable rate in the frozen vegetables market in 2024. The Northern American countries like the U.S. and Canada are leading in the trade of canola oil, fruits, vegetables, chocolate, frozen fries, beef and pork, food preparations, grain alcohol, corn, baked goods, etc. The North American agricultural sector in the U.S., Mexico, and Canada received several benefits due to the North American Free Trade Agreement (NAFTA) and the U.S.- Mexico-Canada Agreement (USMCA). North America is a remarkable producer of agricultural products rather than a consumer. The growing willingness of consumers in countries like Japan, China, East Asia, South Korea, and the European Union to pay premiums for high-quality goods such as meat and fresh fruits from North America drives regional success.

Why did the U.S. Transition to Organic Production through Investments, Partnerships, and New Programs?

In May 2024, the agricultural secretary of Washington DC announced an additional $10 million in funding along with grant awards, new programs, and partnerships for the expansion of the market for organic products and assist producers’ transition to organic production. These programs reduce the financial burden of achieving organic certification and boost the production of organic products. The U.S. is the largest agricultural trading partner of Mexico with the leading U.S. farm exports of corn, dairy products, soybean, and pork to Mexico in 2024. Mexico is the largest supplier of strawberries, tomatoes, and avocado to the U.S.

Frozen Vegetable Market in Middles East and Africa is Growing Notably

The rising middle-class population and increasing disposable income in the Middle East and Africa contribute to enhanced consumer purchasing power and a growing inclination towards a diverse range of frozen vegetables, including premium and exotic varieties. The expansion of supermarket chains and the development of cold chain infrastructure across the region have also made frozen vegetables increasingly accessible. Moreover, there is a notable rise in the production and consumption of organic produce in specific countries, such as Saudi Arabia, Kuwait, and the United Arab Emirates.

The growth of the frozen vegetable market in the United Arab Emirates is primarily driven by heightened consumer demand for convenience foods, urbanization, and busy lifestyles that favor quick meal solutions. The increasing health consciousness among consumers further supports the adoption of frozen vegetables, which are perceived as nutritious and capable of preservation. Additionally, the expanding retail sector, encompassing supermarkets and hypermarkets, facilitates greater access to frozen products.

How Single Vegetables Segment Dominated the Frozen Vegetables Market in 2025?

The single vegetable segment dominated the frozen vegetables market with a 35.6% market share in 2025. A diet rich in vegetables and fruits helps to lower blood pressure and avoids the risk of stroke or heart disease. They can have a positive impact on eye health and digestive health. They avoid the risk of diabetes and cancer and help to manage weight.

The Mixed Vegetables Segment is Expected to Grow at the Fastest CAGR in the Frozen Vegetables Market During the Forecast Period

The mixed vegetables offer improved vision, improved gastrointestinal health, and enhanced immunity. Certain vegetables such as leafy greens, cruciferous vegetables, red vegetables, orange and yellow vegetables, and legumes are good sources of beta-carotene, protein, vitamins, minerals, which reduce the risk of certain cancers.

Frozen Vegetables Market Share, By Freezing Technique, 2025 (%)

| Segments | Shares (%) |

| Individual Quick Freezing (IQF) | 55.43% |

| Blast Freezing | 15% |

| Belt/Tunnel Freezing | 10% |

| Cryogenic Freezing | 10% |

What Made Individual Quick Freezing (IQF) the Dominant Segment in the Frozen Vegetables Market in 2025?

The individual quick freezing (IQF) segment dominated the frozen vegetables market with a 55.43% share in 2025 and is seen to sustain that position during the forecast period. The extensive industrial applications of IQF for freezing vegetables, fruits, and berries in both diced and sliced forms raise its importance in the market. The IQF holds promising applications across various industries related to seafood, processing meat and poultry processing, dairy, and ready-to-eat meals.

The Cryogenic Freezing Segment is Seen to Grow at a Notable Rate in the Frozen Vegetables Market in 202

Cryogenic freezing is advantageous in keeping a constant temperature, preserving the taste and quality of products, increasing the shelf life of products, and improving production efficiency. It ensures savings, cost reduction, maintenance, cleanliness, and environmental sustainability.

Frozen Vegetables Market Share, By End User, 2025 (%)

| Segments | Shares (%) |

| Household Consumers (B2C) | 25% |

| Foodservice Sector (B2B) | 41.3% |

| Restaurants | 12% |

| Hotels | 8% |

| Cafés | 7% |

| Catering Services | 3% |

| Food Processing Sector | 4% |

How did the Foodservice Sector (B2B) Dominate the Frozen Vegetables Market in 2025?

The foodservice sector (B2B) segment dominated the frozen vegetables market with a 41.3% market share in 2025. B2B food marketplaces offer access to a wider audience, reduced marketing and sales costs, efficiency, and automation. The B2B foodservice sector scales up businesses by expanding its customer base, improving profit margins, and streamlining transactions.

The Household Consumers (B2C) Segment is Expected to Grow at the Fastest CAGR in the Frozen Vegetables Market During the Predicted Timeframe

Household consumers benefit from frozen food because they are economical meal solutions, they have a longer shelf life, they can cut down on waste, and help make produce easy to consume. These consumers can save money by finding economical food options.

Frozen Vegetables Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Retail Channels (serving B2C) | 40% |

| Supermarkets & Hypermarkets | 15% |

| Convenience Stores | 10% |

| Online Retail | 5% |

| Foodservice & B2B Channels (serving B2B) | 60.12% |

| Foodservice Distributors | 20% |

| B2B/Wholesale Distributors | 20% |

| Institutional Supply | 20% |

How Foodservice & B2B Channels (serving B2B) Segment Dominated the Frozen Vegetables Market in 2025?

The foodservice and B2B channels (serving B2B) segment dominated the frozen vegetables market with a 60.12% market share in 2025. The B2B channels serve as additional channels to reach unknown buyers. They allow global visibility and cross-sell opportunities on the leading B2B platforms.

The Retail Channels (Serving B2C) Segment is Expected to Grow at the Fastest CAGR in the Frozen Vegetables Market During the Forecast Period

The specific B2C channels offer benefits such as extended shelf life of products, reduced waste, cost-effectiveness, cost savings, time savings, nutritional value, and versatility in cooking. These advantages make food services or food products popular choices for potential consumers.

Iceland Foods Ltd

McCain Foods Limited

By Vegetable Type

Single Vegetables

Mixed Vegetables

Leafy Greens

Root Vegetables

Legumes

Others

By Freezing Technique

By End User

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Frozen Vegetables Market