April 2026

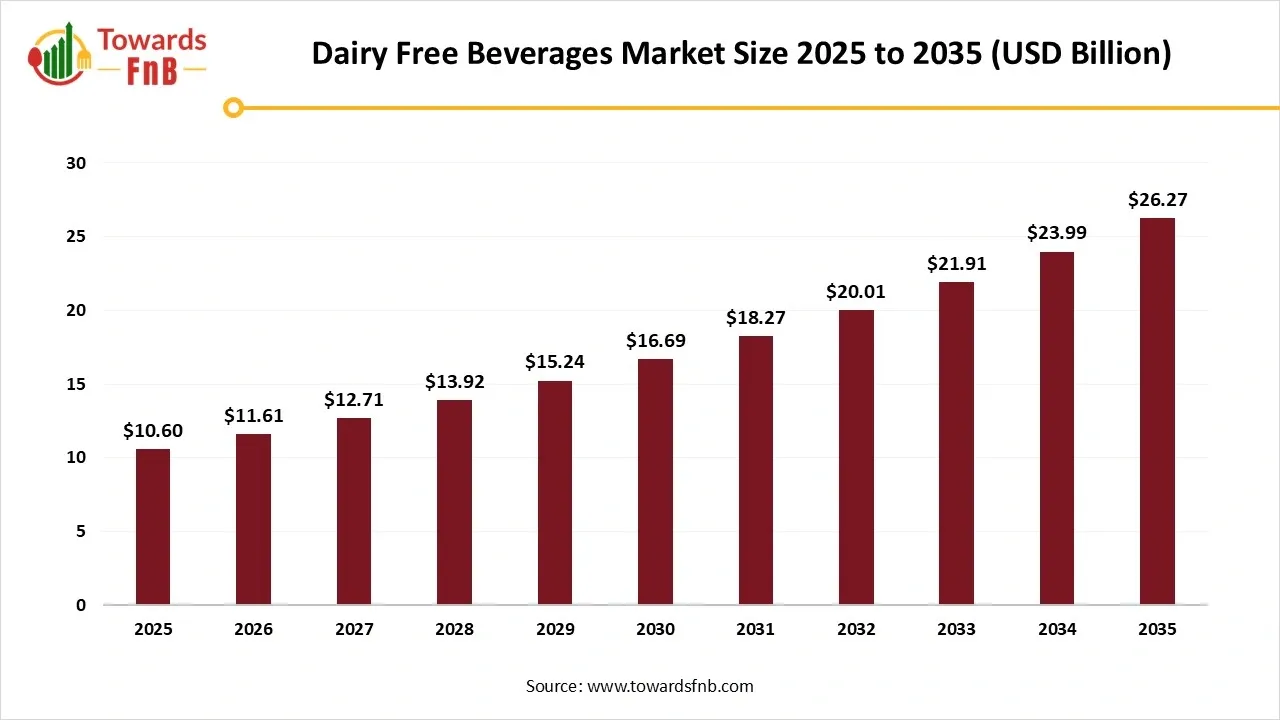

The global dairy free beverages market size reached at USD 10.60 billion in 2025 and is predicted to increase from USD 11.61 billion in 2026 to nearly reaching USD 26.27 billion by 2035, growing at a CAGR of 9.5% during the forecast period from 2026 to 2035. The market is witnessing rapid growth driven by rising consumer awareness about lactose intolerance, plant-based nutrition, and ethical consumption. As demand shifts toward healthier and sustainable alternatives, brands are innovating with a wide range of non-dairy milk and beverage products.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 9.5% |

| Market Size in 2026 | USD 11.61 Billion |

| Market Size in 2027 | USD 12.71 Billion |

| Market Size by 2035 | USD 26.27 Billion |

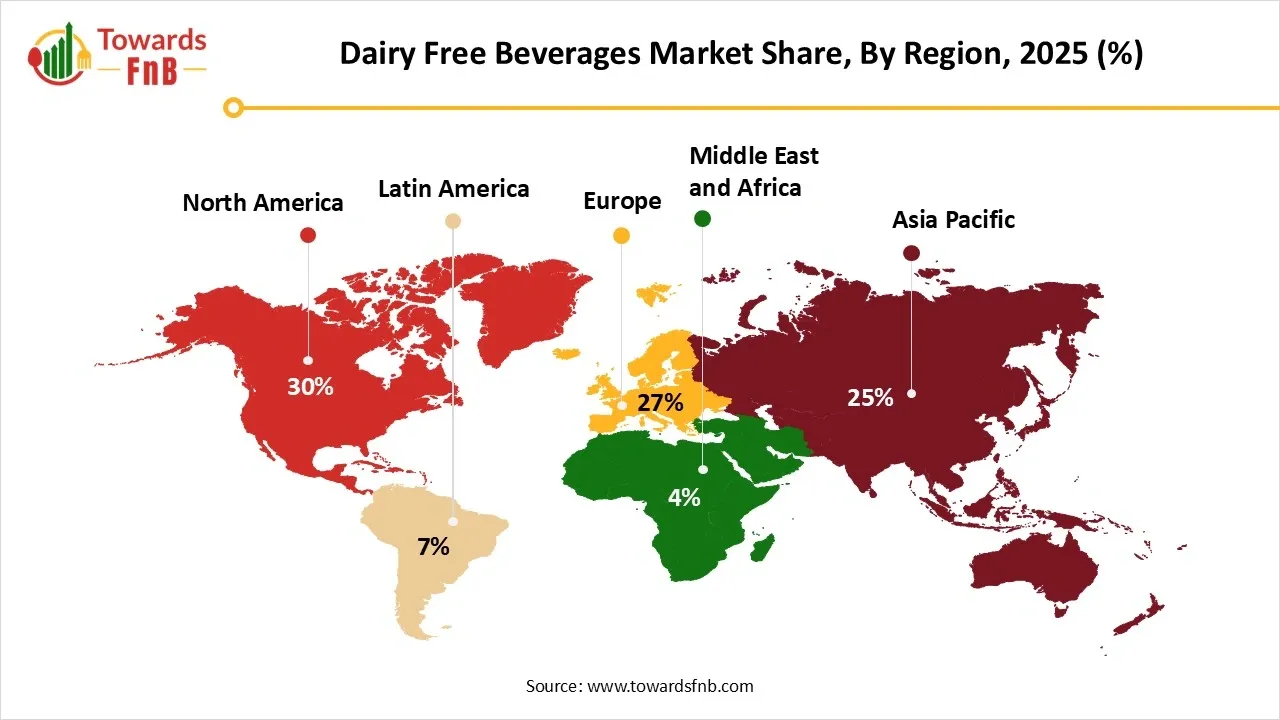

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The dairy free beverages market refers to the global industry comprising plant-based drinks that serve as alternatives to traditional dairy products. These beverages are typically made from plant sources such as soy, almonds, oats, coconuts, rice, and others. They are consumed by individuals who are lactose intolerant, vegan, allergic to dairy, or health-conscious. The market has expanded rapidly due to rising demand for clean-label, sustainable, and animal-free products.

Moreover, the global dairy free beverages market has evolved from a niche trend into a mainstream preference across diverse consumer groups. Fueled by increasing health consciousness, consumers are actively seeking alternatives to traditional dairy due to lactose intolerance, allergies, and vegan lifestyles. Almond, soy, oat, and coconut milk have become household staples, with new blends and Flavors expanding consumer choices. Retail shelves are now crowded with ready-to-drink plant-based beverages, protein-enriched options, and fortified drinks. Major food and beverages companies are heavily investing in product innovation and branding. Distribution has also broadened, with dairy-free drinks now available in convenience stores, cafes, supermarkets, and online platforms.

Customer Analysis (Target Audience And Techniques to Attract Customers)

| 18-24 years | 25-44 years |

| These consumers are more conscious about sustainability, animal welfare, and clear nutrition. Young adults are also more likely to follow flexitarian, vegan or dairy-limited diets. | The sleek high-protein and functional drinks as part of their routines. Meanwhile, families with young children and seniors are adopting dairy-free drinks for allergy management and digestive health. |

There is immense untapped potential in under-penetrated market’s particularly in several regions. With rising disposable incomes and global exposure, consumers in these regions are increasingly open to plant-based alternatives. Innovation in regional ingredients like rice milk in Southeast Asia or cashew milk in India presents exciting product development opportunities. Additionally, cafes, fast-food chains, and wellness brands are introducing dairy-free alternatives to their menus, boosting visibility. The growing online retail ecosystem allows even niche brands to scale rapidly. Collectively, these factors create a robust landscape for future investment and expansion.

Despite its growth, the dairy free beverages market faces notable challenges, particularly related to pricing and taste perception. Many plant-based beverages remain costlier than their dairy counterparts, limiting access in price-sensitive markets. Additionally, some consumers still view non-dairy drinks as less flavorful or less satisfying, especially when used in cooking or coffee. Shelf stability and product separation issues also pose technical hurdles for manufacturers. Limited consumer awareness in rural or traditionally dairy-heavy regions can slow adoption. Regulatory barriers concerning ingredient sourcing and labelling requirements may further complicate market entry. Overcoming these restraints will require innovation, education, and affordability.

Why is North America Sipping the Lead?

North America dominated the dairy free beverages market in 2025, due to strong consumer demand, awareness, and a mature health and wellness industry. A large percentage of the population is actively choosing plant-based diets, whether for ethical, environmental, or health-related reasons. Supermarkets, cafes, and restaurants widely stock and promote dairy-free alternatives, making them easily accessible. Celebrity endorsements and wellness influencers further amplify the shift toward non-dairy options. The market also benefits from a culture of early product adoption and innovation, where functional beverages like protein-enriched oat milk and probiotic almond drinks thrive. Moreover, regulatory standards for labelling and safety support consumer confidence, driving repeat purchases.

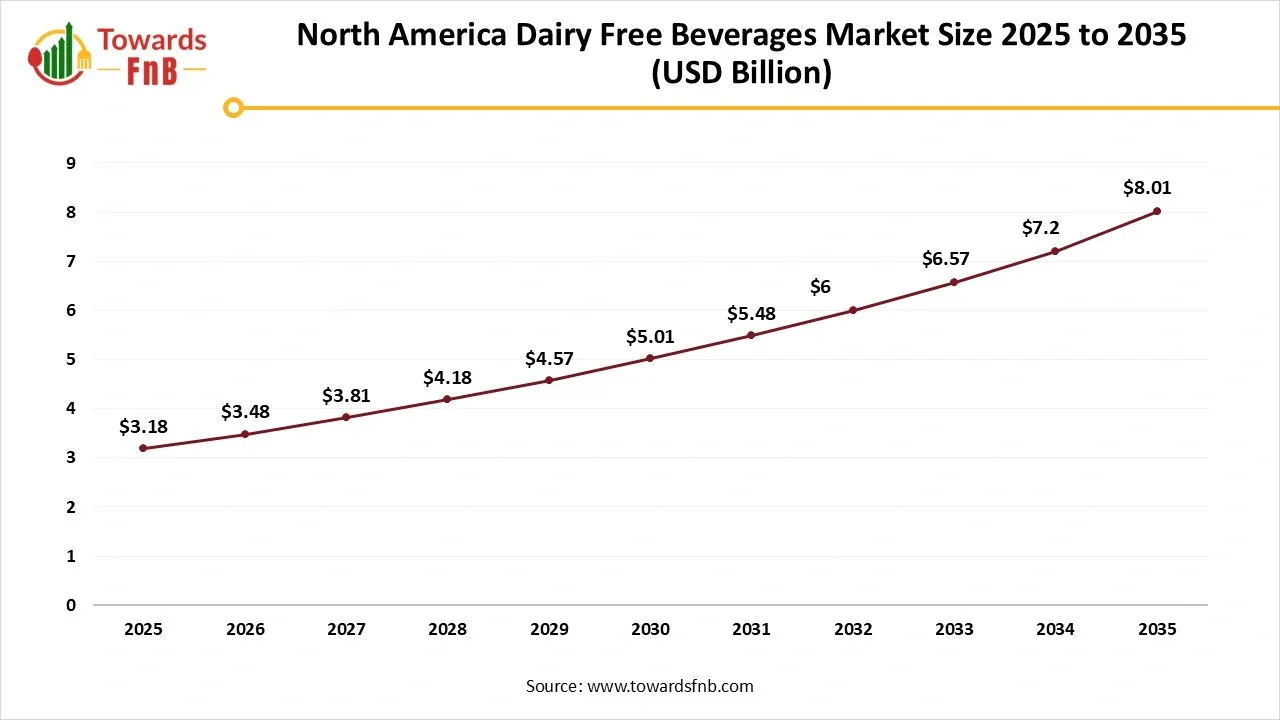

North America Dairy Free Beverages Market Size 2025 to 2035

The North America dairy free beverages market size was valued at USD 3.18 billion in 2025 and is predicted to increase from USD 3.48 billion in 2026 to nearly reaching USD 8.01 billion by 2035, growing at a CAGR of 9.68% during the forecast period from 2026 to 2035.

North America's diversity also plays a major role, with different ethnic groups embracing alternatives like coconut milk, rice milk, and soy drinks based on cultural preferences. The rise in lactose intolerance among Hispanic and African-American populations has added to the growing demand. Additionally, fitness and lifestyle trends like keto, vegan, and low-carb diets have opened new channels for dairy-free product formats like shakes and smoothies. Food service giants and coffee chains are pushing barista-grade dairy alternatives, making them a daily part of consumer life. Private-label and premium brands alike are expanding shelf presence in both brick-and-mortar and online channels. This strong infrastructure and evolving consumer habits keep North America firmly in the driver’s seat.

U.S. Dairy Free Beverages Market Trends

The U.S. market continues to grow rapidly as consumers increasingly seek plant-based, lactose-free, and allergen-friendly alternatives to traditional dairy products. Almond, oat, and soy milks remain the most popular segments, with innovation expanding into pea, rice, and mixed-plant blends that offer improved nutrition and taste profiles.

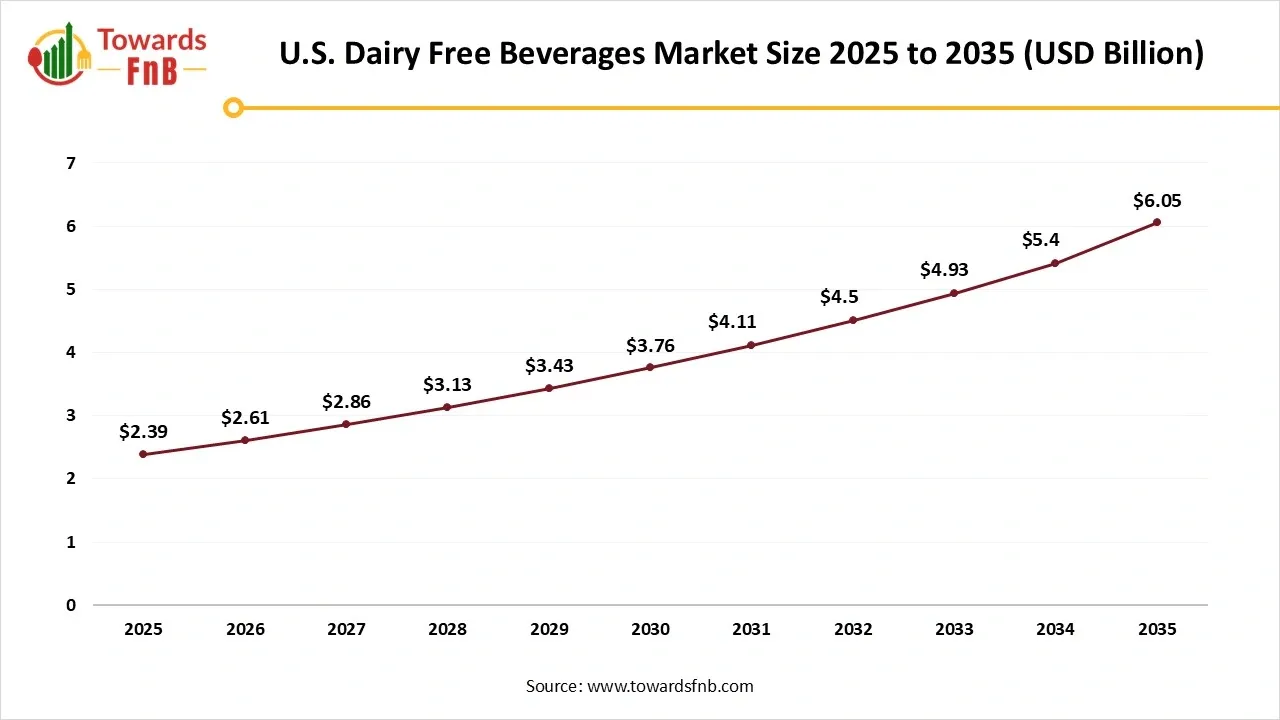

U.S. Dairy Free Beverages Market Size 2025 to 2035

The U.S. dairy free beverages market size was calculated at USD 2.39 billion in 2025 and is predicted to increase from USD 2.61 billion in 2026 to nearly reaching USD 6.05 billion by 2035, growing at a CAGR of 9.73% during the forecast period from 2026 to 2035.

Can Asia Pacific Redefine the Future of Dairy-Free Beverages?

Asia Pacific expects the fastest growth in the dairy free beverages market during the forecast period due to shifting dietary habits and increasing health consciousness. Urban populations are becoming more aware of lactose intolerance, especially in East and Southeast Asian countries, where milk digestion issues are more prevalent. Plant-based beverages are gaining popularity not only for their health benefits but also for cultural alignment with traditional non-dairy drinks like soy milk and rice water. As disposable incomes rise, consumers are willing to pay a premium for wellness products, especially those seen as “modern with ancient roots.” Local ingredients such as sesame, mung bean, and millet are now being reimagined into innovative dairy-free formats. These culturally adapted offerings resonate well with the local palate, driving rapid adoption.

The growth is further supported by the expansion of e-commerce, making plant-based options accessible even in tier-2 and tier-3 cities. Governments in some countries are also launching health campaigns that indirectly favor plant-based eating habits. Foodservice establishments, especially in urban areas, are beginning to offer dairy-free add-ons in coffee, bubble tea, and smoothies. Youth and young professionals in metro regions are adopting dairy-free drinks as part of their fitness and skincare routines. Additionally, regional start-ups are attracting investment by innovating with heritage grains and sustainable packaging. Asia-Pacific's combination of cultural openness, rising incomes, and growing awareness makes it a dynamic hotspot for future dairy-free growth.

China Dairy Free Beverages Market Trends

China's market is growing rapidly as consumers become more health-conscious and seek alternatives due to lactose intolerance and lifestyle preferences. Plant-based milks such as soy, oat, and almond are gaining popularity, supported by expanding product variety and improved taste and nutritional profiles.

")

European Initiatives in the Dairy Free Beverages Industry

The European dairy free beverages market is experiencing significant growth, driven by increasing health consciousness and a focus on sustainability. As consumers become more mindful of their dietary choices, there is a rising demand for alternatives to traditional dairy and animal-based products.

This shift is evident in the wide variety of offerings available, including nut milks, soy beverages, and oat-based drinks. In the UK, for instance, animal welfare has gained popularity, with consumers citing it as a reason for opting for plant-based dairy alternatives.

Germany Dairy Free Beverages Market Trends

In Germany, the dairy free beverages market is expected to continue its growth trajectory, fueled by strong consumer interest in sustainability, health, and ethical eating. The market benefits from a well-established foundation of plant milk products, especially oat milk, which has gained broad appeal due to its low environmental footprint and versatility.

As consumer awareness of the environmental disadvantages of traditional milk production continues to grow, perceptions of plant-based alternatives as more sustainable options are on the rise.

Dairy Free Beverages Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Soy Milk | 49% |

| Almond Milk | 25% |

| Oat Milk | 15% |

| Coconut Milk | 10% |

| Rice Milk | 5% |

| Others | 5% |

Why does Soy Milk Still Pour Ahead of the Pack?

Soy milk segment dominated the dairy free beverages market in 2025, due to its well-established history, affordability, and high protein content. It has been a go-to alternative for decades, especially for consumers seeking a closer nutritional profile to dairy milk. With a neutral taste and smooth texture, soy milk is widely accepted across diverse age groups and culinary uses. Its versatility makes it ideal for cooking coffee, and cereal, maintaining its stronghold in both household and foodservice segments. In many regions, soy milk also benefits from cultural familiarity, especially in Asian cuisines. Additionally, established supply chains and stable sourcing make it cost-effective for both producers and consumers.

Almond Milk Segment Expects the Fastest Growth in the Dairy Free Beverages Market During the Forecast Period

The segment is driven by its light taste, low-calorie appeal, and premium image. Consumers perceive it as a clean, refreshing alternative, especially those prioritizing weight management or sugar reduction. With growing concerns over allergens and soy sensitivities, almond milk serves as a safe and widely acceptable option. The rise in flavored, barista-style, and protein-fortified versions has also boosted its popularity across cafes and health-conscious households. In addition, almond milk aligns well with the lifestyle-driven choices of Gen Z and millennials. Marketing around sustainability and mindfulness living has positioned almond milk as more than just a drink; it is a statement.

Dairy Free Beverages Market Share, By Formulation, 2025 (%)

| Segments | Shares (%) |

| Plain/Unsweetened | 60% |

| Flavored/Sweetened | 40% |

Why Plain/Unsweetened Segment is Dominating the Dairy Free Beverages Market?

Plain or unsweetened dairy-free segment dominated the market in 2025, especially among health-focused and diabetic consumers seeking low-sugar options. These versions cater to those who prefer natural Flavors or want to use the beverage in cooking without altering taste. Diet-conscious buyers are increasingly turning toward zero-added-sugar drinks, making unsweetened variants the preferred choice. Brands are also fortifying plain beverages with essential nutrients like calcium and vitamin D to boost their health profile. These products are widely accepted by nutritionists and healthcare providers, further supporting their market position. From smoothies to sauces, the neutral base makes them versatile in daily consumption.

Flavored and Sweetened Dairy-Free Beverages Segment Expects the Fastest Growth in the Dairy Free Beverages Market During the Forecast Period

Driven by consumer demand for taste and variety. These drinks appeal to a younger audience seeking indulgence without guilt, often incorporating popular flavors like vanilla, chocolate, or berry. Brands are innovating with low-sugar or naturally sweetened versions using stevia, dates, or monk fruit. Coffee drinkers and kids especially favor these enhanced flavors, making them ideal for both breakfast and snack-time routines. The rise of on-the-go lifestyles is fueling demand for ready-to-drink, flavored plant-based beverages. This segment is not just about nutrition; it’s about experience and enjoyment.

Marketing campaigns around taste, fun, and energy are helping sweetened versions build strong brand loyalty. Limited-edition flavors and seasonal offerings also drawing interest and repeat purchases. In cafes and restaurants, flavored dairy-free alternatives are replacing traditional syrups or sweeteners, especially in lattes and smoothies.

Dairy Free Beverages Market Share, By Packaging Type, 2025 (%)

| Segments | Shares (%) |

| Cartons (Tetra Pak, etc.) | 55% |

| Bottles | 30% |

| Cans & Others | 15% |

Why are Cartons Still the Gold Standard?

Carton packaging segment dominates the dairy free beverages market in 2025. because of its convenience, sustainability, and long shelf life. Most consumers associate cartons with health drinks, reinforcing the product’s nutritious image. They are lightweight, easy to store, and ideal for both refrigerated and shelf-stable formulations. Brands also find it cost-effective to produce and transport in bulk. Cartons allow for attractive branding with clean, full-panel designs that appeal to modern buyers. Additionally, consumers perceive carton packaging as more eco-friendly, aligning with the plant-based ethos.

Bottled Dairy-Free Beverages Segment Expects the Fastest Growth of the Market During the Forecast Period

especially in the ready-to-drink (RTD) and on-the-go segments. They are particularly popular among fitness enthusiasts and busy consumers looking for functional beverages they can consume post-workout or during travel. Bottles offer easy grip, portability, and convenience qualities that align with modern lifestyles. Many bottles come with resealable caps, making them suitable for multiple uses throughout the day. As single-serve consumption rises, bottles provide portion control and freshness in one go. The visual appeal and clarity of transparent bottles also allow brands to showcase texture and color, building appeal.

Dairy Free Beverages Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Supermarkets & Hypermarkets | 50% |

| Online Retail | 25% |

| Health Food Stores | 10% |

| Convenience Stores | 15% |

Why do Supermarkets Still Rule the Dairy-Free Shelf?

Supermarkets and hypermarkets segment dominated the dairy free beverages market in 2025, due to their wide reach, product variety, and consumer trust. These outlets provide a tactile shopping experience where customers can compare ingredients, taste samples, and explore new flavors. The organized layout and clear categorization of plant-based products help simplify the buying process. Promotions, combo deals, and end-cap displays further drive visibility and sales. Supermarkets also cater to family shopping habits, where bulk and value packs of dairy-free beverages are often preferred. With large inventories and cold storage, they can easily stock a broad range of plant-based SKUs.

Online Retail Segment Expects the Fastest Growth in the Market During the Forecast Period

Thanks to digital convenience, customization, and reach. Consumers now prefer browsing and ordering from the comfort of home, especially for niche or specialty plant-based products. Subscription services, discounts, and personalized recommendations make online platforms attractive for regular buyers. E-commerce also enables smaller brands to reach audiences beyond physical store limits. With rising mobile usage and digital wallets, purchasing dairy-free drinks online has become seamless. Many platforms offer quick delivery, bulk discounts, and temperature-controlled packaging for perishables.

Dairy Free Beverages Market Share, By End Use, 2025 (%)

| Segments | Shares (%) |

| Household/Retail Consumption | 60% |

| Foodservice (Cafés, Restaurants, etc.) | 25% |

| Food & Beverage Industry | 15% |

Why Household/Retail Consumption Segment is Dominating the Dairy Free Beverages Market?

The household/retail segment dominated the market in 2025, driven by increasing health awareness and changing family dietary habits. Consumers are actively stocking plant-based milks and drinks at home for daily use, whether in cereals, smoothie, or coffee. The availability of multiple options like soy, almond, oat, and coconut milk in supermarkets makes it easy for families to incorporate them into regular routines. Parents are also choosing dairy-free options for children with allergies or sensitivities, further increasing household demand. Bulk packaging, long shelf life, and versatility of use support consistent in-home consumption. As more people cook and experiment at home, dairy-free beverages have become pantry staples.

Foodservice Segment Expects the Fastest Growth in the Market During the Forecast Period

As cafes, restaurants, and quick-service chains are increasingly catering to evolving customer preferences. From almond milk lattes to coconut-based smoothies and oat milk desserts, plant-based options are becoming menu essentials. The demand for dairy-free add-ons is especially high in urban cafes and specialty tea shops. Hospitality brands are using these beverages to differentiate and appeal to health-conscious and vegan customers. With rising customization trends, customers now expect a non-dairy option whenever milk is traditionally used. As consumer dining habits shift towards experience and wellness, foodservice adoption is fueling the next wave of growth.

Country Delight

Slice

By Product Type

By Formulation

By Packaging Type

By Distribution Channel

By End Use

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

March 2026

March 2026

Dairy Free Beverages Market