April 2026

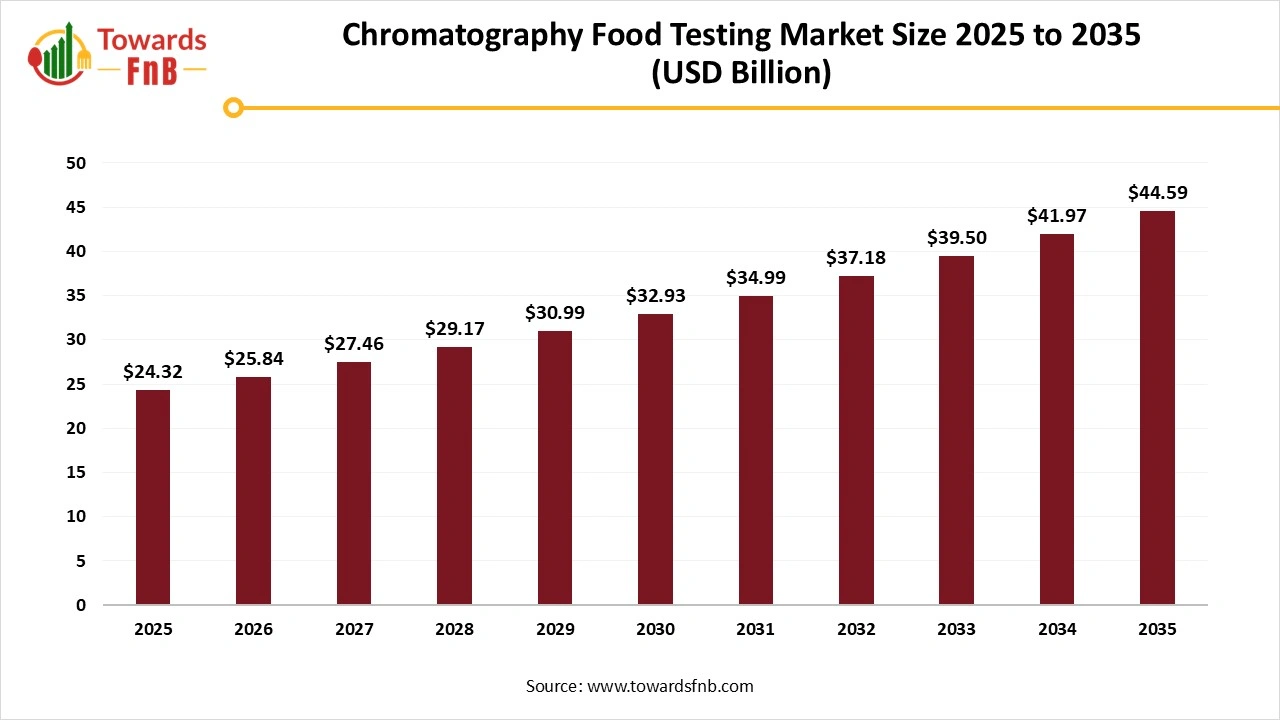

The global chromatography food testing market size stood at USD 24.32 billion in 2025 and is expected to grow steadily from USD 25.84 billion in 2026 to reach nearly USD 44.59 billion by 2035, with a CAGR of 6.25% during the forecast period from 2026 to 2035. The market is expanding due to rising concerns over food safety, quality, and authenticity.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.25% |

| Market Size in 2026 | USD 25.84 Billion |

| Market Size in 2027 | USD 27.46 Billion |

| Market Size by 2035 | USD 44.59 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The chromatography food testing market encompasses the development, supply, and use of chromatographic techniques and instruments for analyzing food safety, quality, and authenticity. This includes High-Performance Liquid Chromatography (HPLC), Gas Chromatography (GC), Ultra-Performance Liquid Chromatography (UPLC), and ion chromatography to detect contaminants, pesticides, additives, mycotoxins, antibiotics, heavy metals, allergens, and nutritional composition.

Growth is driven by rising food safety regulations, increasing consumer awareness of food quality, adoption of advanced analytical technologies, growing demand for processed food and packaged foods, and expansion of testing laboratories across the globe.

Innovations in chromatography technology have significantly improved food testing by boosting speed, sensitivity, and overall thoroughness. Methods such as Ultra-High Performance Liquid Chromatography (UHPLC) enable swift detection of various trace contaminants and improve the resolution of intricate food matrices, while sophisticated coupling with mass spectrometry (MS), including LC-MS/MS and HRMS, delivers unmatched sensitivity for identifying both known and unknown compounds. Innovations also encompass more effective sample preparation techniques such as QuEChERS, compact and portable devices for on-site testing, and the incorporation of artificial intelligence for data analysis, all of which lead to increased speed.

Research & Development

Manufacturing

Testing Services

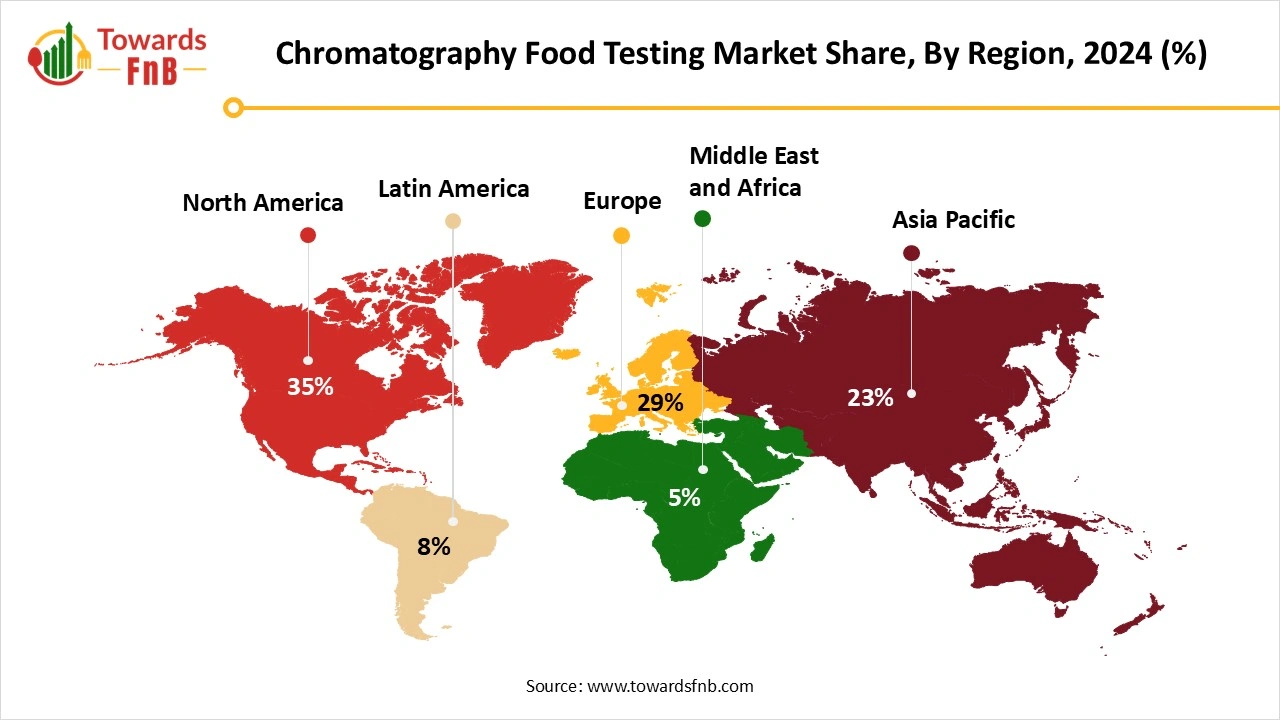

North America Dominated the Chromatography Food Testing Market with Approximately 36% Share in 2025

This increase arises from stricter food safety regulations, heightened public awareness of foodborne incidents via media reports, and rising consumer demand for clear food labeling. With companies participating more in global trade of fresh produce, meat, and processed foods, supply chains have grown more intricate, resulting in increased contamination risks and expanded testing needs.

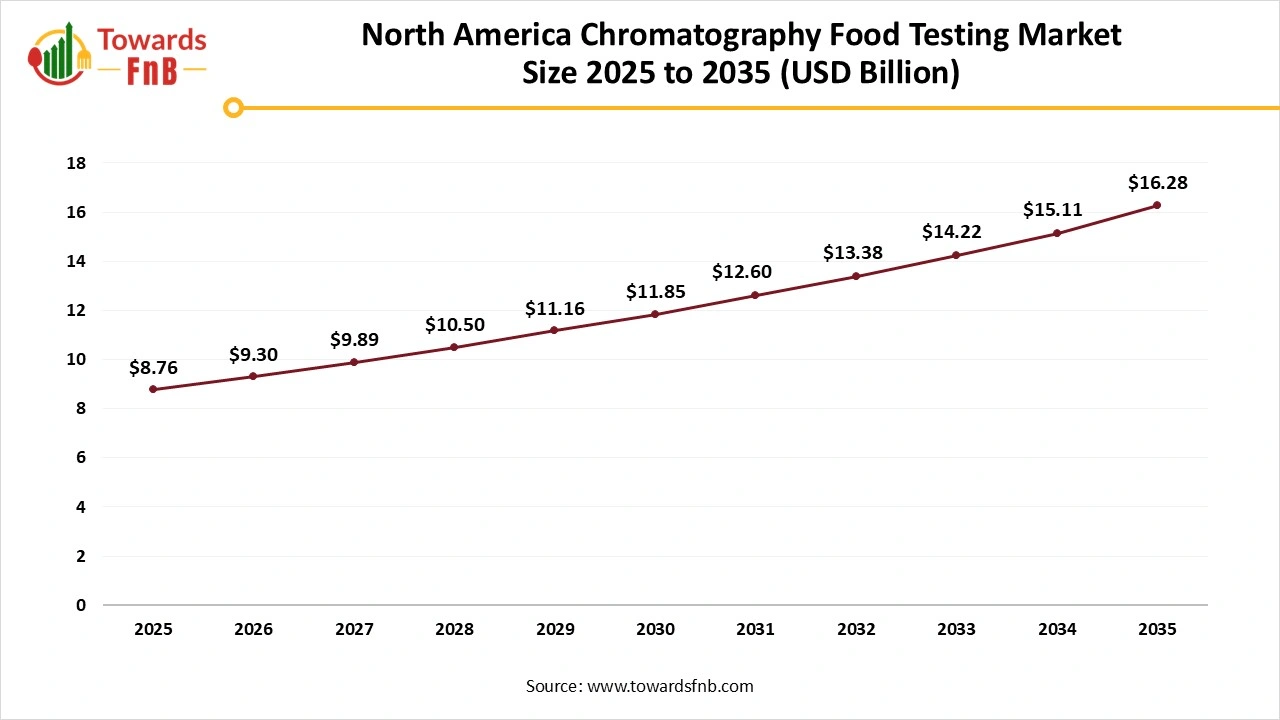

North America Chromatography Food Testing Market Size and Growth 2025 to 2035

The North America chromatography food testing market size was valued at USD 8.76 billion in 2025 and is expected to grow steadily from USD 9.30 billion in 2026 to reach nearly USD 16.28 billion by 2035, with a CAGR of 6.39% during the forecast period from 2026 to 2035.

U.S. Chromatography Food Testing Market Analysis

The increase in foodborne illnesses and contamination alerts has heightened the demand for precise testing to detect pathogens, pesticides, and other hazardous contaminants in food items. The growing use of hyphenated methods such as GC-MS, heightened automation in analytical labs, increased demand for portable and compact systems, and the incorporation of AI-driven data analysis tools are influencing market dynamics and technological development paths. Consumers are more attentive to their diet, requesting greater details about food quality, ingredients, allergens, and nutritional information and boosting the U.S chromatography food testing market.

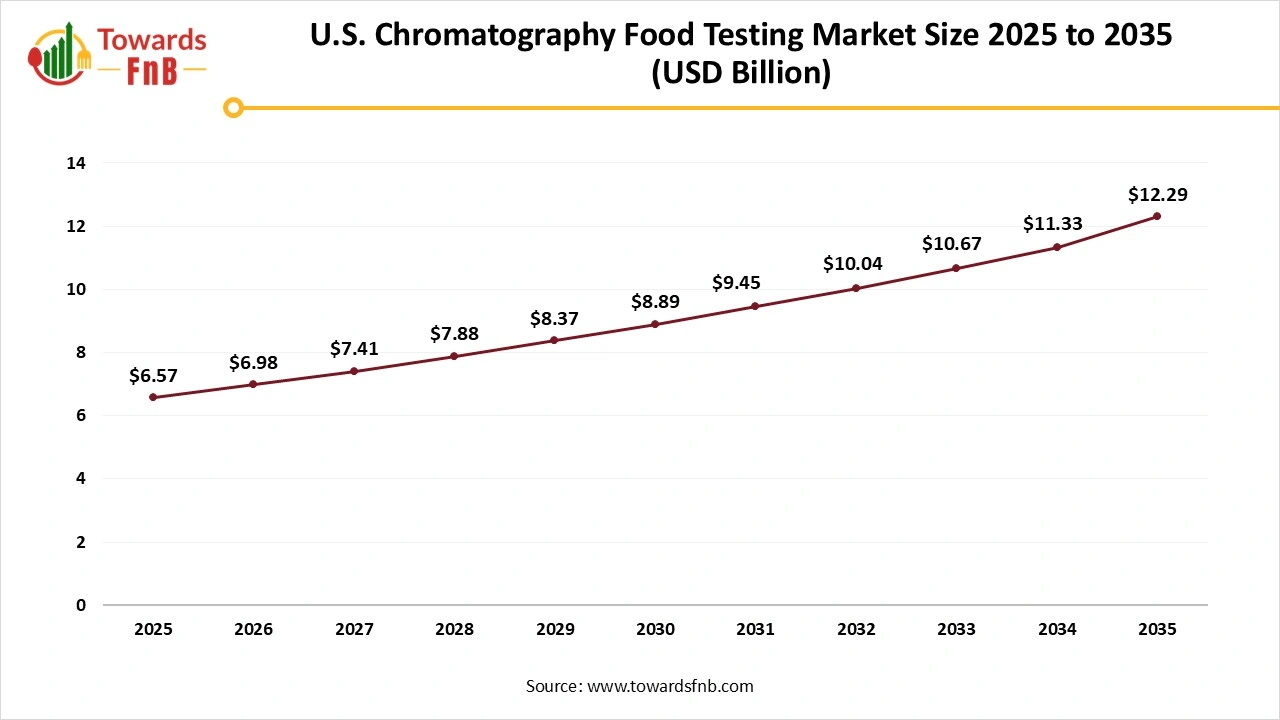

U.S. Chromatography Food Testing Market Size and Growth 2025 to 2035

The U.S. chromatography food testing market size was calculated at USD 6.57 billion in 2025 and is expected to grow steadily from USD 6.98 billion in 2026 to reach nearly USD 12.29 billion by 2035, with a CAGR of 6.46% during the forecast period from 2026 to 2035.

Asia Pacific Chromatography Food Testing Market Trends

Asia Pacific is anticipated to experience significant CAGR of approximately 27% share in the market during the forecast period, driven by the robust pharmaceutical, biotechnology, food and beverage, and environmental industries in the region. The area is progressively emerging as a center for advanced manufacturing, research and development efforts, and superior testing, transforming it into a vital market for chromatography equipment. Nations such as China, India, Japan, South Korea, and Australia are rising as key participants in the market, featuring an increasing number of pharmaceutical and food processing sectors that demand dependable and precise testing techniques. In Japan, advancements in chromatography technologies, especially in high-performance liquid chromatography (HPLC) and gas chromatography (GC), are influencing trends throughout the entire region.

China Chromatography Food Testing Market Analysis

China's focus on environmental and food safety regulations encourages the use of chromatography for analyzing contaminants and additives. Moreover, swift technological progress has led to the development of more advanced liquid chromatography systems, improving the precision and effectiveness of testing procedures. This trend is evident in the increasing use of high-performance liquid chromatography (HPLC) in labs throughout China, addressing the demand for accurate analysis.

Europe Chromatography Food Testing Market Trends

The European is anticipated to expand at notable rate in the market during the forecast period, due to strict food safety regulations, increasing consumer awareness about food quality, and a complex food supply chain. With the ongoing emergence of complications from foodborne illnesses and contamination events, governments and food producers have invested substantial portions of their budgets in food testing services to comply with safety standards and maintain consumer confidence. The industry is presently marked by the rapid implementation of innovative analytical methods and automation, resulting in enhanced accuracy, efficiency, and dependability of food testing services.

")

Germany Chromatography Food Testing Market Analysis

The need for chromatography in Germany's food testing industry is robust and increasing, mainly fueled by strict food safety regulations from the European Union and Germany. Stringent EU regulations and national standards imposed by organizations such as the German Federal Institute for Risk Assessment (BfR) require accurate testing for various contaminants. This ongoing push for adherence increases the need for advanced analytical technologies such as chromatography. The market is experiencing a swift transition towards increasingly automated, precise, and high-throughput chromatography systems, which encompass miniaturized and portable devices.

Chromatography Food Testing Market Share, By Technique/Technology, 2025 (%)

| Segments | Shares (%) |

| High-Performance Liquid Chromatography (HPLC) | 39% |

| Gas Chromatography (GC) | 20% |

| Ultra-Performance Liquid Chromatography (UPLC) | 14% |

| Ion Chromatography (IC) | 15% |

| Thin Layer Chromatography (TLC) & Others | 12% |

Why did the High-Performance Liquid Chromatography (HPLC) Segment Dominate the Chromatography Food Testing Market in 2025?

High-performance liquid chromatography (HPLC) segment led the market with approximately 39% share in 2025. This rapid expansion is fueled by heightened regulatory examination, the escalating demand for quality control, and the increasing intricacy of food and beverage compositions that necessitate accurate analytical methods. The expected growth of the market is due to improvements in high-performance liquid chromatography technology, which have increased the reliability and efficiency of liquid chromatography procedures. HPLC systems, renowned for their unmatched sensitivity and specificity, are perfectly designed to investigate intricate matrices, measure micronutrients, and identify adulterants at minimal concentrations. The continuous advancements in have improved the efficiency and output of HPLC systems, making them more appealing and available to both major manufacturers and small-scale producers.

Ultra-Performance Liquid Chromatography (UPLC) Segment is Observed to Grow at the Fastest CAGR of Approximately 18% During the Forecast Period

Due to the growing demand for swift, sensitive, and high-throughput evaluation of food safety factors such as pesticide residues, contaminants, and nutritional elements. UPLC technology, frequently paired with mass spectrometry (UPLC-MS), is essential for adhering to rigorous international quality standards and guaranteeing consumer safety, with uses in identifying additives, contamination, and harmful substances in various food items. The market is anticipated to expand, driven by its effectiveness in decreasing analysis time and solvent usage relative to conventional techniques.

Chromatography Food Testing Market Share, By Food Type Tested, 2025 (%)

| Segments | Shares (%) |

| Fruits & Vegetables | 25% |

| Dairy & Dairy Products | 15% |

| Meat & Poultry | 14% |

| Processed & Packaged Foods | 16% |

| Seafood & Aquaculture Products | 12% |

| Beverages (Juice, Soft Drinks, Alcoholic) | 8% |

| Grains & Cereals | 10% |

How did the Fruits & Vegetables Segment Dominate the Chromatography Food Testing Market in 2025?

Fruits and vegetables segment held the dominating share of the market with approximately 25% share in 2025. Fruits and vegetables are eaten worldwide in substantial amounts, which inherently raises the demand for testing throughout the supply chain. This area is very vulnerable to pesticide application during farming, which renders pesticide residue testing essential for safety and adherence. Stringent governmental regulations and standards regarding maximum residue limits (MRLs) for pesticides necessitate comprehensive testing to ensure compliance with these criteria. Increasing consumer awareness and demand for products that have minimal or no chemical contamination is fueling the necessity for testing.

Processed & Packaged Foods Segment is Seen to Grow at a Notable CAGR of Approximately 16% Share During the Predicted Timeframe

The prepared food sector is expanding considerably because of the rising demand for ready-to-eat and packaged meals. These items frequently include several components, increasing the likelihood of contamination during manufacturing and storage. Increasing health worries and a demand for clean-label items are enhancing safety inspections. Producers are allocating resources for testing to guarantee product quality and adherence to regulations.

Chromatography Food Testing Market Share, By End User, 2025 (%)

| Segments | Shares (%) |

| Food Testing Laboratories | 39% |

| Contract Research Organizations (CROs) / Testing Services | 18% |

| Food & Beverage Manufacturers | 16% |

| Government & Regulatory Agencies | 15% |

| Academic & Research Institutes | 12% |

Which End User Segment Dominated the Chromatography Food Testing Market in 2025?

Food testing laboratories segment dominated the market with the approximately 39% share in 2025, because of the growing need for food safety and quality assurance, fueled by consumer awareness, stricter regulations, and concerns about foodborne illnesses. Laboratories offer extensive services employing sophisticated chromatography methods to identify contaminants, allergens, and other detrimental substances, guaranteeing adherence to regulations and fostering consumer confidence. The growth of international food trade requires thorough testing for contamination across borders. Improvements in chromatography and associated technologies are allowing for more precise, effective, and quicker testing, positioning laboratories as crucial centers for integrating and utilizing these novel approaches.

Food & Beverage Manufacturers Segment is Expected to Grow at the Fastest CAGR of Approximately 20% Share in the Market During the Forecast Period

To market their products in both local and global markets, F&B manufacturers must comply with a complicated and growing array of government regulations. Chromatography is an effective method for showing adherence to these standards. With consumers becoming increasingly knowledgeable and health-aware, they demand greater safety and transparency from the products they buy. Ensuring uniform product quality is essential for safeguarding a brand's image and customer loyalty. Chromatography is employed for quality assurance at each stage of the production process.

Thermo Fisher Scientific

Thermo Fisher Scientific Inc.

Axcend®

By Technique/Technology

By Food Type Tested

By End User

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

March 2026

Chromatography Food Testing Market