April 2026

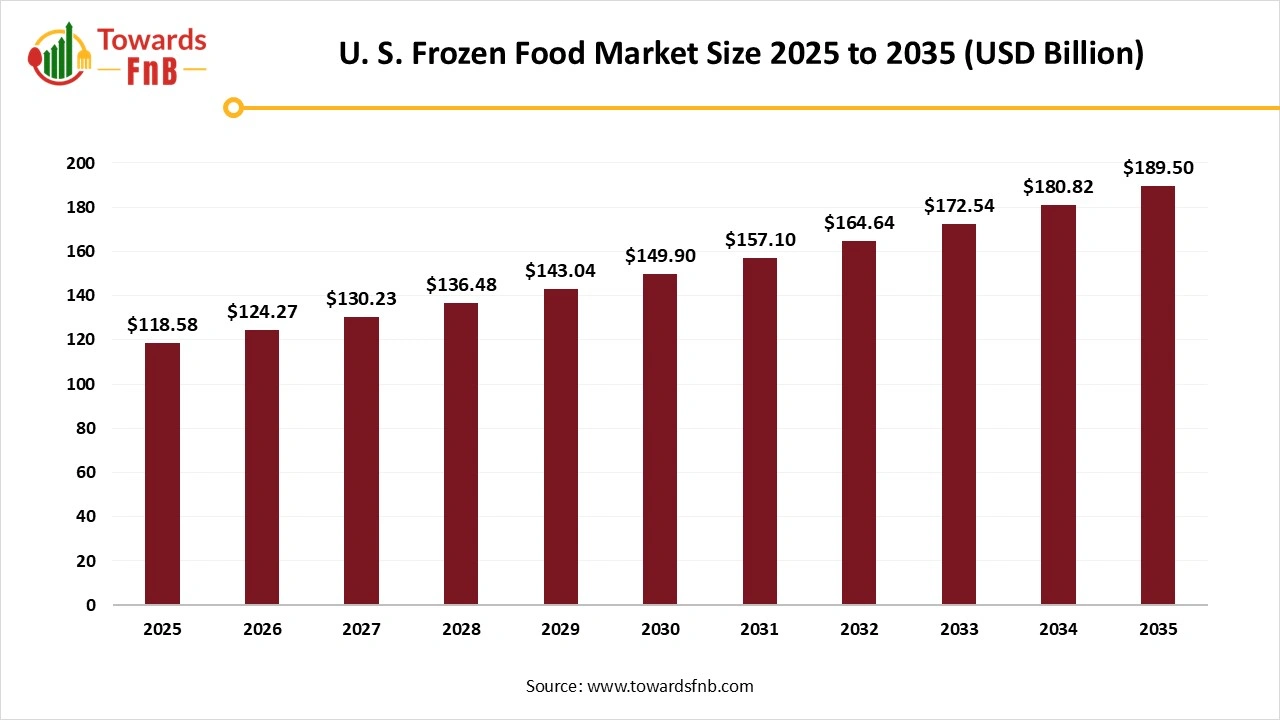

The U.S. frozen food market size stood at USD 118.58 billion in 2025 and is expected to grow steadily from USD 124.27 billion in 2026 to reach nearly USD 189.50 billion by 2035, with a CAGR of 5.57% during the forecast period from 2026 to 2035. Growing demand for convenience, ready-to-eat meals and advancement in freezing technology driving the market.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 5.57% |

| Market Size in 2026 | USD 124.27 Billion |

| Market Size in 2027 | USD 130.23 Billion |

| Market Size by 2035 | USD 189.50 Billion |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The increase in households with two incomes and more hectic lifestyles in the U.S. has driven the need for frozen meals. Frozen food items are appreciated for their extended shelf life, providing convenience and minimizing food waste, appealing to environmentally aware consumers. Enhanced freezing methods boost the quality, taste, and nutritional value of frozen products, making them more attractive.

Technological changes in the U.S. frozen food market are reshaping the production, distribution, and consumption of frozen foods through digital retail transformation and innovation. Improvements in smart freezing, cryogenic techniques, and flash-freezing processes enhance nutrient preservation, prolong shelf-life, and elevate product quality. These advancements are essential as customers seek frozen meals that taste fresher and are of higher quality. Temperature monitoring solutions connected via IoT and reusable, refrigerated containers improve cold chain management and decrease energy expenses. Businesses are employing advanced food science to merge plant proteins and various components to imitate the sensory experience of meat and dairy.

Raw Material Procurement

Processing of Frozen Food

Packaging of Frozen Food

Frozen Food Distribution

The interest in organic frozen foods has increased notably as shoppers seek healthier choices. These items frequently possess certifications, guaranteeing they comply with organic agricultural standards. Examples consist of frozen organic berries, vegetables, and meals that are ready to eat, which do not use synthetic pesticides and fertilizers. Plant-based diets are gaining popularity, as an increasing number of consumers choose vegetarian and vegan alternatives. This trend encompasses plant-derived meats such as frozen vegetables patties, meat-free crumbles, and plant-derived dairy substitutes like cashew-based frozen treats and almond milk ice creams.

Even with advancements in freezing technology, certain consumers continue to view frozen foods as less nutritious compared to fresh options. Worries about the inclusion of extra preservatives, synthetic additives, and high sodium levels in some frozen foods pose a challenge to market expansion. Enhancing the nutritional value and reducing the processing of frozen fruits and vegetables is essential to address this issue.

U.S. Frozen Food Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Ready Meals | 28% |

| Vegetables | 14% |

| Potatoes | 10% |

| Fruits & Vegetables | 15% |

| Meat | 12% |

| Fish/Seafood | 9% |

| Dairy Products | 7% |

| Bakery Products | 1% |

| Others | 4% |

Why did the Ready Meals Segment Dominate the U.S. Frozen Food Market in 2025?

The ready meals segment led the U.S. frozen food market in 2025. Market expansion is fueled by growing urbanization, heightened demand for convenience food, and changing consumer lifestyles that prioritize quick meal options. The need for convenient, ready-to-eat meals is consistently growing as they help working professionals save time and effort due to lifestyle changes. With the increasing demand for innovative packaged foods, GenZ and millennials are driving the launch of high-quality products.

The Fruits and Vegetables Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Consumers are more frequently focusing on health and wellness, prompting them to select frozen fruits and vegetables for their rich nutritional value, low-calorie features, and contribution to healthy eating. The growing popularity of vegetarian and vegan diets, along with a broader transition to plant-based eating, boosts the need for fruits and vegetables as essential food items. Busy lifestyles and the need for fast meal solutions fuel the need for convenient choices such as ready-to-cook, pre-seasoned, or prepared frozen vegetables.

U.S. Frozen Food Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Offline | 55% |

| Retail | 25% |

| Food Service | 15% |

| Online | 5% |

Which Distribution Channel Dominated the U.S. Frozen Food Market in 2025?

Offline segment held the dominating share of the U.S. frozen food market in 2025, due to its effective reach and the opportunity it offers consumers to physically examine the products prior to purchase. Many of these stores offer a diverse selection of frozen products from fruit and vegetables to prepared meals making them a convenient option for daily necessities. The vast array of supermarkets and grocery stores offers a strong distribution system that has historically met the demands of the frozen food sector. Shoppers appreciated being able to examine products in person, take advantage of in-store deals, and the overall convenience and known presence of brick-and-mortar stores for their frozen food shopping.

Online Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Owing to the rise in e-commerce popularity, a change in consumer habits favoring convenience, and rapid growth during the pandemic that pushed individuals toward digital solutions for their requirements. Additionally, online platforms provide a broader range of products and brands, featuring specialty dietary choices such as vegan or gluten-free, along with competitive pricing and delivery services straight to your doorstep, all accommodating fast-paced lifestyles and evolving tastes.

U.S. Frozen Food Market Share, By Freezing Technology, 2025 (%)

| Segments | Shares (%) |

| Blast Freezing | 46% |

| Individual Quick Freezing (IQF) | 38% |

| Belt Freezing | 16% |

How did the Individual Quick-Freezing Technology Dominate the U.S. Frozen Food Market in 2025?

The individual quick-freezing technology segment dominated the market with the largest share in 2025, as it effectively maintains the quality, texture, and nutritional value of food by freezing each item individually. This prevents clumping and results in a superior product that attracts consumers desiring convenience and freshness. This innovation also provides manufacturers with operational benefits, including minimized waste, longer shelf life, and suitability for mass production, while fostering the expansion of the convenient and health-focused frozen food industry.

The Blast Freezing Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Blast freezing rapidly preserves vitamins, minerals, and other nutrients, ensuring the product remains as nutritious as fresh food. It retains the natural moisture, flavor, and scent of the food by avoiding the formation of large ice crystals, which can harm cells during slow-freezing techniques. This technology effectively freezes substantial quantities of varied items, ranging from meat to seafood, providing a cost-efficient and productive option for food processing facilities, commercial kitchens, and extensive food services.

Nissin Foods

Nestlé

Conagra Brands, Inc

By Product Type

By Freezing Technology

By Distribution Channel

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

U.S. Frozen Food Market