April 2026

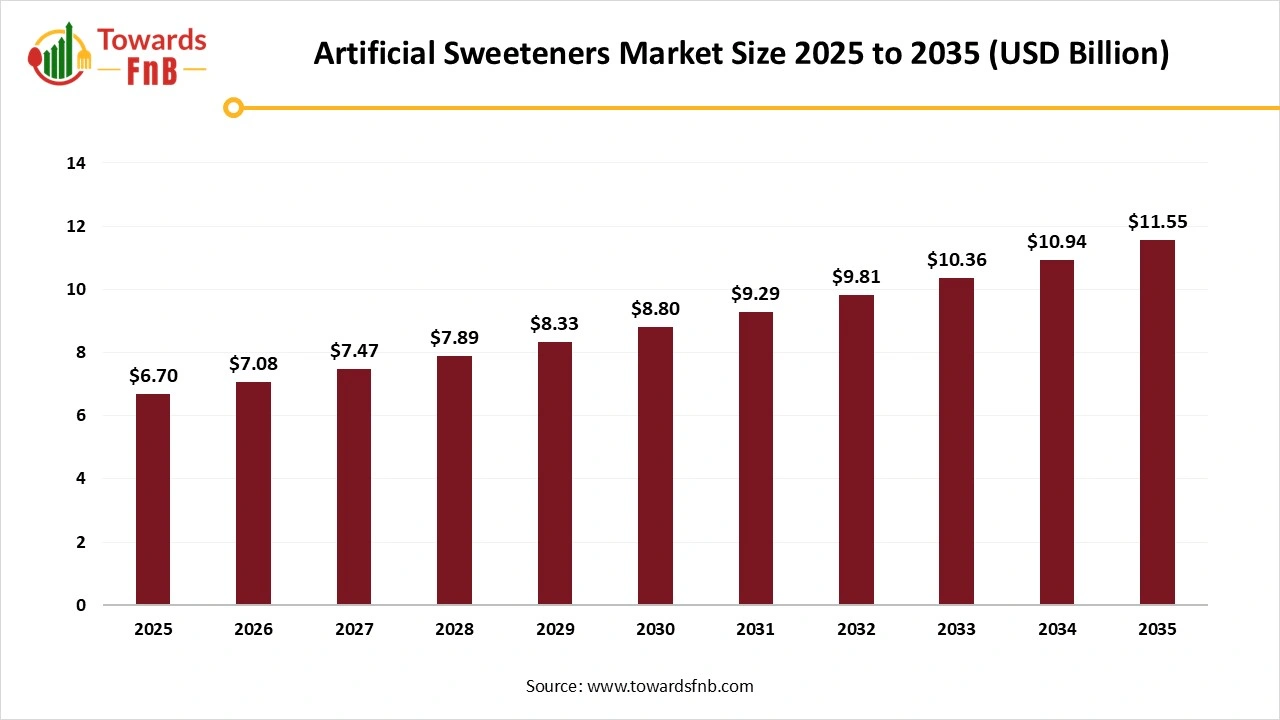

The global artificial sweeteners market size estimated at USD 6.70 billion in 2025 and is predicted to increase from USD 7.08 billion in 2026 to reach nearly USD 11.55 billion by 2035, with a CAGR of 5.6% during the forecast period from 2026 to 2035.This growth is due to the low-calorie and diabetic friendly food options.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.6% |

| Market Size in 2026 | USD 7.08 Billion |

| Market Size in 2027 | USD 7.47 Billion |

| Market Size by 2035 | USD 11.55 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The artificial sweeteners market includes the production and distribution of high-intensity synthetic sugar substitutes, such as aspartame, sucralose, and saccharin, used to provide sweetness with minimal or zero calories. These additives are essential in formulating diet and sugar-free products for weight management, diabetic care, and calorie-conscious global consumer diets.

Advances in technology and the increasing popularity of innovative foods have led various brands to develop next-generation sweetener solutions. Additionally, integrating artificial intelligence and machine learning into food science could accelerate the discovery of new sweet compounds. Manufacturers are continuously conducting R&D activities to improve the taste profile and sweetness intensity of synthetic sweeteners. The emergence of novel sweeteners like stevia and tagatose, which mimic the taste of sugar, is aiding in the adoption of these alternatives. Companies are also employing techniques such as masking agents and synergistic sweetener blends to overcome any bitter aftertastes.

Raw Material Procurement

Processing

Quality control

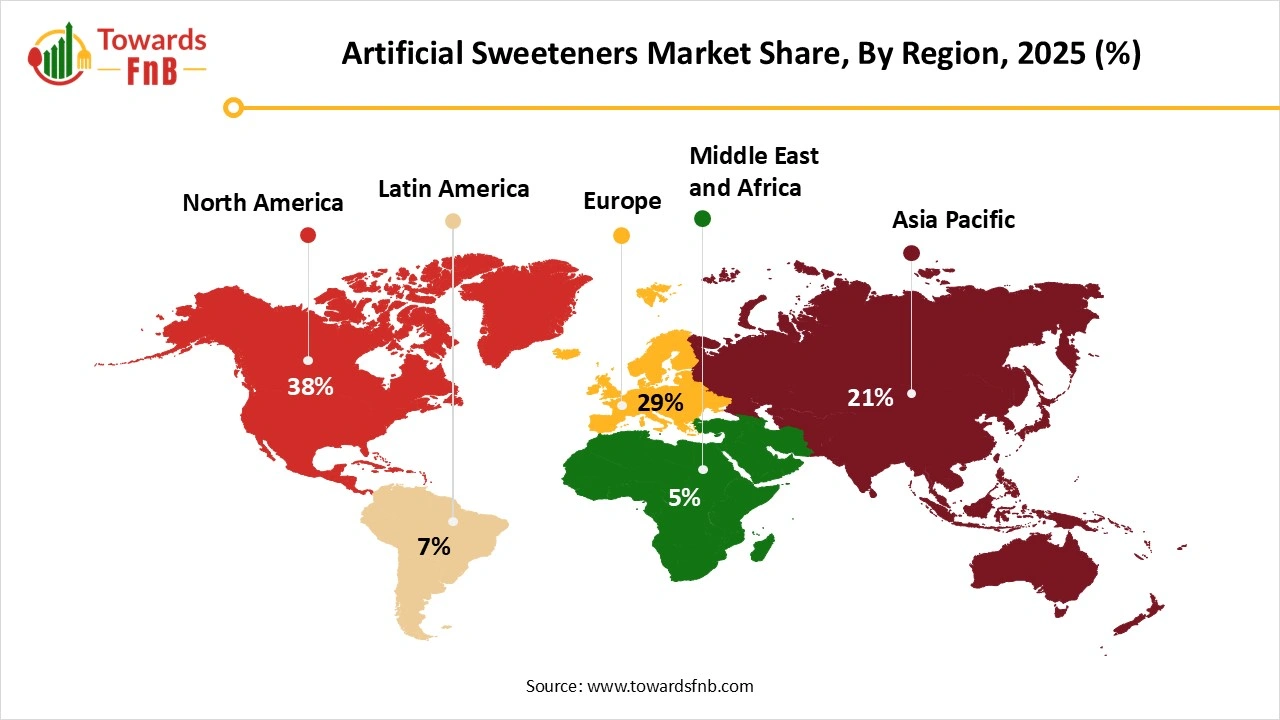

Which Region Dominated the Artificial Sweeteners Market in 2025?

North America dominated the artificial sweeteners market with approximately 38.1% share in 2025. The growth of the North American market is primarily driven by increasing health consciousness among consumers, leading to a shift toward low-calorie and sugar-free products. The rising prevalence of obesity, diabetes, and other lifestyle-related health issues further propels the demand for artificial sweeteners as healthier alternatives to sugar. Producers are launching new low-calorie options as consumers search for healthier choices across various product categories. Furthermore, The American Heart Association labels zero- and reduced-energy food additives as low-calorie sweeteners (LCS). The Food and Drug Administration has approved several LCS as safe for use in food and beverages, including Acesulfame-K, Advantame, Aspartame, Neotame, Saccharin, and Sucralose. The FDA also considers stevia, monk fruit, and allulose to be Generally Recognized as Safe for use as LCS.

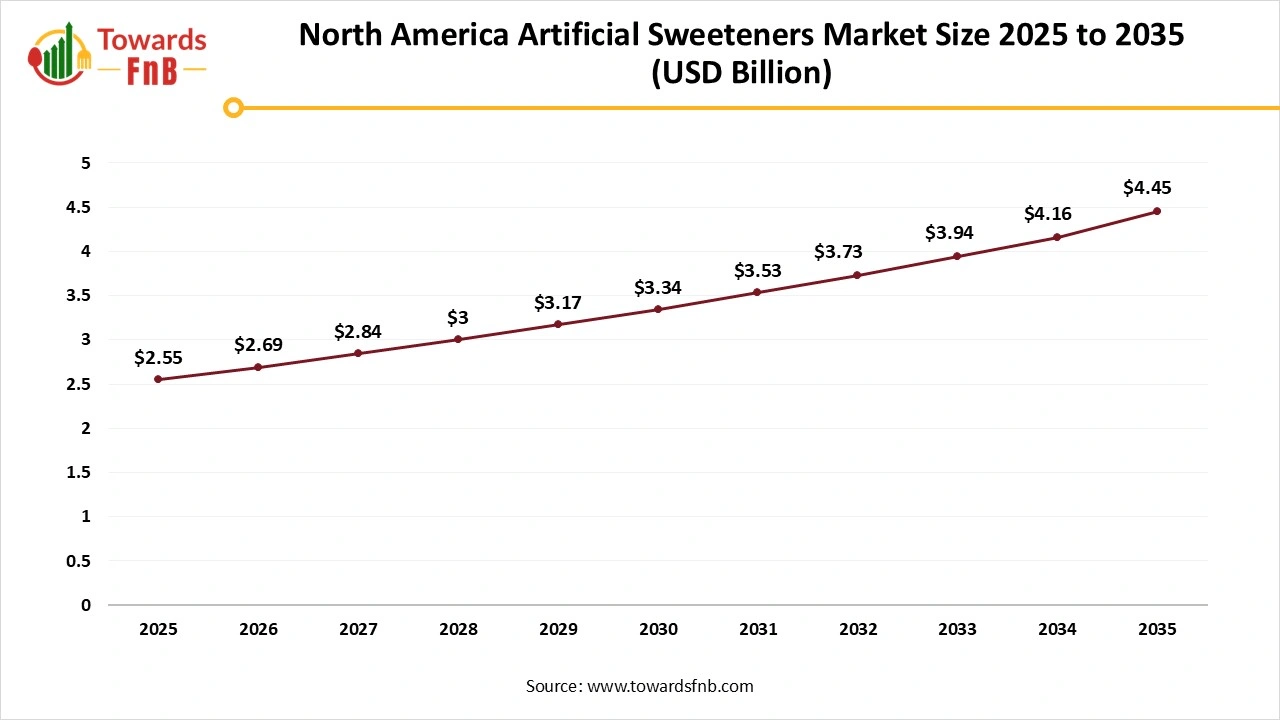

North America Artificial Sweeteners Market Size 2025 to 2035

The North America artificial sweeteners market size was calculated at USD 2.55 billion in 2025 with projections indicating a rise from USD 2.69 billion in 2026 to approximately USD 4.45 billion by 2035, expanding at a CAGR of 5.73% throughout the forecast period from 2026 to 2035.

U.S. Artificial Sweeteners Market Trends

As people prioritize healthier lifestyles and seek sugar substitutes that aid in weight control and illness prevention, the artificial sweeteners market in the U.S. is expanding significantly. Artificial sweeteners provide sweetness without the calories associated with regular sugar and are widely used in various industries, including food, beverages, pharmaceuticals, and personal care. To adapt to changing consumer preferences, businesses are also investing in healthier and clean-label artificial sweetener options.

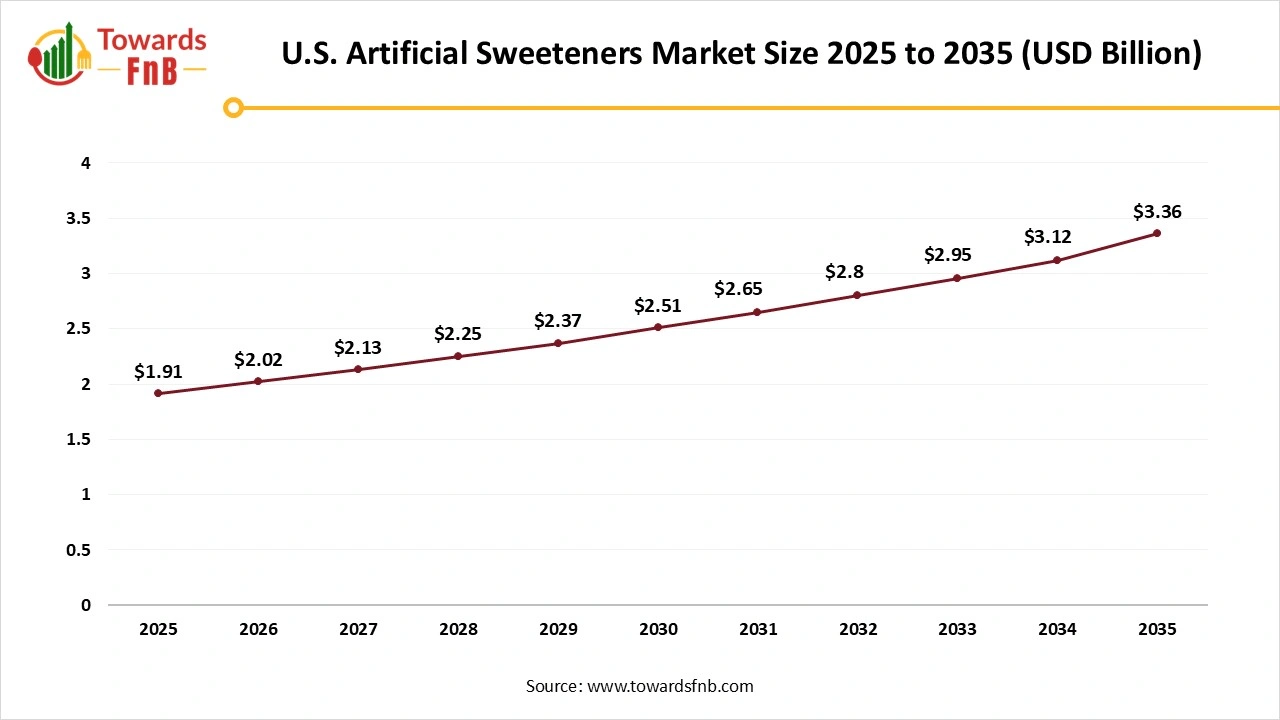

How Big is the U.S. Artificial Sweeteners Market?

The U.S. artificial sweeteners market size estimated at USD 1.91 billion in 2025 and is predicted to increase from USD 2.02 billion in 2026 to nearly reaching USD 3.36 billion by 2035, growing at a CAGR of 5.81% during the forecast period from 2026 to 2035.

Asia Pacific Artificial Sweeteners Market Trends

Asia Pacific expects fastest growth during the forecast period. The rapid growth of artificial sweeteners in the Asia Pacific region can be attributed to evolving consumer preferences, increased health awareness, and significant lifestyle changes. As the region becomes more urbanized, there is a marked shift toward healthier living, driven largely by rising concerns over obesity, diabetes, and other lifestyle-related diseases. This shift in consumer behavior has significantly influenced the demand for healthier alternatives to traditional sugar, leading to a growing preference for low or no-calorie sweeteners, including artificial ones.

India Artificial Sweeteners Market Trends

Artificial sweeteners have gained popularity in India in the food and beverage sector due to rising concerns about obesity and diabetes. Urban areas in India are adopting artificial sweeteners significantly, influenced by the convenience of processed food consumption. With the changed regulatory landscape allowing the use of sweeteners in everyday consumables, the market is poised for growth. The entry of new and safer molecules could lead to large volumes in the artificial sweeteners industry in India.

")

Europe Artificial Sweeteners Market Trends

The increased consumer awareness and demand for low-calorie products are driving the market for artificial sweeteners in Europe. Currently, the European Union has approved 17 artificial sweeteners and their combinations for use in food products. While high-intensity sweeteners such as aspartame, sucralose, and acesulfame K remain popular, there is a rapidly growing demand for natural alternatives like stevia, erythritol, and xylitol due to cleaner label trends. Western and Northern European countries, including Germany, France, and the UK, generally exhibit a higher demand for artificial sweeteners, which are commonly found in sugar-free beverage, dairy products, and confectioneries.

Germany Artificial Sweeteners Market Trends

Germany is the largest market for artificial sweeteners in Europe. The rise in the consumption of processed food products, along with the cost-effectiveness and high sweetness potency of these sweeteners, makes them the preferred choice in the food, beverage, and pharmaceutical industries. Additionally, supportive government policies that promote reduced sugar intake and the expanding application of sweeteners across various sectors further accelerate market growth in Germany.

Artificial Sweeteners Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Sucralose | 34% |

| Aspartame | 25% |

| Saccharin | 15% |

| Acesulfame Potassium (Ace-K) | 10% |

| Neotame | 16% |

Why did the Sucralose Segment Dominate the Artificial Sweeteners Market in 2025?

The sucralose segment dominated the artificial sweeteners market with approximately 34% share in 2025. Due to its stability, food manufacturers can use sucralose to create a variety of great-tasting new foods and beverages, including canned fruit, low-calorie fruit drinks, baked goods, and sauces and syrups. Sucralose can also be used as a sweetener in nutritional supplements, medical foods, and vitamin/mineral supplements. It combines the taste of sugar with the necessary heat, liquid, and storage stability for use in all types of foods and beverages.

The Neotame Segment is Expected to Grow at the Fastest Rate During the Forecast Period

Its higher heat stability, fewer usage restrictions, and greater sweetness potency provide a 30% cost advantage due to lower dosage requirements. Neotame has advantages over aspartame, such as stability at neutral pH, making it suitable for baked goods. Its rapid onset of sweetness and lingering duration make it ideal for use in chewing gum and candies. In carbonated drinks, neotame enhances citrus or berry notes without overshadowing delicate flavors.

Artificial Sweeteners Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Powder/Granular | 71% |

| Liquid/Syrup | 15% |

| Tablets | 14% |

Which Form Segment Dominated the Artificial Sweeteners Market in 2025?

The powdered/granular segment dominated the market with approximately 71% share in 2025, owing to its superior stability, long shelf life, and ease of use across a variety of food and beverage applications. Additionally, powdered sweeteners have a significantly longer shelf life than liquid counterparts, as they are less prone to degradation caused by moisture, heat, or microbial contamination. The powdered format also ensures uniform mixing, making it ideal for large-scale food manufacturing processes where consistency is crucial.

The Liquid/Syrup Segment is Expected to Grow Notably During the Predicted Timeframe

Liquid syrups dissolve more easily in hot drinks, resulting in uniformly sweetened beverages. Using liquid sugars instead of granulated sugars contributes to moist and fluffy baked goods. Moreover, the production of liquid sweeteners typically requires minimal processing, a key factor driving their demand in end-use industries. These sweeteners are often used to enhance volume and improve mouthfeel in items like ice cream, yogurts, and dressings.

Artificial Sweeteners Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Beverages | 39% |

| Bakery & Confectionery | 12% |

| Dairy Products | 15% |

| Pharmaceuticals & Nutraceuticals | 8% |

| Tabletop Sweeteners | 26% |

Which Application Segment Dominated the Artificial Sweeteners Market in 2025?

The beverages segment dominated the market with approximately 39% share in 2025, as these sweeteners can help in the formation of zero-calorie drinks, an appealing health advantage, often sought for weight loss or weight maintenance. Some sweeteners are up to 200 times sweeter than sugar or high fructose corn syrup (HFCS), meaning their higher cost is offset by the small quantities required. Functional beverages, diet sodas, and low-sugar snacks significantly contribute to market growth, especially with increasing investments in product reformulation. The rising trend of personalized beverages, which offer customizable sweetness levels and flavor enhancements, is shaping the future of beverage sweetener formulations globally.

The Bakery & Confectionery Segment is Projected to Experience the Fastest Growth During the Forecast Period

Food sweeteners play a crucial role in this industry, enhancing the taste, texture, and overall quality of various products. In baked goods, sucralose and acesulfame potassium are commonly employed due to their ability to withstand temperature variations. Maltitol is often used in chocolates and confectionery for its high sweetening power.

Ingredion

Mylor Bio Co., Ltd

By Product Type

By Form

By Application

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Artificial Sweeteners Market