April 2026

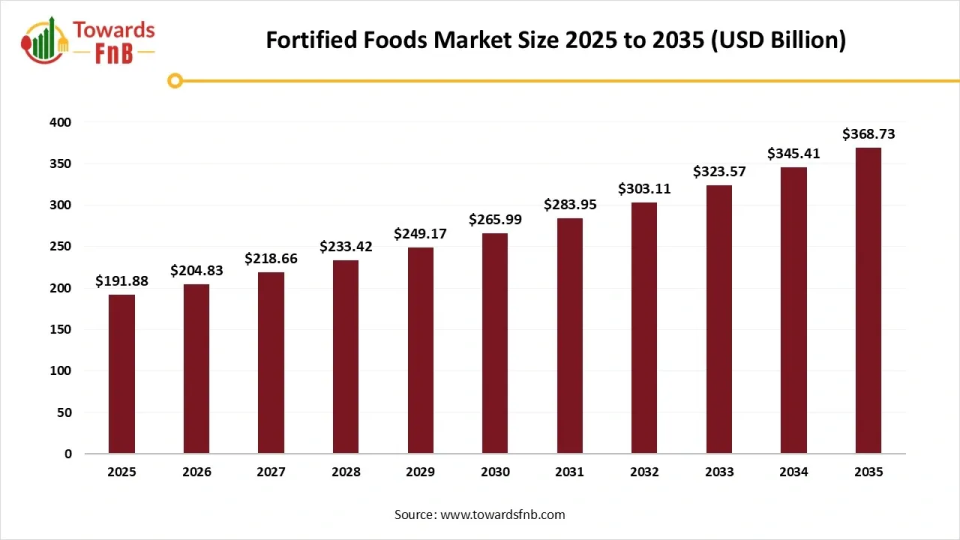

The global fortified foods market size reached at USD 191.88 billion in 2025 and is anticipated to increase from USD 204.83 billion in 2026 to reach nearly USD 368.73 billion by 2035, growing at a CAGR of 6.75% during the forecast period 2026 to 2035. Market is driven by increasing health consciousness, rising demand for convenient and nutritious products, and government efforts to combat malnutrition.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.75% |

| Market Size in 2026 | USD 204.83 Billion |

| Market Size in 2027 | USD 218.66 Billion |

| Market Size by 2035 | USD 368.73 Billion |

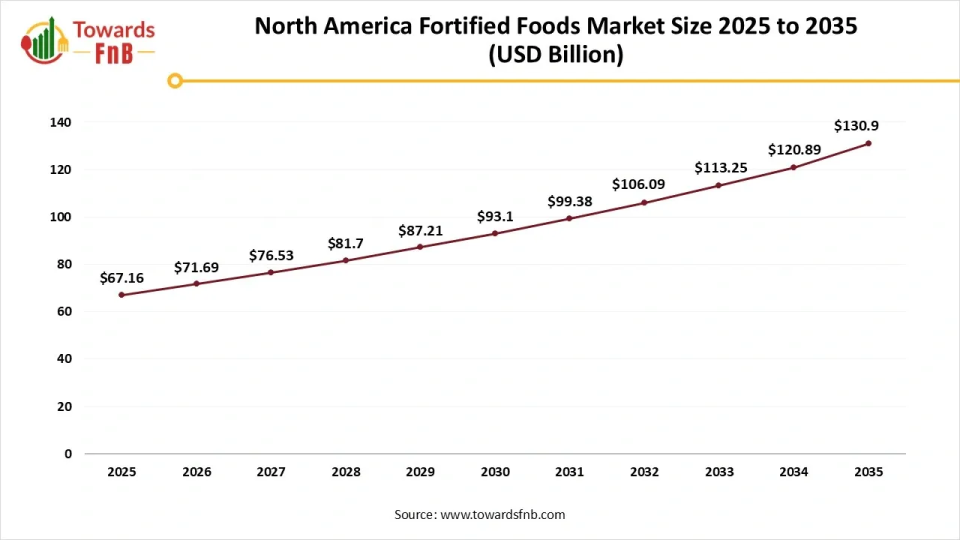

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The market for fortified foods encompasses the manufacturing and selling of food items enriched with vitamins, minerals, and additional nutrients. The main objective is to tackle nutrient shortages, enhance public health, and boost the nutritional quality of staple or processed food. Food fortification can enhance lives, particularly when numerous families struggle to access a balanced diet. Currently, around 3 billion individuals – 37% or more of the global population experience various forms of micronutrient deficiency.1 Insufficient intake of vital micronutrients like folate, iodine, iron, vitamin A, or zinc can result in significant health issues. The market is expanding because of rising health awareness and public health efforts aimed at combating malnutrition.

The sector will change through the strength of breakthroughs in bio fortification, tailored nutrition, and AI-driven food innovation. Customized fortification, tailored to an individual’s dietary needs, will increase, driven by microbiome knowledge and DNA-informed nutrition assessment. Advancements in encapsulation and nano-delivery technologies will enhance nutrient absorption and stability. Novel technologies such as genetic biofortification, nanoencapsulation, cold plasma processing, edible coatings, and 3D food printing have enhanced nutrient stability, bioavailability, and delivery efficacy.

Trade of Fortified Rice

Raw Material Procurement

Processing of Fortified Foods

Distribution of Fortified Foods

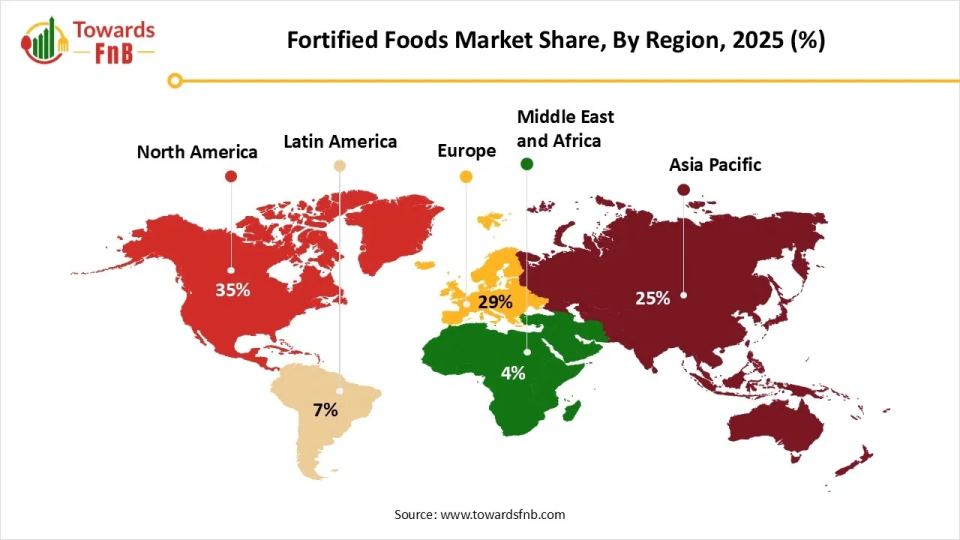

North America dominated the fortified foods market in 2025. The rising consciousness about health and the occurrence of lifestyle-related diseases fuel the need for fortified food and beverages products in North America. Increasing health consciousness prompts consumers to focus on wellness and proper nutrition, with enhanced products significantly contributing to remedying nutritional gaps and fostering improved lives. The National Institutes of Health (NIH) reports that almost 60% of American adults suffer from at least one chronic condition, highlighting the need for preventive dietary measures. This health-focused atmosphere is enhancing the fortified foods market.

North America Fortified Foods Market Size 2025 to 2035

The North America fortified foods market size was valued at USD 67.16 billion in 2025 and is anticipated to increase from USD 71.69 billion in 2026 to reach nearly USD 130.9 billion by 2035, growing at a CAGR of 6.9% during the forecast period 2026 to 2035.

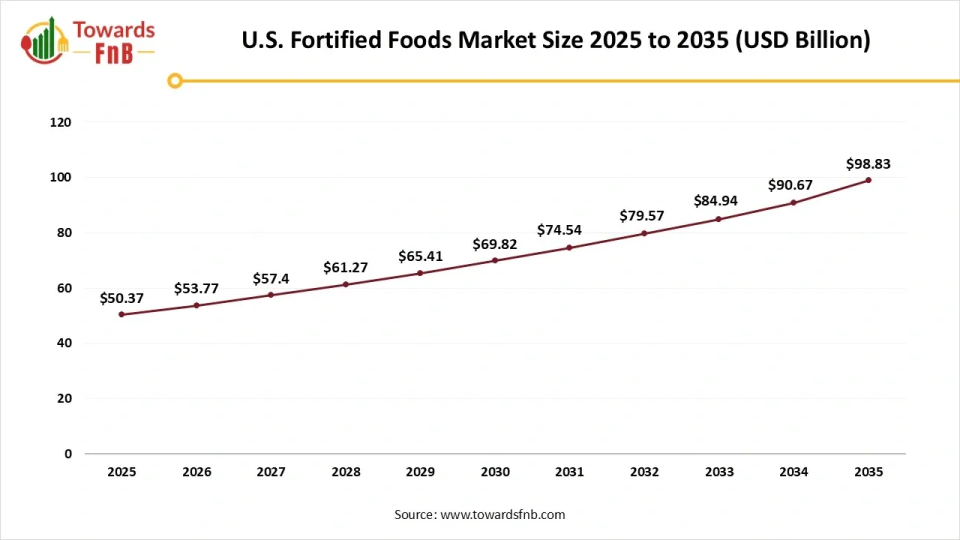

U.S. Fortified Foods Market Trends

U.S. fortified foods market is driven by strong consumer knowledge, wide-ranging product availability, and solid regulatory backing. The nation possesses an extensive background in food fortification initiatives, including the addition of folic acid to cereals to avert neural tube defects. The U.S. market features a strong demand for enriched food and drinks, especially among health-aware individuals and those aiming to remedy particular nutritional gaps.

U.S. Fortified Foods Market Size 2025 to 2035

The U.S. fortified foods market size was calculated at USD 50.37 billion in 2025 and is anticipated to increase from USD 53.77 billion in 2026 to reach nearly USD 98.83 billion by 2035, growing at a CAGR of 6.97% during the forecast period 2026 to 2035.

Growth of the Fortified Foods Market in Asia Pacific

Asia Pacific expects the fastest growth in the market during the forecast period. The market is primarily fueled by the rising health awareness among consumers and the numerous advantages of food fortification agents. Moreover, the increase in elderly populations and the escalating health issues have resulted in widespread use of food fortifying agents for multiple purposes. Key trends feature the inclusion of traditional herbs, the emergence of plant-based fortified options, and fortification programs spearheaded by governments, particularly in nations such as India and China.

India Fortified Foods Market Analysis

The market for fortified foods in India is propelled by growing health consciousness, a rise in micronutrient deficiencies, and government efforts to encourage fortified staples. Urban growth and evolving lifestyles drive the need for convenient, nutrient-dense foods, while increasing disposable income facilitates the adoption of premium products. The Indian government has introduced multiple initiatives for fortified foods, with the most notable being the nationwide rollout of fortified rice distribution across all government welfare programs by March 2024. This effort is also a component of the larger Anemia Mukt Bharat initiative, which encourages fortified products such as double-fortified salt and cooking oil in programs like PM-POSHAN.

")

Leveraging Fortified Foods Market of Europe

The Europe fortified foods market features a well-established consumer demographic with increased health awareness and strict regulatory requirements enhancing product safety and effectiveness. Nations like Germany, France, and the UK are at the forefront of embracing fortified products, motivated by rising rates of nutritional deficiencies and a transition towards preventive health measures. Specifically, the European Food Safety Authority (EFSA) discovered that around 80% of consumers in Europe are prepared to spend more for fortified foods, particularly those containing functional ingredients that enhance immunity and digestive well-being.

Germany Fortified Foods Market Analysis

In Germany, the demand for fortified foods is fueled by a growing awareness of health, a pursuit of preventive nutrition, and a need for products that aid in particular health issues such as immunity, digestive health, and energy levels. Germans are growing increasingly positive regarding the cost-of-living crisis and their financial situations, opening up opportunities for brands to reach wealthier consumers. Items that aid concentration are highly sought after by young, career-focused Germans. Certain groups within the population have been identified as having inadequate consumption of specific nutrients such as folate or vitamin D, leading to a demand for fortified products to address these deficiencies.

Expanding Market of Fortified Foods in Middle East and Africa

Expansion is fueled by increasing recognition of hidden hunger, enabling regulations, and incorporation of premixes in basic and packaged food. Urban growth and the rise of contemporary retail are enhancing the accessibility of fortified SKUs, while government purchasing pathways elevate volumes in social initiatives. Advancements in the stabilization of micronutrients and sensory neutrality allow for increased loading without affecting product quality. These elements generate chances for fortified items like flour, rice, oil, and salt to tackle problems such as anemia, vitamin A insufficiency, and neural tube defects, as well as to enhance general public health and wellness.

Saudi Arabia Fortified Foods Market

The market is undergoing consistent expansion, fueled by rising health consciousness and the need for nutrient-dense products. Increasing consumer demand for functional food that provide additional health advantages, like vitamins and minerals, is driving market growth. The increase in health-aware individuals and changing eating habits are also boosting Saudi Arabia's fortified foods market share.

Swiftly Expanding Fortified Foods Market of Latin America

The demand for fortified foods in Latin America is rising, fueled by greater health awareness, expanding government initiatives, and a shift from basic staples to more convenient options such as snack bars and dairy substitutes. Nations such as Costa Rica and Panama enforce mandatory rice fortification laws, while countries like Nicaragua engage in considerable voluntary fortification, though the extent and execution differ throughout the area.

Brazil Fortified Foods Market

In Brazil, the demand for fortified foods is rising, fueled by heightened health awareness and the necessity to address malnutrition. Although the market is growing, especially with vitamins and probiotics, certain staple food fortification such as rice remains a niche market, experiencing slower growth potential due to consumer awareness and sensitivity to prices.

Fortified Foods Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Fortified Dairy Products | 50% |

| Fortified Cereals | 20% |

| Fortified Beverages | 17% |

| Fortified Snacks | 13% |

Which Product Type Segment Dominated the Fortified Foods Market?

Fortified dairy products segment led the fortified foods market in 2025. A significant trend is the increasing interest in dairy items fortified with vitamins like A and D, minerals such as iron and calcium, and omega-3 fatty acids. This trend is driven by an increasing population with nutritional shortages and a wish to actively enhance general health and wellness. Moreover, the growing elderly demographic is a major factor in demand.

Fortified snacks segment is observed to grow at the fastest rate during the forecast period, because of the need for convenience, increasing health awareness, and the adaptability of snacks. Shoppers are looking for convenient meals that provide extra nutritional benefits, and producers have effectively added vitamins, minerals, and proteins to numerous snacks such as bars, chips, and other quick foods.

Fortified beverages segment is growing at notable rate. The increasing popularity of fortified drinks is mainly influenced by changing dietary habits, heightened awareness of micronutrient shortages, and a rising inclination towards clean-label, plant-based, and low-calorie products that provide additional functional benefits.

Fortified Foods Market Share, By End User, 2025 (%)

| Segments | Shares (%) |

| Infants | 10% |

| Children | 17% |

| Adults | 60% |

| Elderly | 13% |

Which End User Segment Dominated the Fortified Foods Market?

Adults segment held the dominating share of the fortified foods market in 2025, due to a substantial adult population, a high occurrence of lifestyle diseases such as obesity and diabetes, and a growing awareness of preventive healthcare. The significant group of health-conscious working professionals and fitness enthusiasts also fuels the need for fortified products.

Elderly segment is seen to grow at a notable rate during the predicted timeframe, due to age-related physiological alterations that heighten their susceptibility to malnutrition and nutrient deficits. This group is increasingly conscious of the impact nutrition has on their health, and many are proactively looking for strategies to manage or avert chronic diseases via their diet.

Infants segment is expanding at the notable rate during the forecast period, driven by increased parental awareness regarding infant nutrition, a rising interest in promoting early development, and the ease of access to specialized items such as fortified infant formula. Higher disposable incomes enable parents to invest more in high-quality baby food, while elements such as urban living, hectic schedules, and a growing number of working mothers boost the need for convenient and ready-to-serve choices.

Fortified Foods Market Share, By Nutritional Benefits, 2025 (%)

| Segments | Shares (%) |

| Vitamins | 50% |

| Minerals | 25% |

| Protein | 15% |

| Fibers | 10% |

Why did the Vitamins Segment Dominated the Fortified Foods Market?

Vitamins segment led the fortified ingredients market in 2025. Over the past decade, the vitamins sector has undergone a notable change driven by consumer demand for overall wellness and preventive healthcare. Rising prevalence of chronic diseases combined with a globally aging population has prompted individuals to include vitamins as vital elements of their daily health practices.

Protein segment is expected to grow at the fastest rate in the market during the forecast period, driven by heightened consumer awareness of its health advantages, resulting in strong demand for protein-rich foods that aid in muscle growth, weight management, and overall wellness. Producers are addressing this demand by enhancing various products, from sports nutrition to everyday goods, with protein to attract a wider audience.

Fiber’s segment growing significantly during the forecast period, driven by increasing consumer awareness of its digestive health advantages, the rising incidence of lifestyle-related diseases, and advancements in food science that simplify fortification. This transition is backed by consumers who are progressively looking for functional foods to enhance general wellness.

Which Distribution Channel Dominated the Fortified Foods Market?

Supermarkets segment held the largest share of the market in 2025, attributed to their extensive reach, convenience, and capacity to provide a comprehensive shopping experience. They offer a wide variety of fortified items, ranging from dairy to grains, addressing various consumer preferences and price points, and numerous customers rely on the quality and dependability of goods available in these well-known retail settings.

Online retail segment is observed to grow at the fastest rate during the forecast period, because of consumer ease, availability, and e-commerce's capacity to provide a broader and more tailored range. Digital platforms accommodate hectic lifestyles by offering home delivery and convenient access to items that can be difficult to locate in brick-and-mortar stores, while also enabling direct-to-consumer sales and the marketing of specialized products aimed at particular health requirements.

The health food stores segment expanding at significant rate. Health food stores represent an important avenue for niche and specialized fortified items, including those designed for dietary requirements. They serve a targeted consumer group that is more health-aware and ready to invest in functional and specialized food options.

Initiative

Idahoan Foods

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Over the years Nestlé has made numerous acquisitions to build scale and expand into new categories. For example:

Partnerships & Collaborations

Product Launches / Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

Recent News & Strategic Updates

By Product Type

By End User

By Nutritional Benefit

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Fortified Foods Market