April 2026

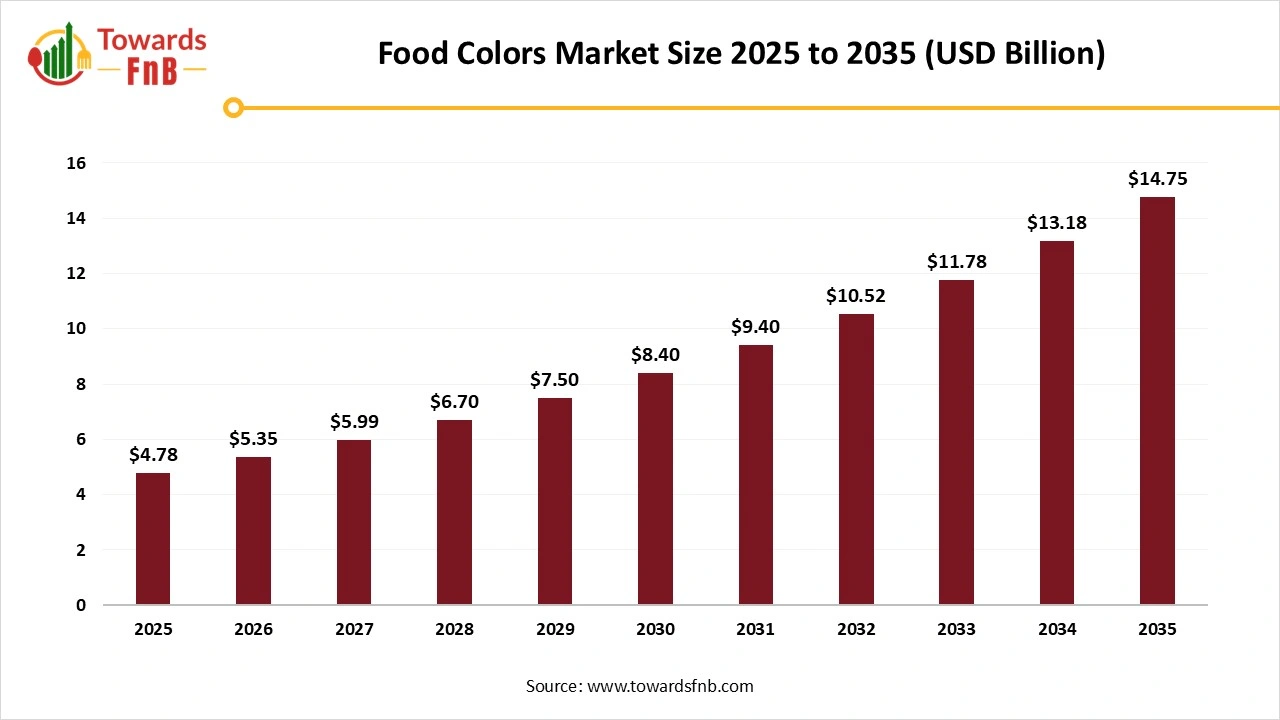

The global food colors market size reached at USD 4.78 billion in 2025 and is expected to grow steadily from USD 5.35 billion in 2026 to reach nearly USD 14.75 billion by 2035, with a CAGR of 11.93% during the forecast period from 2026 to 2035. The market is primarily driven by the need to enhance the visual appeal of food products and a significant shift in consumer preference towards natural, clean-label ingredients.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 11.93% |

| Market Size in 2026 | USD 5.35 Billion |

| Market Size in 2027 | USD 5.99 Billion |

| Market Size by 2035 | USD 14.75 Billion |

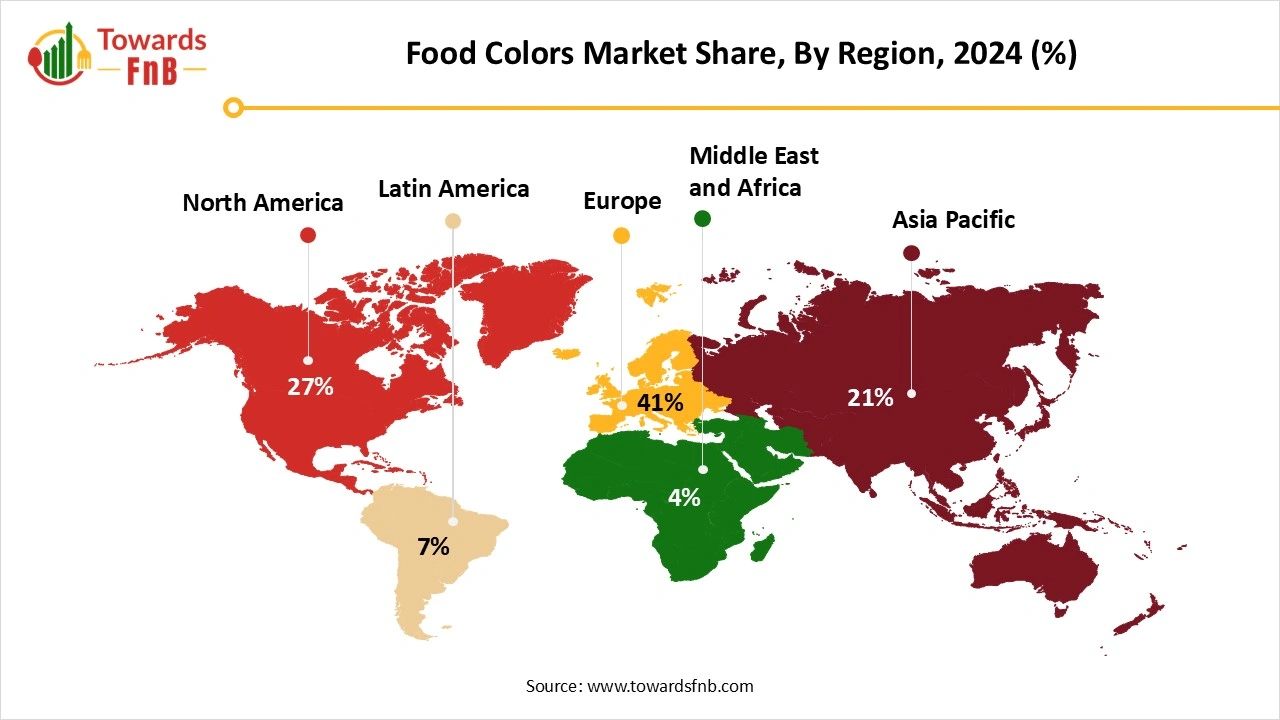

| Largest Market | Europe |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A particularly thrilling advancement is the combination of natural extracts with bioengineering methods. Microencapsulation represents a significant advancement. Recent advancements in food coloring technology feature intelligent colorants that can alter their hue in response to environmental factors such as temperature, pH, and humidity. Advancements in food coloring technology are improving the visual appeal of food while also meeting requirements for safety, sustainability, and natural ingredients. Firms such as Ginkgo Bioworks and Conagen use fermentation to produce colors from microbes. These advancements respond to the growing demand for natural, safe food choices and for novel ways to engage with food.

Raw Material Procurement

Food Color Processing

Packaging of Food Color

Logistics and Distribution

Europe Food Colors Market Analysis

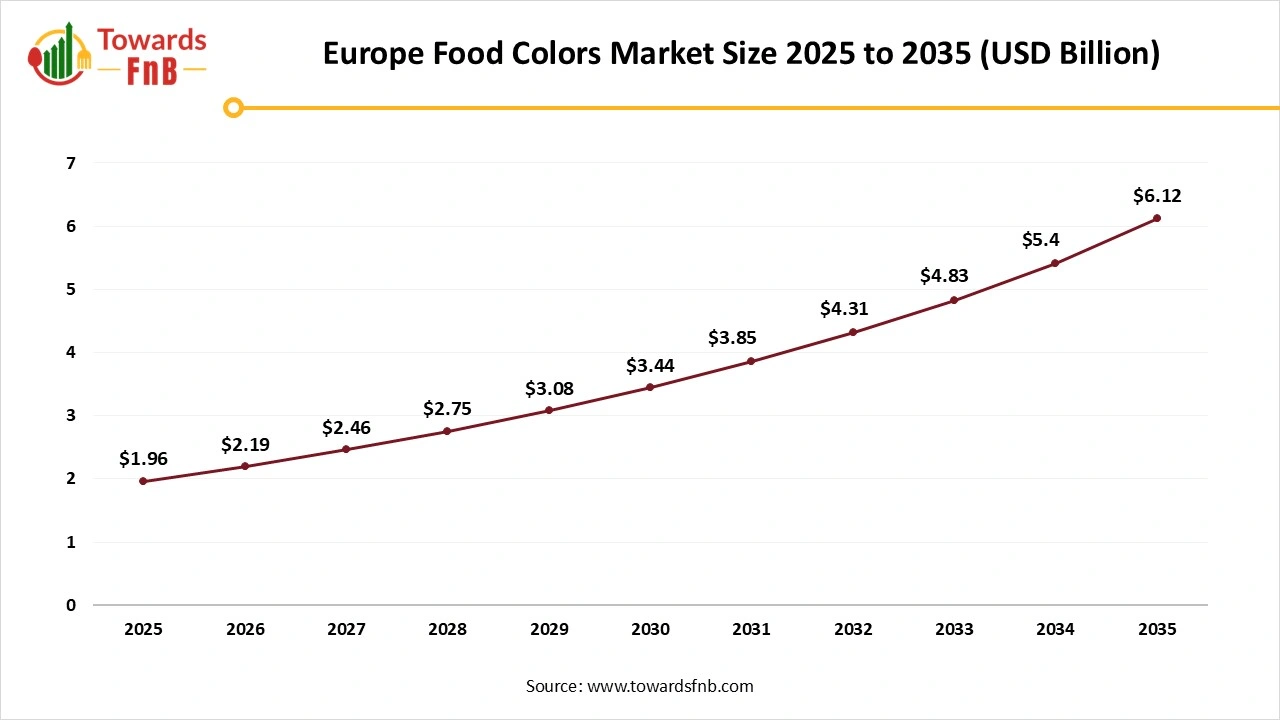

Europe dominated the food colors market in 2025. European consumers are increasingly opting for foods made with natural, healthier ingredients, exerting significant pressure on manufacturers to replace synthetic colors with plant-derived alternatives. This shift is supported by stringent EU food safety regulations that encourage companies to adopt safer, more transparent practices. European consumers are increasingly opting for foods with natural, healthier ingredients, putting significant pressure on manufacturers to replace synthetic colors with plant-derived alternatives.

Europe Food Colors Market Size 2025 to 2035

The Europe food colors market size was valued at USD 1.96 billion in 2025 and is expected to grow steadily from USD 2.19 billion in 2026 to reach nearly USD 6.12 billion by 2035, with a CAGR of 12.06% during the forecast period from 2026 to 2035.

This shift is bolstered by rigorous EU food safety rules that encourage businesses to adopt safer, more transparent practices. The rise in the use of natural colors across multiple food categories in Europe is boosting imports of different plant-derived substitutes. Imports to Europe of items classified under HS code 32030010, pertaining to vegetable-origin coloring agents, have steadily risen in recent years.

Germany Food Colors Market Insights

Germany stands as Europe's largest market for food colors, driven by millennials' increasing preference for dairy, seafood, bakery, and confectionery products, along with fresh and natural food colors. Germany continues to spearhead the European trend in organic and functional food, with natural food colorings facilitating product appearance innovation and enabling clean labeling. The advancement of market trends is propelled by technological innovations in extraction and enhanced stability of natural pigments in applications such as beverages, baking, dairy products, snacks, and confectionery.

")

Asia Pacific Food Colors Market Analysis

Asia Pacific is expected to see significant growth during the forecast period. The market is seeing considerable expansion driven by rising consumer interest in natural and organic food items, especially in the growing food processing sectors of China and India. The beverage and confectionery industries drive demand for colorants, while regulatory environments across Asia-Pacific shape market dynamics through differing standards and allowable limits for synthetic colors. Health issues, including research linking artificial colorants to hyperactivity in children, have led producers to move toward natural substitutes.

India Food Colors Market Insights

The market for food colors in India is driven by ready access to raw materials, including fruit and vegetables. In India, the yield of fruits and vegetables is substantial due to the extensive production regions. The evolving lifestyle and increased economic stability have led to heightened consumer demand for attractive food, driving the growth of the food colorants market in the nation. Indian food color manufacturers are establishing new benchmarks with natural resources, cutting-edge technology, and world-class production. Firms such as Hridhan Chem are also prominent as dyestuff producers in India.

North America Food Colors Market Analysis

The food colors market in North America is expected to expand considerably, driven by consumer preferences for natural and clean-label products and new regulations banning petroleum-derived synthetic dyes. This expansion is mainly due to the FDA's requirement to eliminate petroleum-derived synthetic dyes by December 2026, which is driving the transition of natural colorants from a specialized segment to widespread use. The market share for natural solutions is projected to grow as producers secure long-term supply agreements to support reformulation initiatives.

United States Food Colors Market

The United States distinguishes itself as a crucial regional market, driven by rising consumer demand for natural and clean-label products. Moreover, heightened health consciousness is driving greater demand for food and drinks containing natural colorants, including those derived from fruits, vegetables, and spices. The growing processed and packaged food sector is driving this expansion, as producers aim to boost product appeal with bright, secure colors.

Middle East and Africa Food Colors Market Analysis

The food colors market in the Middle East and Africa (MEA) is witnessing notable expansion, driven by a growing population, rising demand for processed and ready-to-eat meals, and an increasing inclination towards natural and healthy ingredients. Efforts and strategies to attract foreign investment in the food and beverage industry are expected to boost the market.

UAE Food Colors Market

The food processing industry in the UAE generates billions in revenue and is home to thousands of food and beverage firms, boosting the need for food colors. Advancements in color extraction and formulation technologies are enhancing the quality and range of food colors available. The UAE has established food labeling regulations (UAE S. 9: 2017) and is taking measures to prohibit specific artificial colors, including Red No. 3, found in numerous products worldwide. Halal certification is essential, necessitating colorants that comply with halal standards.

Latin America Food Colors Market Analysis

The demand for food colors in Latin America is increasing, mainly due to a strong inclination towards natural colors derived from fruits, vegetables, and plants, which corresponds with consumer interest in clean-label products, health and wellness, and plant-based diets. This trend is backed by regulatory limitations on synthetic dyes and advancements in extraction methods. As a result, demand for natural food colors, especially those derived from sources such as anthocyanins, turmeric, and spirulina is growing significantly in the food and beverage industry.

Brazil Food Colors Market

Brazil is notable for its robust agricultural industry, which ensures a consistent supply of raw materials such as annatto, turmeric, and various plant-based ingredients used to create natural colors. Mexico is not far behind, capitalizing on its extensive processed-food sector and growing exports to adjacent North American markets, thereby solidifying its leadership in the area. The Brazilian government, through ANVISA, has implemented tougher regulations on the use of synthetic additives in food products. Revised in 2023, these regulations have encouraged the use of natural food colors in packaged and processed foods

Food Colors Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Natural Colors | 76.5% |

| Synthetic Colors | 23.5% |

Why did the Natural Colors Dominate the Food Colors Market?

The natural colors segment led the food colors market by holding the share of 76.5% in 2025, driven by increasing consumer health awareness, a desire for clean-label items, and worries about the negative impacts of synthetic dyes. Technological advances, including microencapsulation and precision fermentation, have enhanced the stability and cost-effectiveness of natural colors, while tighter regulations on synthetic dyes further promote the transition to natural alternatives.

The Synthetic Colors Segment is Observed to Grow at the Fastest CAGR of 6.8% During the Forecast Period

Because of their affordability, vibrant color quality, excellent durability, and broad accessibility. These elements attracted food manufacturers to produce eye-catching, consistent, and shelf-stable items that resonate with consumers and uphold brand identity throughout worldwide supply chains. They provide enhanced stability across different processing and storage environments, helping preserve a uniform product appearance and color vibrancy over time.

Food Colors Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Liquid Form | 71.5% |

| Powder Form | 28.5% |

Which Form of Food Colors Held the Dominating Share of the Market?

The liquid form segment held the dominating share of 71.5% in the food colors market in 2025, due to its versatility, user-friendliness, and capacity to improve product quality. Liquid colors mix effortlessly with various products, providing consistent and stable hues, making them perfect for drinks, sauces, and dairy items, particularly in mass production. Moreover, the increasing desire for convenient and tailored food products enhances their appeal, as they provide ease of use and accurate color management for producers.

The Powder Form Segment is Seen to Grow at a Notable CAGR of 6.5% During the Predicted Timeframe

Due to its considerable benefits regarding storage, handling, and accurate application, resulting in extended shelf life, reduced spillage risk, and improved transportability. These advantages are essential for food producers, particularly for large-scale operations, allowing them to attain uniform color intensity and handle inventory more efficiently.

Food Colors Market Share, By Solubility, 2025 (%)

| Segments | Shares (%) |

| Water-Soluble | 74.3% |

| Oil-Dispersible | 25.7% |

How did the Water-Soluble Segment Dominate the Food Colors Market?

The water-soluble segment dominated the largest market share of 74.3% in 2025. Consumers favor water-soluble forms for their consistent product quality and dual-use potential. They offer aesthetic and technological benefits, such as color enhancement, improved appearance, and increased consumer appeal. The growth of the worldwide beverage sector, especially, has significantly fueled demand for water-soluble colors, which are widely used in beverages to provide distinct colors and visual appeal.

The Oil-Dispersible Segment is Expected to Grow at the Fastest CAGR of 6.7% in the Market During the Forecast Period

Owing to the diverse uses of oil-soluble food dyes in chocolate, sweets, baked goods, dairy items, flavoring, and coloring. They can fulfill consumer needs for sustainably sourced, natural, and health-focused food items. The oil-soluble versions are a secure alternative to artificial dyes and enhance the visual appeal of food and drink items.

Which Application Segment Dominated the Food Colors Market?

The beverages segment led the market, accounting for 42.3%, driven by strong consumer interest in vibrant drinks, the aesthetic significance of color in beverages, and the widespread use of natural and artificial colors in products such as juices, soft drinks, and functional beverages. The increasing demand for ready-to-drink beverages, along with the shift towards natural colorants, has driven market growth in this sector.

The Bakery & Confectionery Segment is Observed to Grow at the Fastest CAGR of 6.7% During the Forecast Period.

Bright colors are crucial for enhancing products such as cakes, candies, cookies, and pastries, attracting consumers and impacting their buying choices. The demand is driven by changing consumer behavior, the expansion of convenience foods, and the growing use of specialized e-commerce platforms for bakery and confectionery products.

Sensient Food Colors

By Type

By Form

By Solubility

By application

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Food Colors Market