April 2026

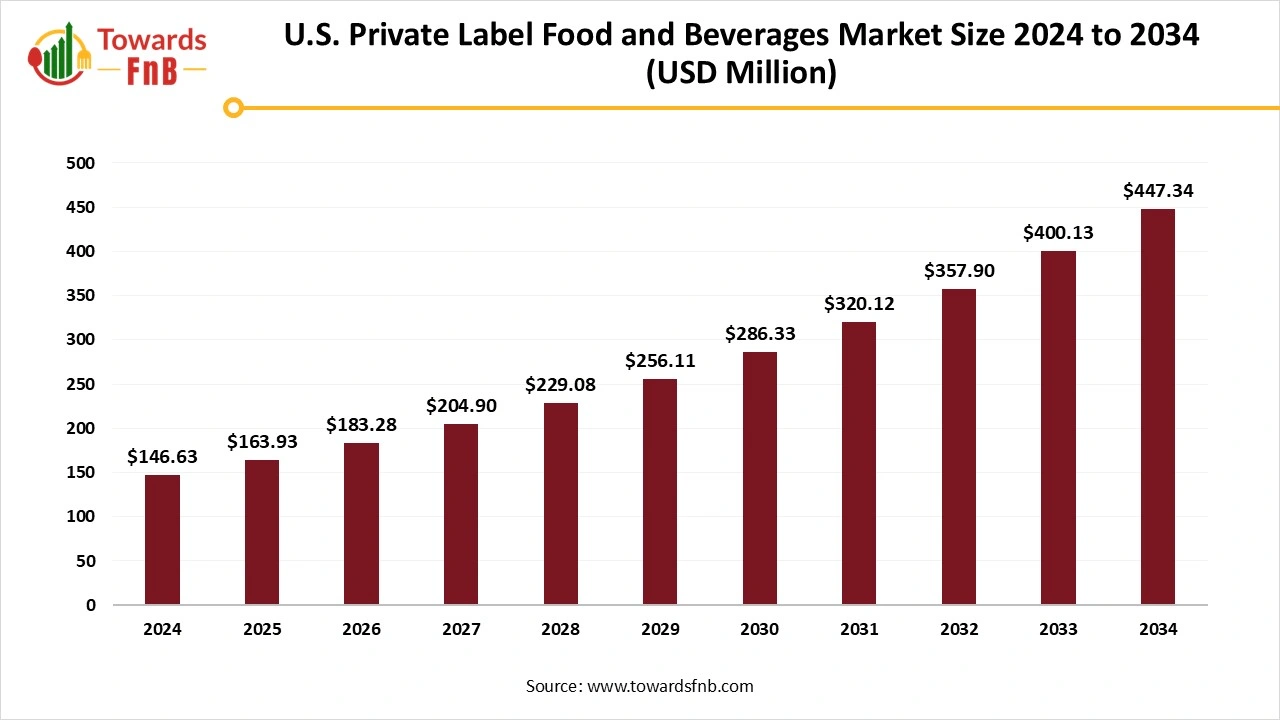

The U.S. private label food and beverages market size stood at USD 146.63 million in 2024 with projections indicating a rise from USD 163.93 million in 2025 to approximately USD 447.34 million by 2034, expanding at a CAGR of 11.8% throughout the forecast period from 2025 to 2034. The increasing product innovation and consumer trust drives the growth of the market.

| Study Coverage | Details |

| Growth Rate from 2025 to 2034 | CAGR of 11.8% |

| Market Size in 2025 | USD 163.93 Million |

| Market Size in 2026 | USD 183.28 Million |

| Market Size by 2034 | USD 447.34 Million |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

The U.S. private label food and drink market refers to the segment of consumables sold under a retailer’s proprietary brand, rather than a national manufacturer. These products are manufactured by third-party contract manufacturers or vertically integrated in-house facilities and sold via retail channels, including supermarkets, hypermarkets, club stores, drugstores, and e-commerce. Driven by rising consumer trust, product innovation, and cost-conscious behavior, the private label market is steadily competing with national brands across all categories.

Some of the significant factors driving the U.S. private label food and drink market are increasing consumer desire for value and differentiation, increasing consumer trust in retailer brands, and a focus on health and wellness. In addition, by offering unique packaging, formulations, and Flavors, private label drinks allow retailers to differentiate themselves from competitors.

Consumers are trusting retailer brands rapidly and providing quality products at reasonable prices, which may accelerate the demand for private label and the drink market in the U.S. The increasing consumer shift towards perception also drives the market growth. Furthermore, to cater to specific dietary preferences or needs, the demand for healthy drink options is increasing rapidly. Retailers can create private-label sugar-free and organic fortified drinks with minerals and vitamins are further expected to drive the growth of the U.S. private label and drink market.

The private label and drinks segment is expected for continuous innovation with increasing competition, as retailers strive to exceed and address expectations for ethically sourced, sustainable, and healthier products, which may create significant opportunities in the U.S. The various company leaders are contributing significantly to private brands and signaling a commitment to value and quality.

In addition, the rising integration of AI-generated product development also enhances market growth in the U.S. To improve supply chain, forecast trends, and design Flavors for private label drinks, companies are integrating data analytics and AI, which is further expected to revolutionize the growth of the U.S. private label food and drink market in the coming years.

The increasing difficulties in the supply chain may create major challenges in the manufacturing of private labels and drinks. To keep up a dependable and steady supply chain for private label ingredients, it can be challenging for consumers, particularly those who are entering new markets. The challenges may increase from matters such as quality control, logistics, and sourcing, which may further restrain market growth. In addition, limited product differentiation, economic downfalls, quality control, and restricted advertising and marketing budgets are further expected to hinder the growth of the U.S. private label and drink market.

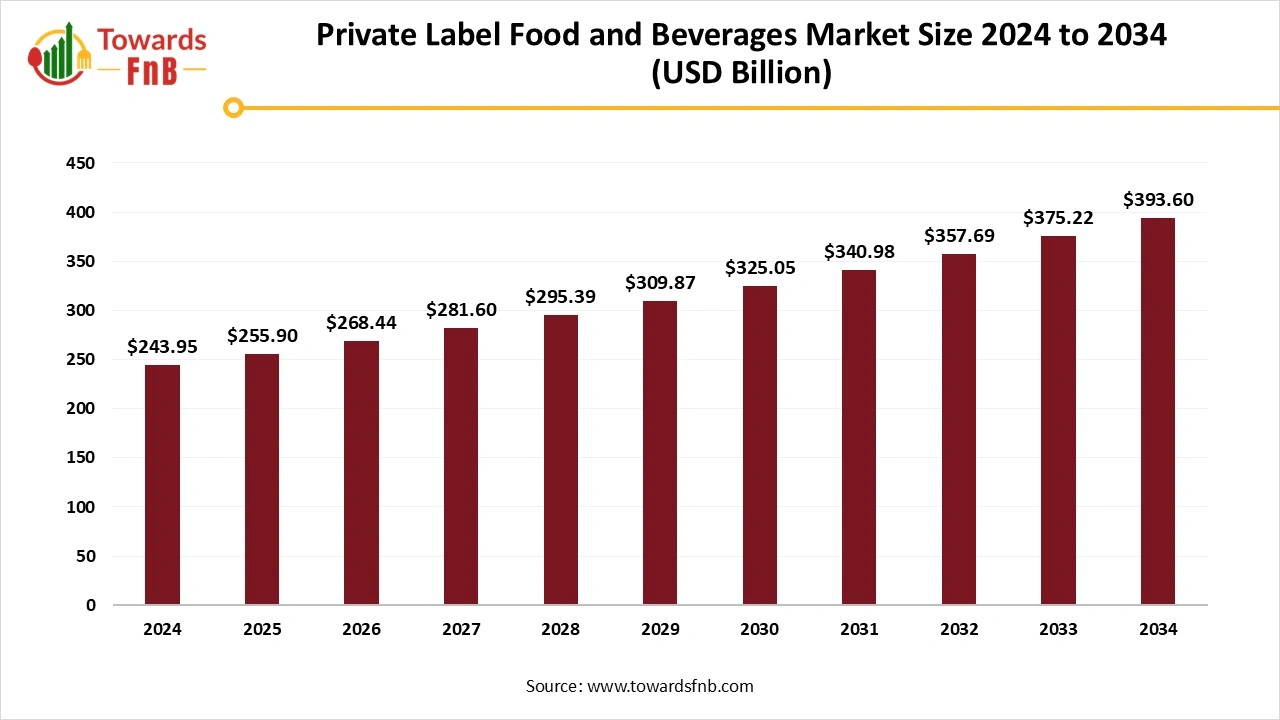

The global private label food and beverages market was valued at USD 243.95 billion in 2024 and is projected to grow from USD 255.90 billion in 2025 to approximately USD 393.60 billion by 2034, reflecting a CAGR of 4.9% during 2025 to 2034. This growth is driven by supportive government initiatives for private sector development, rising consumer preference for high-quality yet affordable products, and the ongoing evolution of private label manufacturers who are increasingly competing with national brands.

The market growth in the U.S. is attributed to the increasing consumer awareness towards health and wellness, increasing growth in e-commerce platforms, increasing use of the internet and smartphones, and increasing demand for high-quality products.

The online retailer Amazon provides private-label drinks under various house brands, including Amazon Fresh and Happy Belly. The consumer demand for affordable store brands is increasing as inflation has soared in the U.S. The private label and drinks sales in the U.S. grew by over 45 billion in 2023. Approximately 70% of adults are expected to purchase private label products in the coming year, according to the research from Mintel, which is further expected to drive the growth of the private label and drink market in the U.S.

How Food Segment Dominates U.S. Private Label Food and Drink Market Revenue in 2024?

The food segment dominated the U.S. private label food and drink market in 2024. The segment growth in the U.S. market is attributed to factors such as increasing flexibility in food consumption, increasing brand loyalty, cost-effectiveness, and increasing consumer demand for natural, organic, and unique food products. In the U.S., private label foods account for 18%. Consumers are continuously looking for diverse and unique food products that enhance their food preferences and tastes. By offering high-quality products, private labelling helps companies to build their brand quality, which enhances the consumer experience. The private labelling enables businesses to enhance products’ packaging and branding, which is further expected to enhance the segment growth in the U.S.

The Beverages Segment is Expected to Grow Fastest During the Forecast Period.

The segment growth in the U.S. private label food and drink market is attributed to factors such as increasing consumer focus on health and wellness, enhanced brand loyalty, responsiveness and flexibility, and higher profit margin. Retailers can improve brand loyalty among their consumers by offering high-quality beverages. To create custom packaging, flavours, and formulations, retailers can potentially work with the beverage industry. In addition, focusing on market trends and changing consumer preferences, retailers have greater flexibility with private-label beverages. Furthermore, private label beverages offer significant opportunities for targeted promotional and marketing campaigns, which further drive segment growth.

Why Supermarkets and Hypermarkets Segment Held the Largest U.S. Private Label Food and Drink Market Revenue in 2024?

The supermarkets and hypermarkets segment dominated the U.S. private label food and drink market in 2024. The segment growth in the market is driven by factors such as increasing consumer preference towards offline stores, improved operational efficiency, greater understanding of buyer behavior, increasing product discoverability, and increasing consumer desire to shop physically without waiting for delivery. In addition, the major advantages of supermarkets driving market growth are accessibility, promotional schemes, variety, and availability.

In June 2025, the 24-layer Chocolate Cake, ‘Matilda’, was Launched by Supermarkets, Which is Inspired by Bruce Bogtrotter.

The e-commerce & DTC segment is expected to grow fastest during the forecast period. The segment growth in the U.S. private label food and drink market is driven by the increasing consumer awareness towards health and wellness, increasing busy and modern lifestyles, increasing rapid growth in e-commerce platforms, and increasing the need for smartphones and internet penetration. In addition, the Direct-to-Consumer (DTC) model revolutionizes how products are consumed and procured in the beverage industry. Furthermore, enhanced profit margins, rich consumer insights, and empowered brand control are the potential benefits of DTC, which is further expected to drive segment growth.

What Factors Help Budget-Conscious Consumers Segment Grow in 2024?

The budget-conscious consumers segment dominated the U.S. private label food and drink market revenue in 2024. The segment growth in the market in the U.S. is attributed to the growing rapid nuclear families and urbanization, increasing demand for everyday and basic beverages, increasing penetration of retail channels, increasing consumer trust in private labels, and increasing product prices in food and beverages.

The Health-Conscious Shoppers Segment is Expected to Grow Fastest During the Forecast Period.

The segment growth in the U.S. private label food and drink market is attributed to the increasing consumer demand towards health and nutrition, increasing range of diverse consumer needs, increasing consumer preference towards plant-based options and functional beverages, rising innovation in technology integration and smart packaging, and demand for ready-to-drink beverages.

How Value/ Basic Tier Segment Dominates U.S. private label food and drink market Revenue in 2024?

The value/basic tier segment dominated the U.S. private label food and drink market in 2024. The segment growth in the U.S. market is propelled by the increasing consumers’ food purchasing behavior, rapid urbanization, increasing consumer preference towards consistent taste and quality improvements, increasing demand for necessary drinks, and rising cost of inflation and living.

The Premium Tier Segment is Expected to Grow Fastest During the Forecast Period.

The segment growth in the U.S. private label food and drink market is attributed to the increasing modern and busy lifestyles, rising innovation in ingredients, increasing consumer preference towards clean label packaging and sustainability, and increasing demand for functional drinks and wellness. In addition, the premium tier plays an important role in attracting quality-conscious consumers, driving segment growth, and elevating perception, which is further expected to enhance the segment growth in the U.S.

Generous Brands

bp

By Product Type

B. Beverages

By Distribution Channel

By Consumer Orientation

By Label Tier / Price Point

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

U.S. Private Label Food and Beverages Market