April 2026

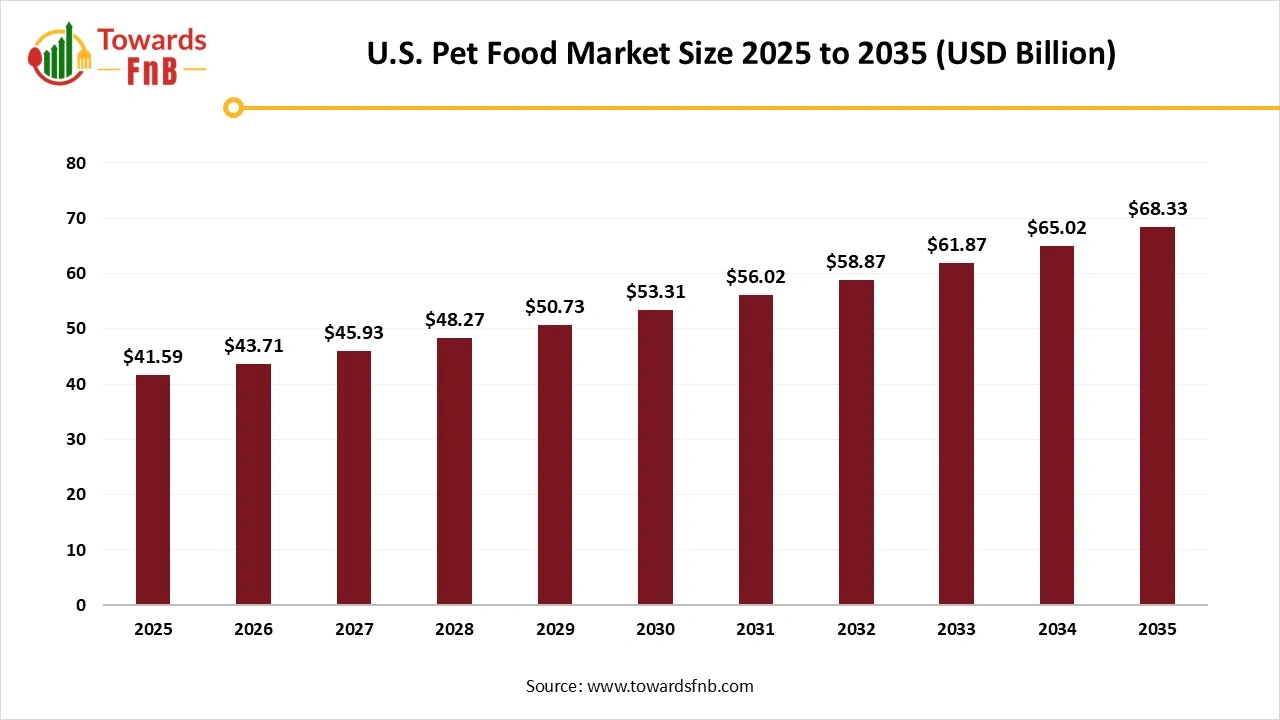

The U.S. pet food market size reached at USD 41.59 billion in 2025 with projections indicating a rise from USD 43.71 billion in 2026 to reach approximately USD 68.33 billion by 2035, expanding at a CAGR of 5.09% throughout the forecast period from 2026 to 2035. The increasing demand for customized, organic, and premium pet food options in the United States drives the growth of the market.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.09% |

| Market Size in 2026 | USD 43.71 Billion |

| Market Size in 2027 | USD 45.93 Billion |

| Market Size by 2035 | USD 68.33 Billion |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The U.S. pet food market refers to the domestic industry engaged in the manufacturing, distribution, and sale of food and nutritional products for pets, primarily cats and dogs, but also birds, fish, reptiles, and small mammals. With rising pet ownership, humanization of pets, and growing awareness of animal nutrition, the market is driven by demand for premium, natural, organic, and functional pet food. E-commerce adoption, customized diets, and veterinary-approved formulas are also shaping the industry.

One of the major significant factors driving the growth of the market is the increasing pet ownership. The rapidly increasing pet personalized and metropolitan areas are encouraging pet owners to choose quality and nourishing food for their pets, which helps fuel market growth. In addition, to assisting pets’ health, the rising per-person income of pet owners motivates them to spend on natural and wholesome food products for their pet animals. Furthermore, increasing pet population across the globe, increasing pet humanization, growing expansion of e-commerce pet food sales, and increasing demand for premium pet food are further expected to drive the growth of the market.

The rising technological advancements in pet food are revolutionizing market growth. Rising technological advancements are transforming pet feeding with automated feeders that ensure pets are fed regularly and dispense food at scheduled times. Smart bowls tailored with connectivity and scales to mobile apps can provide dietary recommendations, track nutritional metrics, and monitor food intake, which may create major opportunities in the market. In addition, the rising fresh and raw food movement, increasing focus on health-focused and functional food, and personalized nutrition are further expected to revolutionize the growth of the market in the coming future.

In the Western markets, pet food is one of the most regulated foods. Pet animal foods are studied strictly at every level in the established market. The increase in rigidity linked with commercialization can be a major challenging factor restraining market growth. In addition, less acknowledgment for high-quality or qualitative pet food across various emerging markets can also be a major hindering factor, which further restrains the growth of the market.

The recent introduction of the Agricultural Export Promotion Act in January 2025 is a positive development for strengthening U.S. agricultural exports, including pet food. This legislation secures funding for the Market Access Program (MAP), which PFI proudly participates in, supporting the industry's efforts to remain competitive in the global market through strategic support and advocacy.

PFI continues to be a strong collaborator in the MAP program, which supports U.S. pet food exports to 19 countries. Notably, 18 of these countries ranked among the top 35 export markets for U.S. pet food in 2024, showcasing an increase from the previous year.

Raw Material Procurement

Processing

Quality Control

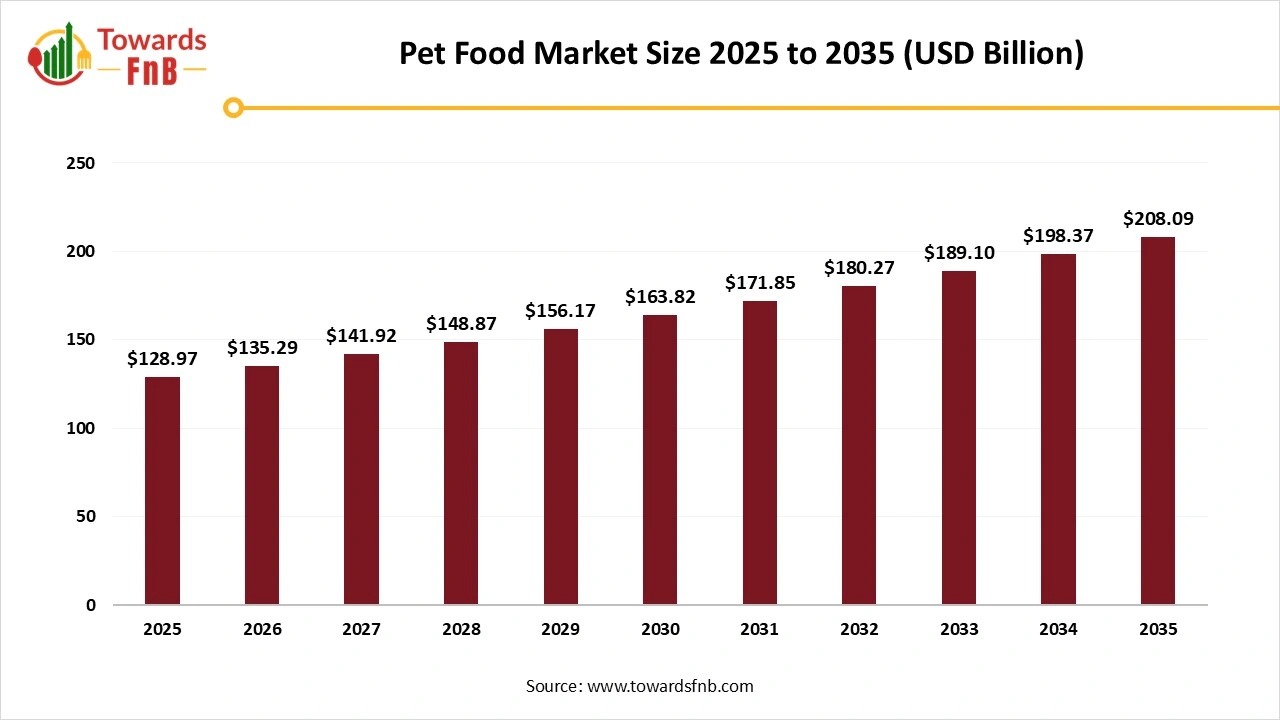

The global pet food market was valued at USD 128.97 billion in 2025 and is expected to rise from USD 135.29 billion in 2026 to reach around USD 208.09 billion by 2035, reflecting a CAGR of 4.9% over the forecast period from 2026 to 2035. Growth is fueled by factors such as the rising rate of pet ownership, the humanization of pets, greater focus on pet health, and the rapid expansion of the pet food industry.

U.S. Pet Food Market Trends

The market growth in the U.S. is attributed to factors such as the increasing demand for personalized snack packs, increasing innovative packaging solutions such as biodegradable and resealable options, and increasing adoption of cutting-edge processing technologies to enhance nutritional content, flavor, and product quality. About 86 million American households are rapidly adopting pets in the U.S., according to the American Pet Product Association, which contributed to propel the market growth in the U.S.

U.S. Pet Food Market Share, By Pet, 2025 (%)

| Segments | Shares (%) |

| Dogs | 70% |

| Cats | 15% |

| Fish | 5% |

| Birds | 2% |

| Small Mammals | 3% |

| Reptiles | 1% |

| Others | 4% |

How Dogs Segment Dominates U.S. Pet Food Market Revenue in 2025?

The dogs segment dominated the market revenue in 2025. The segment growth in the market is attributed to the increasing rapid adoption of dogs and dog food via online and retail channels, increasing demand for functional, natural and premium dog food, increasing consumer trend or mentality to treat dogs as family members and increasing dog ownership.

The cats segment expects the fastest growth in the market during the forecast period. The segment growth in the market is driven by increasing demand for specialized nutrition, health-focused and premium products, increasing cat ownership, increasing urbanization, and increasing popularity of cats.

Why Dry Pet Food Segment Held the Largest U.S. Pet Food Market Revenue in 2025?

The dry pet food segment dominated the U.S. pet food market in 2025. The segment growth in the market is driven by benefits such as cost-effectiveness, longer shelf life, and convenience. Due to its dental health benefits, portion control, and ease of storage, various pet owners prefer dry food. In addition, the increasing availability of specialized and nutritionally balanced dry formulas, including breed-specific options, high-protein and grain-free options, is looking for tailored nutrition for their pets and attracting health-aware consumers, which is expected to drive the segment growth.

The Veterinary Diets Segment is Expected to Grow Fastest During the Forecast Period

Pet owners can receive the proper level of nutrients for their health issues, lifestyles, breed, and age by providing pets with prescription and super premium veterinary food. Veterinary diets enable pets to have healthier lives. This diet provides pets with plenty of exercise and water. Regular check-ups play an important role and ensure the pet is happy and healthy. Veterinary diets enable pets to have toned muscles and a healthy body. It includes enough protein, which helps in improving the repair mechanism of damaged cells and building organs, muscles, hair, skin, and other tissues, which is further expected to accelerate the demand for the segment.

What Factors Help Animal-derived Protein Segment Grow in 2025?

The animal-derived protein segment dominated the U.S. pet food market revenue in 2025. Animal-derived protein includes lamb, fish, beef, chicken, and various protein sources, which help pets to improve their health. In addition, the segment growth in the market is attributed to the increasing disposable incomes, rapid urbanization, increasing demand for functional and premium pet foods, increasing popularity of novel and exotic proteins, increasing demand for high-quality protein diets, and rising pet humanization.

The Functional Ingredients Segment is Expected to Grow Fastest During the Forecast Period

The functional ingredients offer specific health advantages and nutritional value. These ingredients help pets to maintain flexibility and joint health, particularly those with aging. Some functional ingredients, such as red fruits and taurine plants are rich in omega-3 fatty acids and bioflavonoids, which help a pet’s cardiovascular health. Essential fatty acids can improve heart function, maintain healthy cholesterol levels, and help reduce inflammation, which is further expected to fuel the growth of the segment in the market.

U.S. Pet Food Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Distributors/Wholesalers | 34% |

| Supermarkets/Hypermarkets | 17% |

| Pet Specialty Stores | 12% |

| Veterinary Clinics | 10% |

| Online/E-Commerce Platforms | 13% |

| DTC (Direct-to-Consumer Subscriptions) | 14% |

How Supermarkets/Hypermarkets Segment Dominates the U.S. Pet Food Market Revenue in 2025?

The hypermarkets and supermarkets dominated the U.S. pet food market in 2025. The segment growth in the market is attributed to the increasing pet food product visibility and pet owner awareness towards pet health and wellness, and increasing strategic locations, coupled with promotional activities and competitive pricing. To serve varying pet owner preferences, supermarkets and hypermarkets play an essential role in the market by providing extensive shelf space and diverse product selections. In addition, supermarkets and hypermarkets leverage their robust logistics networks to ensure consistent availability and efficient distribution, which further accelerates the segment demand.

The Online/E-commerce Platforms Segment Expects the Fastest Growth During the Forecast Period

The segment growth in the market is driven by factors such as increasing consumer trend towards online shopping, growing e-commerce platforms, increasing busy and modern lifestyles, increasing demand for online retail stores, doorstep delivery, easy return and exchange policies.

U.S. Pet Food Market Share, By Price Tier, 2025 (%)

| Segments | Shares (%) |

| Economy | 20% |

| Mid-Range | 47% |

| Premium | 15% |

| Super Premium | 18% |

Why did the Mid-Range Segment Held the Largest U.S. Pet Food Market Revenue in 2025?

The mid-range segment dominated the market in 2025. The segment growth in the market is attributed to the increasing demand for functional ingredients, increasing pet owner preference towards clean-label and natural food products, rising middle-class population, and growing pet population. In addition, the mid-range segment provides a balance between better ingredients and affordability, such as functional ingredients and real meat, which is expected to drive the segment growth.

The Premium Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in the market is propelled by factors such as increasing demand for high-quality pet food products, increasing focus on functional and preventive ingredients, growing sustainability, rising preference towards personalized food products, and growing e-commerce platforms.

U.S. Pet Food Market Share, By Packaging, 2025 (%)

| Segments | Shares (%) |

| Cans | 10% |

| Pouches | 15% |

| Bags | 39% |

| Tubs & Trays | 5% |

| Bulk Packaging | 31% |

How Bags Segment Dominates the Largest U.S. Pet Food Market Revenue in 2025?

The bags segment dominated the U.S. pet food market in 2025. Pet food bags play an important role in keeping pet food healthy and safe. They are designed to protect food from light, moisture, and air. Good pet food bags keep the food nutritious and fresh for a longer period. Pet owners can make their pets stay healthy and happy by using the right kind of pet food bags. In addition, paper bags are more eco-friendly than plastic bags and are used for dry pet foods. Furthermore, various benefits of bags, such as preventing contamination, maintaining freshness, preventing nutrient degradation, and keeping food aromas inside, are further expected to accelerate the demand for pet food bags in the market in the U.S.

The Pouches Segment is Expected to Grow Fastest During the Forecast Period

The segment growth in the market is attributed to the various benefits such as extending shelf life, enhancing freshness, improving pet food quality and safety, usability and convenience for pet owners, increasing demand for resealable pet food packaging, brand differentiation, customization, and reducing the necessity of stock holding.

Godrej Consumer Products Limited (GCPL)

Nutrition Nxt

General Mills

By Pet Type

By Product Type

By Ingredient Type

By Distribution Channel

By Price Tier

By Packaging Type

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

U.S. Pet Food Market