April 2026

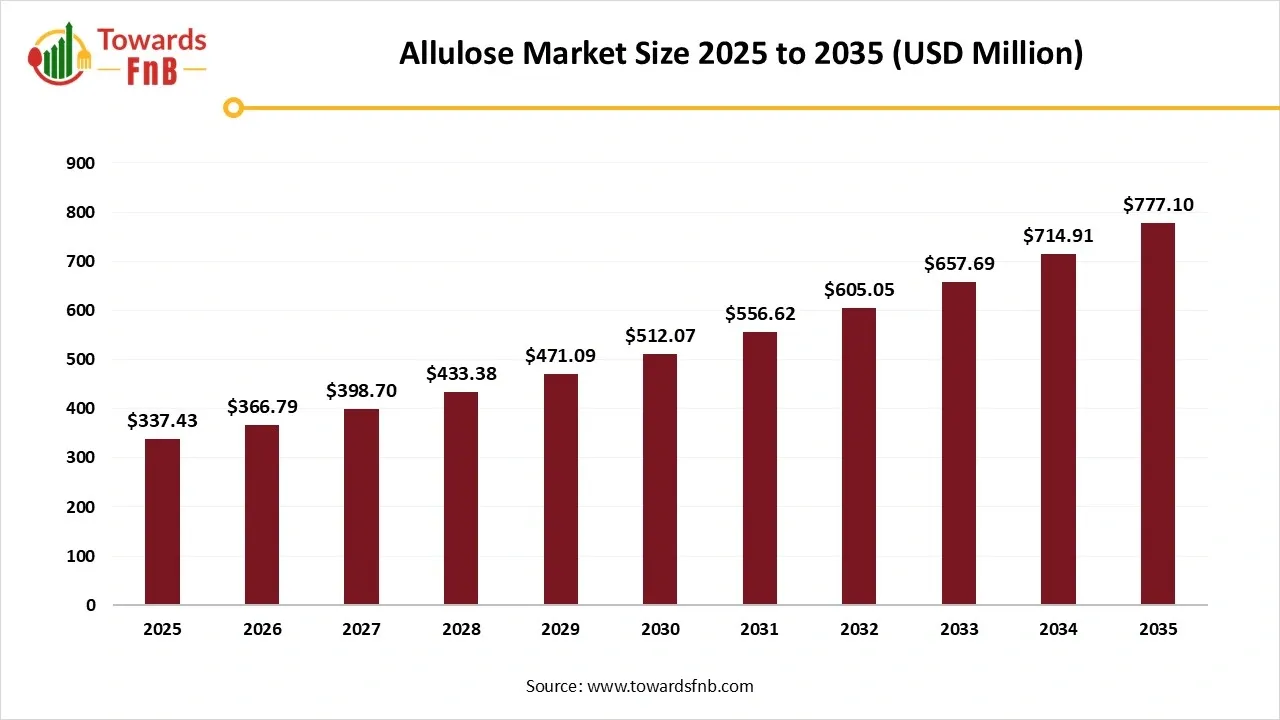

The global allulose market size reached at USD 337.43 million in 2025 and is expected to grow steadily from USD 366.79 million in 2026 to reach nearly USD 777.10 million by 2035, with a CAGR of 8.7% during the forecast period from 2026 to 2035. Allulose is gaining traction in the market because it serves as an alternative to sugar, providing the same sweet taste and better affordability rates with assurance of no side effects to the human body.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 8.7% |

| Market Size in 2026 | USD 366.79 Million |

| Market Size in 2027 | USD 398.70 Million |

| Market Size by 2035 | USD 777.10 Million |

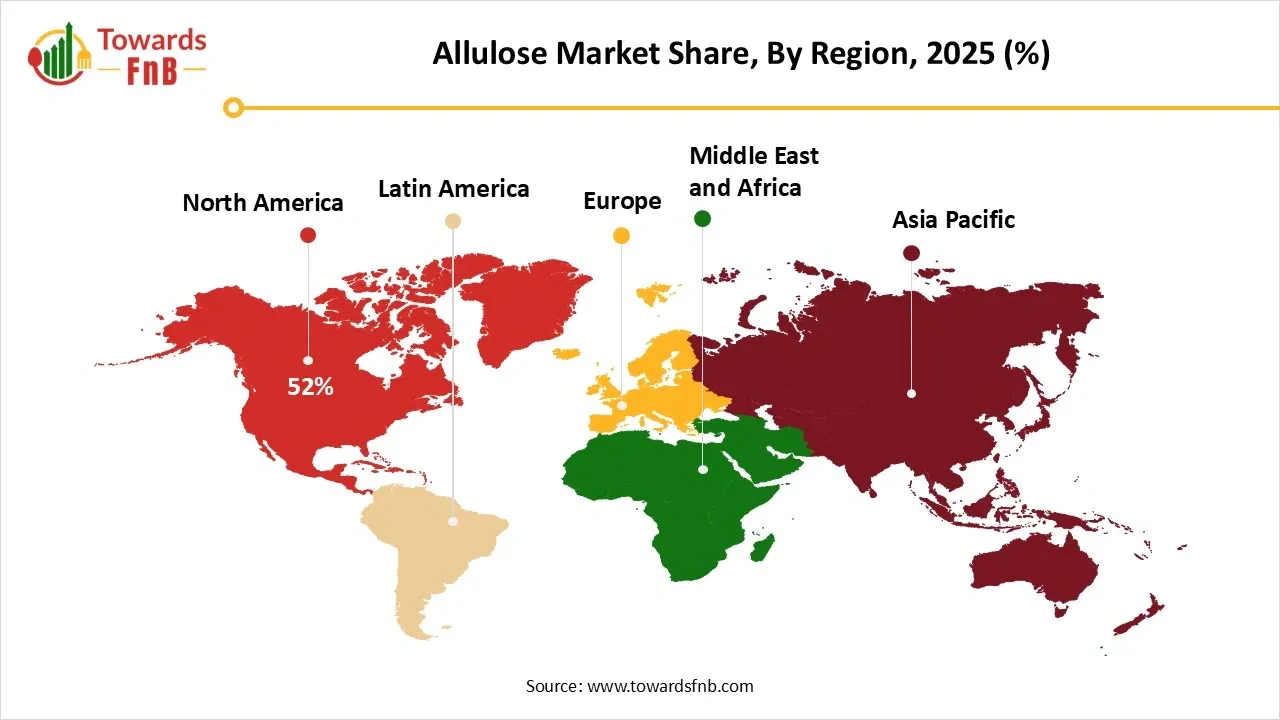

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The allulose market refers to the global industry for allulose, a low-calorie rare sugar that mimics the taste and texture of regular sugar but contains only a fraction of the calories. Due to its negligible impact on blood glucose and insulin levels, it is gaining popularity in diabetic-friendly, keto, and low-calorie food and beverages formulations. Allulose is naturally found in small quantities in foods like figs and raisins but is mostly produced through enzymatic conversion from fructose. Its growing acceptance by regulatory bodies (e.g., U.S. FDA excludes it from total and added sugars labelling) further boosts market expansion.

The market is experiencing rapid growth as consumers and food manufacturers alike seek healthier alternatives to sugar. It's a zero-glycaemic ingredient for diabetic-friendly, keto, and weight management products. Major food and beverage players are reformulating products to include allulose, aligning with the global push toward sugar reduction. While North America currently leads the market, it is emerging as a strong contender due to increasing awareness and evolving dietary preferences. Regulatory support in key regions has further fueled its adoption, encouraging innovation in confectionery, bakery, and beverages. As the spotlight shifts from artificial sweeteners to natural and functional options, allulose is carving out a significant niche.

Samyang Corporations

Customer Analysis (Target Audience and Techniques to Attract Customers)

| 18-25 (Generation Z) | 30-40 age group |

| These consumers are increasingly health-conscious and attentive to taste and clear nutrition, aligning with trends in the Allulose Market. Young adults are more likely to adopt flexible diets such as flexitarian, vegan, or dairy-limited, seeking products that complement these lifestyles. They prefer high-protein and functional foods to support their routines. | families with young children and seniors are turning to products like caviar drinks for digestive health, indicating a broader demographic interest in health benefits. Overall, the customer base for the Allulose Market includes health-conscious individuals across various age groups who prioritize nutrition, dietary flexibility, and functional food options. |

The allulose market presents strong potential due to rising consumer demand for healthier sugar alternatives. As obesity, diabetes, and metabolic disorders increase globally, products with low glycemic impact like allulose are gaining traction. Its natural origin and close resemblance to sugar in taste give it a competitive edge over other sweeteners. Food and beverage manufacturers are increasingly incorporating allulose in categories like snacks, beverages, bakery, and dairy. With regulatory approvals expanding across regions, there's room for scale and innovation. The clean-label and low-calorie movement further opens up premium product positioning and niche market growth.

Despite its promise, the allulose market faces several hurdles. Limited global regulatory approval still restricts its use in many countries, slowing down widespread adoption. High production costs compared to traditional sweeteners make it less accessible for budget-conscious brands. Consumer awareness remains low in emerging markets, which affects demand despite health benefits. Technical formulation issues, such as browning in baking or solubility in beverages, can limit its application. Lastly, competing sweeteners like stevia or erythritol, already well-established and often cheaper, pose strong market resistance.

How is North America Leading the Sweet Shift?

North America dominated the allulose market in 2025, driven by strong consumer demand for healthier food choices. The rise in lifestyle diseases like diabetes and obesity has made low-calorie sweeteners a dietary priority. Food manufacturers are rapidly incorporating allulose into reformulated snacks, beverages, and desserts. The region’s well-established health food industry and innovation-friendly regulatory environment have accelerated adoption. Major brands and startups alike are investing in clean-label sweetener alternatives, with allulose standing out due to its sugar-like taste.

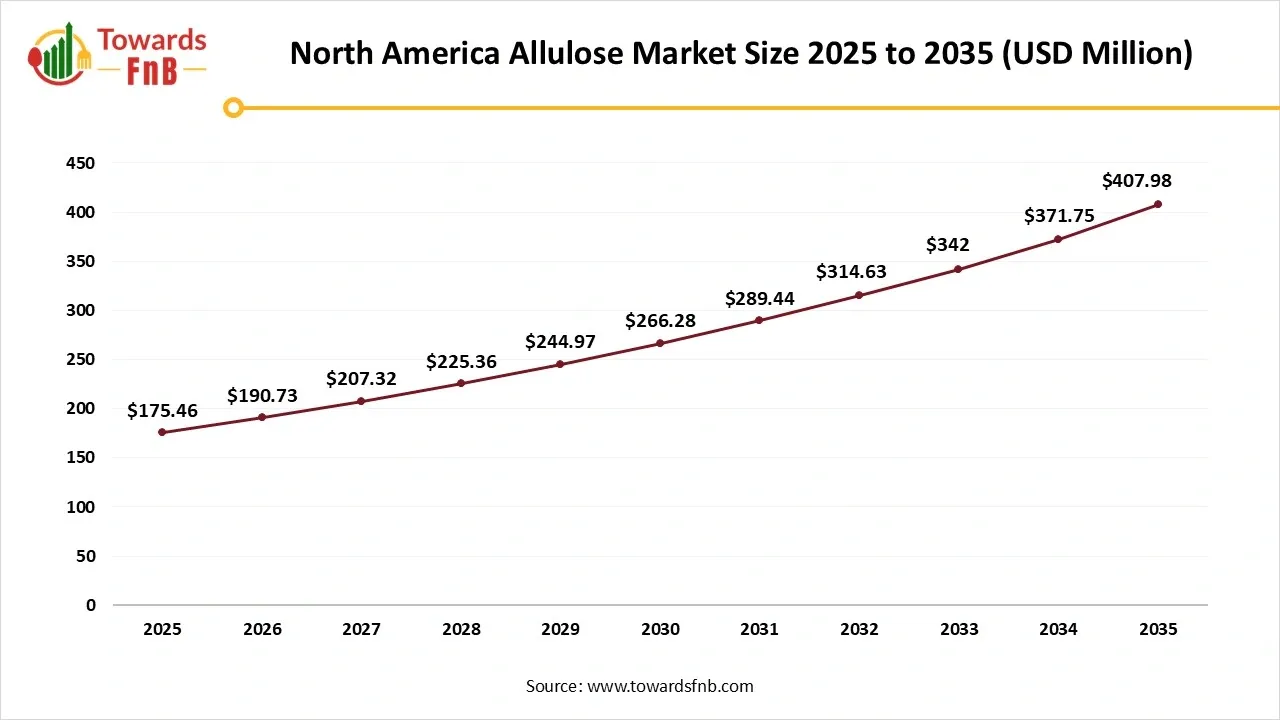

North America Allulose Market Size 2025 to 2035

The North America allulose market size was valued at USD 175.46 million in 2025 and is expected to grow steadily from USD 190.73 million in 2026 to reach nearly USD 407.98 million by 2035, with a CAGR of 8.8% during the forecast period from 2026 to 2035.

The U.S. represents the dominance in North America; this regulatory clarity has encouraged its use across mainstream food categories. American consumers, increasingly label-conscious, are turning to sugar substitutes that deliver both taste and health benefits. The keto and low-carb trends have further fueled demand for allulose-based formulations. With major food chains and wellness brands promoting sugar reduction, allulose is steadily becoming a staple. Continued R&D investment and consumer trust position the U.S. as a long-term leader in allulose innovation.

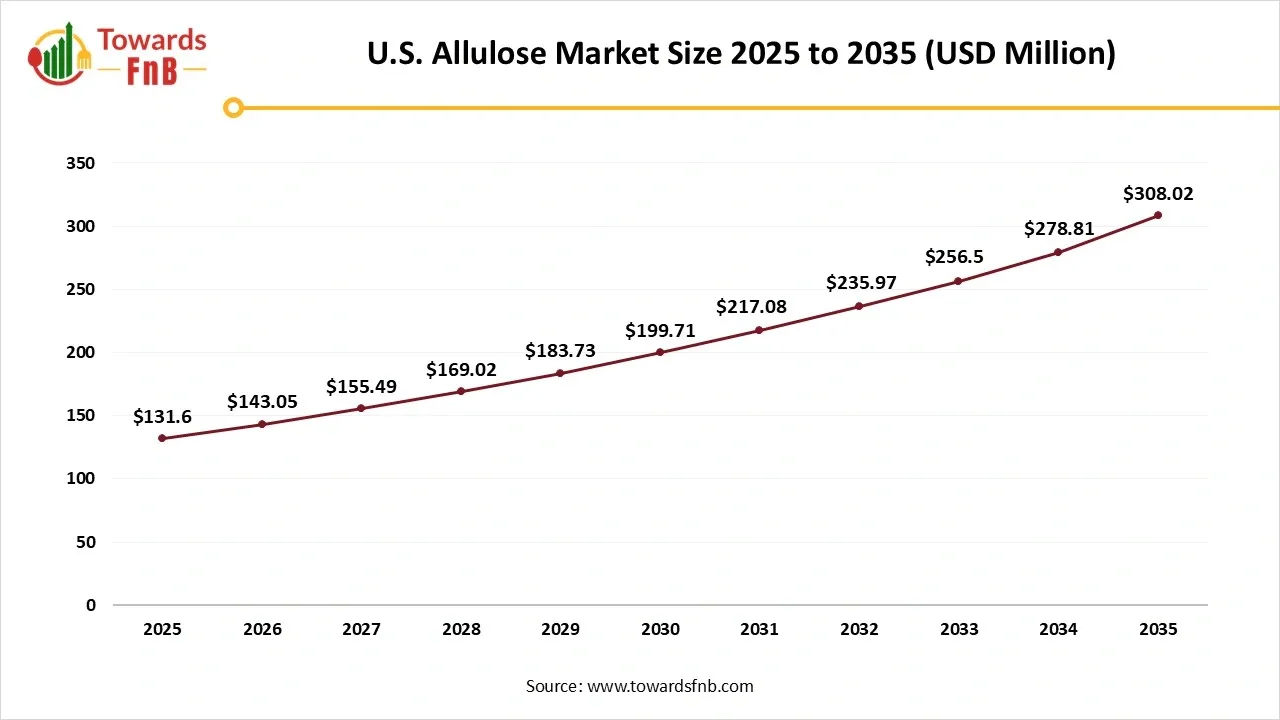

U.S. Allulose Market Size 2025 to 2035

The U.S. allulose market size was calculated at USD 131.6 million in 2025 and is expected to grow steadily from USD 143.05 million in 2026 to reach nearly USD 308.02 million by 2035, with a CAGR of 8.88% during the forecast period from 2026 to 2035.

Is Asia Pacific a Sweet Innovator at High Speed?

Asia Pacific expects the fastest growth in the allulose market during the forecast period, powered by urbanization and rising health awareness. Consumers are becoming more proactive about managing sugar intake, especially in urban centers. The region’s large population and evolving dietary habits offer massive market potential. Food and beverage companies are increasingly exploring allulose to differentiate their products from sugar-loaded competitors. Governments across Asia are also beginning to support sugar reduction initiatives, indirectly boosting demand.

India is emerging as the key player in Asia pacific allulose market, growing concerns about diabetes and obesity are reshaping consumer choices toward healthier sweeteners. Traditional Indian diets are being blended with modern health-conscious alternatives, giving room for new ingredients like allulose. Although consumer awareness is still growing, urban populations are showing increased interest in clean-label, sugar-free products. Ayurveda-inspired wellness brands are also beginning to experiment with metabolic-friendly ingredients. The country’s strong food processing sector offers room for innovation and integration of allulose in snacks, sweets, and beverages.

")

Europe Allulose Market Growth

The allulose market in Europe is experiencing substantial growth, driven by an increasing consumer preference for low-calorie, natural sugar substitutes. As health consciousness continues to rise across the region, manufacturers are innovating to cater to the evolving demands for clean-label and functional sweeteners. Key markets such as Germany, the United Kingdom, and France collectively hold a considerable market share. The rising adoption of allulose in various food and beverage applications, alongside advancements in production and formulation techniques, positions Europe as a crucial region for the growth trajectory of the global allulose market.

Germany Allulose Market Analysis

Germany's allulose market is experiencing robust expansion, fueled by a health-conscious populace and stringent regulations that favor the use of natural sweeteners. The demand for low-calorie foods ingredients is driving manufacturers to incorporate allulose into a diverse array of products, including baked goods and beverages. This market growth is further supported by technological advancements in extraction and production processes that ensure a high-quality and cost-effective supply. Additionally, increasing consumer awareness regarding the benefits of sugar alternatives is creating regional opportunities for innovative product development and market penetration.

Allulose Market Share, By Form, 2025 (%)

| Segments | Shares (%) |

| Powder | 49% |

| Liquid | 30% |

| Crystal | 21% |

How is Powdered Form Dominating the Allulose Market?

The powder segment dominated the market in 2025, due to its superior stability, ease of storage, and longer shelf life. It blends seamlessly into dry mixes, baked goods, and powdered drink formulations, making it the preferred choice for manufacturers. Its resemblance to table sugar also makes it appealing for consumers switching to low-calorie alternatives. Food processing companies prefer powdered formats for bulk handling and cost efficiency. Its use in protein bar, cookies, and snack mixes further strengthens its market share. With its versatility across food systems, powdered allulose is firmly established as the dominant form.

The Liquid Segment Expects the Fastest Growth in the Market During the Forecast Period

Because it offers excellent solubility and convenience in manufacturing processes, particularly for ready-to-drink products. As demand for clean-label, low-sugar drinks rises, liquid allulose is becoming a go-to ingredient for natural sweetness. It is also easier to blend with other liquid ingredients, making it ideal for formulating functional beverages and liquid supplements. Health-conscious brands are actively experimenting with it in dressings, smoothies, and flavored waters. With consumer trends favoring convenience and drinkable nutrition, liquid allulose is gaining rapid ground.

Allulose Market Share, By Source, 2025 (%)

| Segments | Shares (%) |

| Corn-Based | 55% |

| Sugar Beet-Based | 15% |

| Sugarcane-Based | 15% |

| Fruit-Based | 15% |

How Corn-Based Segment is Leading the Allulose Market?

The corn-based segment dominated the market in 2025, due to its abundant availability and cost-effective production. The established corn supply chain provides manufacturers with scalability and consistency. Its production technology is mature, making it a go-to option for large-scale use in food and beverage products. Many North American producers rely on corn as a dependable raw material. Corn-based allulose is widely accepted across regulatory bodies, further cementing its leading position. Its economic viability keeps it at the center of commercial formulations.

Fruit-Based Expects the Fastest Growth in the Allulose Market During the Forecast Period

Due to its natural and label-friendly appeal. Extracted from sources like figs, raisins, and jackfruit, it resonates with clean-eating consumers. Brands focused on organic and minimally processed ingredients are beginning to choose fruit-based allulose over synthetic or grain-derived types. Although production is currently limited and more expensive, demand is rising in premium product categories. Health-conscious segments are especially drawn to its closer-to-nature positioning. As innovation scales up, fruit-based allulose could redefine what natural sweetness means.

Allulose Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Food & Beverages | 64% |

| Bakery | 10% |

| Dairy | 5% |

| Confectionery | 5% |

| Sauces & Dressings | 5% |

| Beverages | 5% |

| Nutraceuticals & Dietary Supplements | 10% |

| Pharmaceuticals | 5% |

| Personal Care Products | 5% |

Why Food and Beverages is Dominating the Allulose Market?

The food and beverages segment dominated the market in 2025, due to its versatility and sugar-like taste. It is widely used in baked goods, snacks, beverages, dairy, and frozen dessert. With rising demand for sugar reduction in mainstream products, manufacturers are rapidly turning to allulose. Its ability to mimic sugar's taste and texture without calories makes it ideal for both indulgent and functional products. It’s also heat-stable, which is a big advantage in food processing. From reformulated classics to innovative launches, allulose is now a kitchen essential for many brands.

The Nutraceuticals & Dietary Supplements Segment Expects the Fastest Growth in the Market During the Forecast Period

As consumers look for palatable options in wellness products, allulose provides sweetness without compromising health goals. It is being integrated into protein powders, meal replacement shakes, gummies, and fiber blends. Its low glycemic index aligns perfectly with blood sugar management supplements. Formulators appreciate its solubility, stability, and ability to mask the unpleasant tastes of actives. With functional nutrition booming, allulose is becoming a vital tool in supplement formulation.

Allulose Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| B2B (Direct Sales to Manufacturers) | 61% |

| B2C (Retail - Online & Supermarkets) | 25% |

| Ingredient Distributors | 14% |

Why did B2B Segment Dominated the Allulose Market in 2025?

The B2B segment dominated the market in 2025, due to its ability to replace sugar without affecting product quality. Major brands are reformulating everything from soft drinks to cookies to cater to health-conscious consumers. Allulose helps meet sugar-reduction targets without sacrificing flavor, making it ideal for mass-market reformulations. Its performance in texture, browning, and sweetness gives it a competitive edge over many alternatives. The global push toward low-calorie diets continue to fuel adoption in this segment. As consumer palates evolve, food and beverage applications remain the engine of demand.

The B2C Segment Expects the Fastest Growth in the Allulose Market During the Forecast Period

As individuals become more ingredient-conscious and proactive about healthy living. Allulose is now sold through online platforms and health-focused retail stores in standalone packets, jars, and blends. Home bakers, fitness enthusiasts, and diabetic consumers are major buyers in this space. Brands are leveraging social media and influencer marketing to promote allulose’s benefits. With e-commerce expanding, convenience and transparency are driving B2C growth. Personalized health trends are turning B2C into an exciting new frontier for allulose.

Two spoons Creamery

In September 2025

In October 2024

By Form

By Source

By Application

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Allulose Market