April 2026

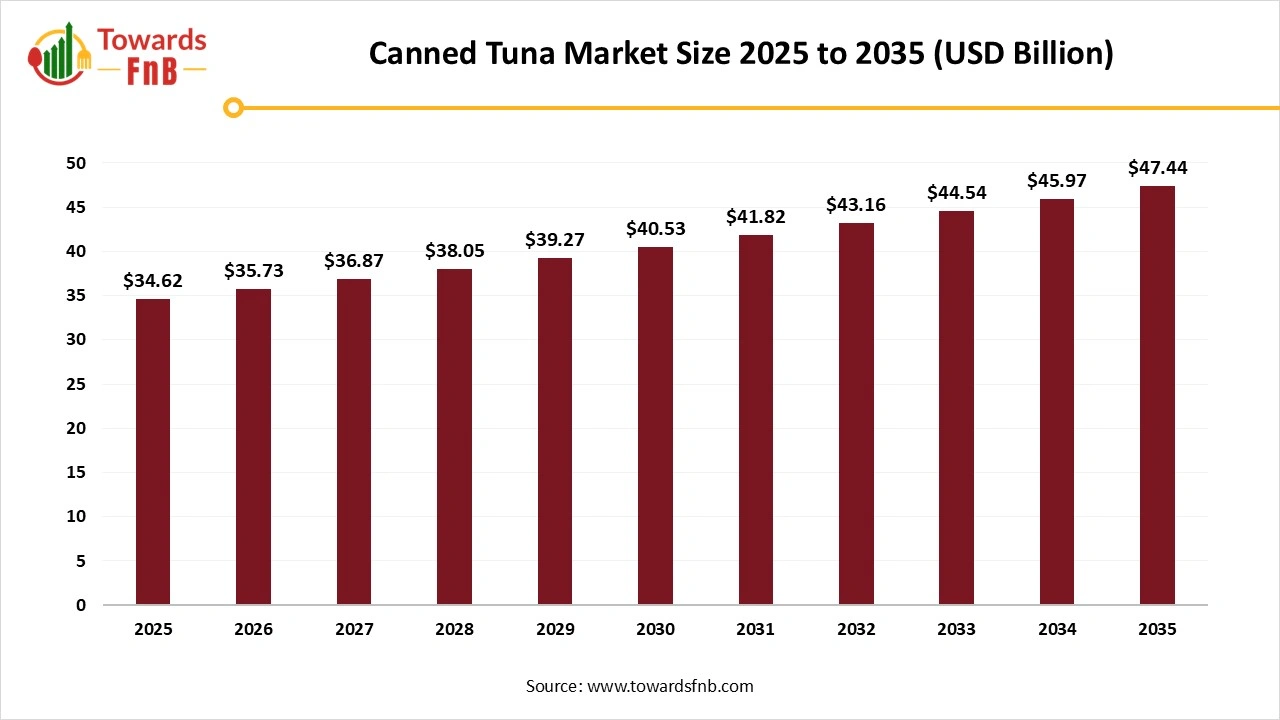

The global canned tuna market size reached at USD 34.62 billion in 2025 and is anticipated to increase from USD 35.73 billion in 2026 to an estimated USD 47.44 billion by 2035, witnessing a CAGR of 3.2% during the forecast period from 2026 to 2035. The market growth is fueled by increased consumer awareness of its health benefits, such as high protein and omega-3 content, along with its convenience and versatility as a food option.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 3.2% |

| Market Size in 2026 | USD 35.73 Billion |

| Market Size in 2027 | USD 36.87 Billion |

| Market Size by 2035 | USD 47.44 Billion |

| Largest Market | Europe |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The canned tuna market involves the production, distribution, and consumption of tuna preserved in cans or pouches for retail and food service. This segment includes various tuna species (such as skipjack and yellowfin), packaging types (metal cans and pouches), and sales channels (supermarkets, specialty stores, online). Canned tuna is valued for its high protein content, long shelf life, convenience, and nutritional benefits (like omega-3s and vitamins). Market trends are influenced by consumer preferences for ready-to-eat foods, concerns about sustainability, and limitations in the global seafood supply.

The canned tuna sector is advancing through technological innovations like vacuum sealing, advanced sterilization, and AI-driven inspection, which enhance product quality, shelf life, and efficiency. These advancements, along with automation in manufacturing processes, not only reduce production costs but also improve packaging, distribution, and overall market reach, enabling businesses to offer a broader range of ready-to-eat canned products while adhering to sustainability and food safety regulations.

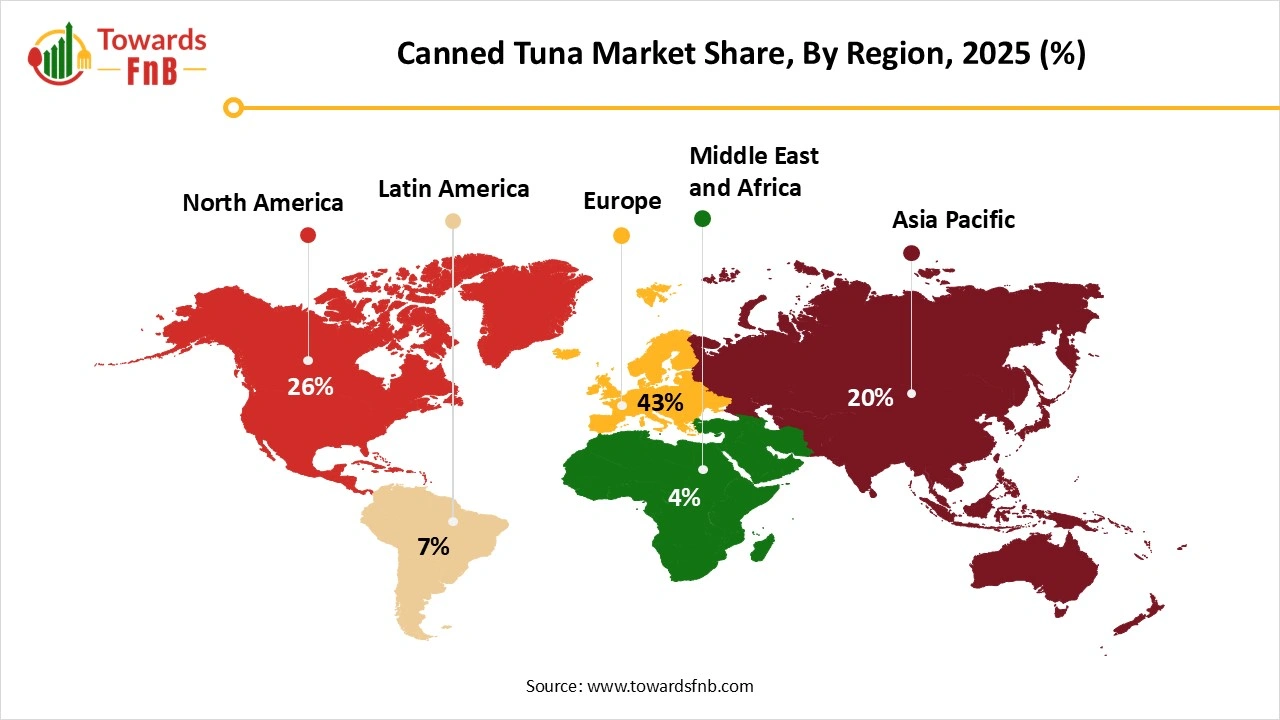

Why did Europe Dominate the Canned Tuna Market?

Europe dominated the canned tuna market by holding the largest share in 2024. This is mainly due to the increased consumer demand for more convenient and healthier ready-to-eat meals. The market is further fueled by an increasing preference for nutritious seafood, especially high-protein fish, as well as rising awareness about sustainable fishing practices, prompting greater investment in high-quality raw ingredients and the expansion of retail networks to meet the needs of busy, health-conscious consumers. Moreover, the growing demand for ready-to-eat seafood products that suit the busy lifestyle of urban residents is driving more investment in premium raw ingredients.

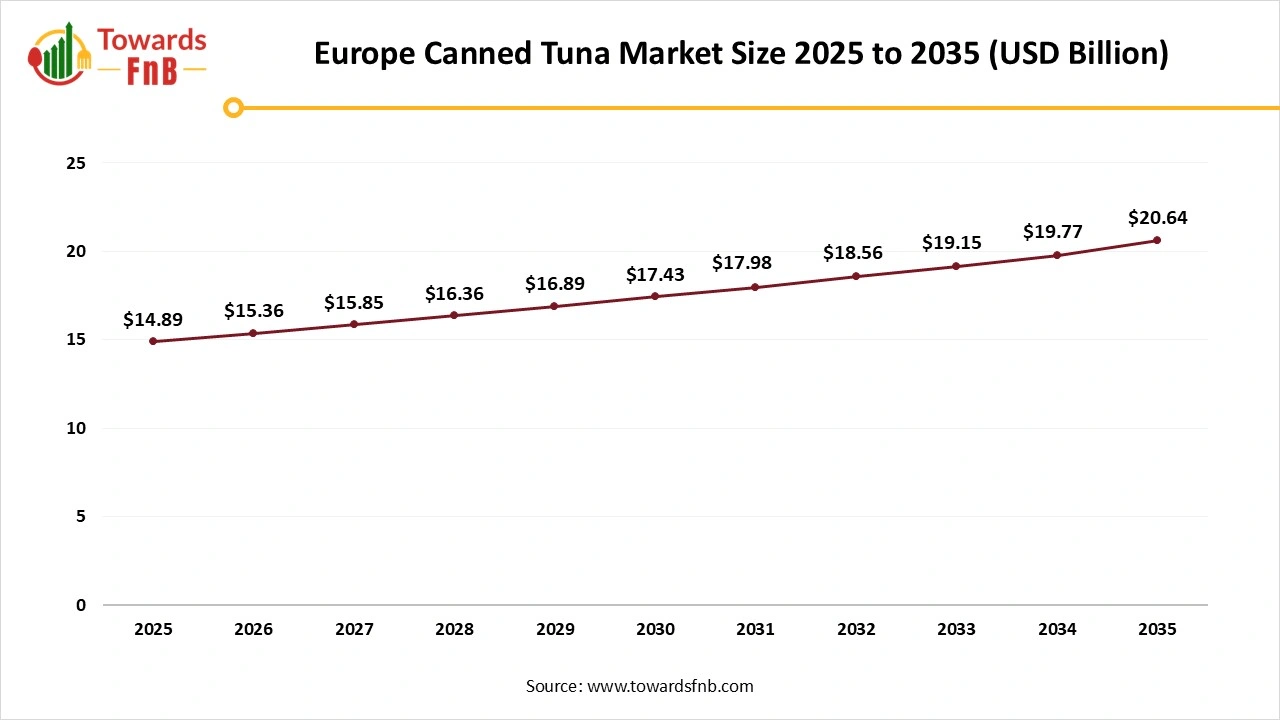

Europe Canned Tuna Market Size 2025 to 2035

The Europe canned tuna market size was calculated at USD 14.89 billion in 2025 with projections indicating a rise from USD 15.36 billion in 2026 to approximately USD 20.64 billion by 2035, expanding at a CAGR of 3.32% throughout the forecast period from 2026 to 2035.

Germany Canned Tuna Market Analysis

In Germany, the market is experiencing several key trends, including a growing preference for sustainable, responsibly sourced products, driven by rising consumer awareness of environmental issues and overfishing. There is also a rising demand for healthier, high-protein, and convenient ready-to-eat food options, as busy lifestyles make quick meals more appealing. Additionally, innovations in packaging, such as easy-open cans and environmentally friendly materials, are gaining traction, as consumers prioritize both convenience and sustainability in their purchasing decisions.

Middle East and Africa: The Fastest-Growing Region

The Middle East and Africa (MEA) is expected to grow at the fastest rate during the forecast period. This growth is driven by the increasing demand for convenient, long-lasting, and nutritious food options, particularly in urban areas with busy lifestyles and limited refrigeration. Canned tuna's affordability, extended shelf life, and versatility make it a staple in many households, while rising health consciousness boosts the demand for its lean protein and omega-3 fatty acids. Additionally, product innovations, including convenient packaging and a wider variety of flavors, cater to diverse consumer preferences and further fuel market expansion in the region.

")

UAE Canned Tuna Market Analysis

The canned tuna market in the UAE is experiencing strong growth, driven by its convenience, health benefits (rich in protein and omega-3s), and affordability compared to fresh fish. As a key part of the broader canned seafood industry, the market benefits from the UAE's diverse population and growing health awareness. In 2023-2024, the UAE imported 92 shipments of tuna from 22 international suppliers to 21 buyers, reflecting a 5% increase in imports from the previous year, signaling sustained market expansion.

What Factors are Driving the Growth of the Canned Tuna in North America?

The market in North America is driven by increasing consumer awareness of health-conscious diets, driving higher consumption of tuna, which is rich in protein and omega-3s. Additionally, the rising demand for ready-to-eat and convenient seafood options aligns with consumers' busy lifestyles, making canned tuna an ideal choice for portable and nutritious meals, further boosting market growth.

The U.S. is a major contributor to the market due to its high demand for convenient, ready-to-eat meals and increasing consumer focus on health and wellness. Tuna, with its high protein content and omega-3 benefits, aligns with growing trends for healthier food options. Additionally, the U.S. market is bolstered by its strong retail infrastructure, e-commerce growth, and consumer interest in sustainable, ethically sourced seafood, further driving demand for canned tuna products.

What Makes Asia Pacific a Notably Growing Area?

Asia Pacific is expected to experience notable growth in the upcoming period, fueled by rising seafood demand and increasing disposable incomes. Shifting dietary preferences, a growing need for convenient protein sources, and the fast-paced urban lifestyle are driving consumers toward ready-to-eat canned options. The region's strong tuna fishing and processing industries, particularly in countries like Thailand, Indonesia, and the Philippines, also support market growth by ensuring a steady supply of canned tuna.

China Canned Tuna Market Analysis

The market in China is driven by evolving consumer tastes and a growing awareness of the health benefits associated with seafood. Culinary trends in China are shifting, with an increasing interest in global cuisines that incorporate canned tuna, leading to its use in diverse dishes like salads and pasta. As consumers become more adventurous with their food choices, the versatility of canned tuna is gaining popularity, further fueling market growth.

What Potentiates the Growth of the Canned Tuna Market in Latin America?

The market in Latin America is witnessing steady growth, driven by a growing demand for convenient, protein-rich, and nutritious food options. Urbanization, coupled with changing lifestyles and an increased focus on health, is leading to a shift toward ready-to-eat and shelf-stable products, especially in countries like Brazil, Colombia, and Chile. As consumers adopt busier routines, canned tuna offers a practical solution that fits their need for quick and healthy meals.

Brazil Canned Tuna Market Analysis

Brazil leads the market in Latin America due to its strong cultural affinity for seafood, with canned tuna being a staple in many traditional and contemporary Brazilian dishes. The country's growing urbanization, hectic lifestyles, and increasing focus on convenience, health, and protein-rich diets further fuel the demand for canned tuna as a quick, affordable, and nutritious food option. Additionally, Brazil’s large retail and foodservice sectors provide widespread accessibility to canned tuna, reinforcing its dominant market position in the region.

Canned Tuna Market Share, By Species/Product Type, 2025 (%)

| Segments | Shares (%) |

| Skipjack | 70% |

| Yellowfin | 30% |

Why did the Skipjack Segment Dominate the Canned Tuna Market?

The skipjack segment dominated the market in 2025 because of its widespread availability, affordability, and appropriateness for light tuna items, which are favored by buyers. Its lower mercury content compared to other tuna varieties makes it a healthier and more sustainable choice for frequent consumption, enhancing its appeal, particularly among health-conscious shoppers. The need for easy, ready-to-eat meals has increased, and canned skipjack tuna aligns seamlessly with this trend.

The Yellowfin Segment is Expected to Grow at the Fastest Rate During the Forecast Period

Driven by its superior quality, prized for its firm texture and rich flavor, making it perfect for gourmet and upscale products. This demand is backed by rising health awareness, an emphasis on protein-rich foods, and a shift towards convenience and sustainably sourced seafood.

The others segment, which include Albacore and Bigeye, is expected to grow significantly during the forecast period because of distinct qualities that attract various consumer segments, ranging from everyday affordability to premium tastes. Both species are considered more valuable than skipjack tuna, attracting a market that seeks more than just the typical canned offering.

Canned Tuna Market Share, By Product Style/Type, 2025 (%)

| Segments | Shares (%) |

| Light Tuna | 60% |

| White / Albacore Tuna | 20% |

| Unflavored | 12% |

| Flavored | 8% |

How did the Light Tuna Segment Dominate the Canned Tuna Market?

The light tuna segment held the dominant market share in 2024 due to several factors such as affordability, high protein content, lower mercury levels, and versatility in various recipes. Light tuna appeals to consumers as a low-fat, nutritious protein option that is also budget-friendly and adaptable for a wide range of dishes, from simple sandwiches to elaborate casseroles.

The White/Albacore Tuna Segment is Expected to Grow at the Fastest CAGR During the Forecast Period

Albacore white tuna has a milder flavor and lighter color, often regarded as higher quality and closer to fresh fish. Consumers who prioritize health and have higher disposable incomes tend to choose white tuna, seeing it as a more premium option.

Canned Tuna Market Share, By Packaging Format, 2025 (%)

| Segments | Shares (%) |

| Metal Cans | 80% |

| Pouches / Tetra / Flexible Packaging | 20% |

Which Packaging Format Held the Largest Share of the Canned Tuna Market?

The metal cans segment dominated the market with the largest share in 2025. Metal cans offer a complete barrier against oxygen, moisture, and light, which are key factors in food spoilage. Their strength allows them to withstand high temperatures during the sterilization process. For many years, canned tuna in metal containers has become a staple in homes worldwide, thanks to its reliability and convenience.

The Pouches/Tetra/Flexible Packaging Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Primarily driven by rising consumer preferences for convenience, portability, and sustainability, as well as logistical and production benefits for producers. The adaptable material provides a 360-degree surface for high-quality graphics and branding, enhancing shelf visibility and product differentiation compared to conventional cans.

What Made Hypermarkets & Supermarkets the Dominant Distribution Channel in the Canned Tuna Market?

The hypermarkets & supermarkets segment dominated the market while holding the largest share in 2025. This is mainly due to their convenience, extensive product range, and competitive pricing. These retail formats provide a convenient shopping experience, enabling consumers to effortlessly buy canned tuna with their other groceries. They also offer a wide range of brands and varieties, often at reduced prices due to bulk-purchasing advantages and special deals.

The Online/E-commerce Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Online platforms enable consumers to purchase items from home and receive deliveries at their doorstep, making it perfect for staple products such as canned tuna. Digital platforms offer a wide variety of products, including specialty and sustainably sourced options, enabling consumers to effortlessly compare brands and prices. Digital platforms enable brands to market directly to consumers, enhancing profit margins and fostering stronger customer connections.

Dongwon F&B

Bumble Bee Seafoods

By Species/Product Type

By Product Style/Type

By Packaging Format

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Canned Tuna Market