April 2026

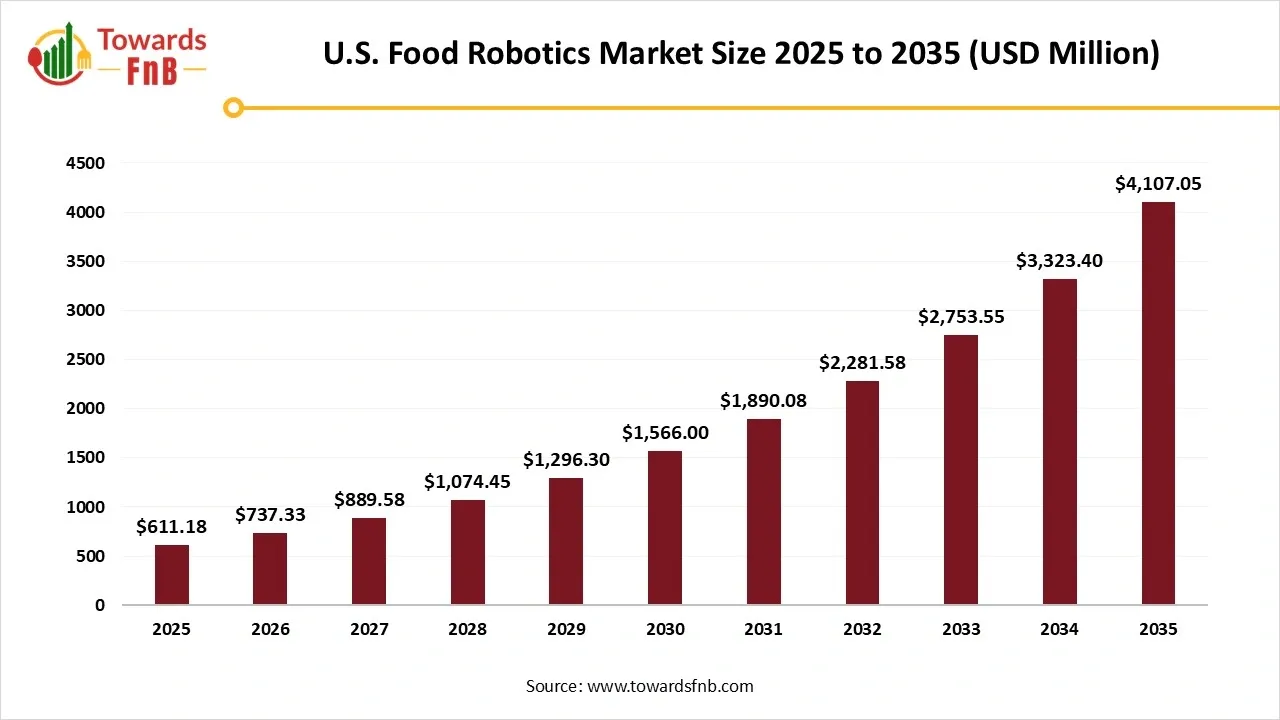

The U.S. food robotics market size reached at USD 611.18 million in 2025 with projections indicating a rise from USD 737.33 million in 2026 to reach approximately USD 4,107.05 million by 2035, expanding at a CAGR of 20.99% throughout the forecast period from 2026 to 2035. Growth of the market is driven by increasing labor shortages and a focus on hygiene in food processing.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 20.99% |

| Market Size in 2026 | USD 737.33 Million |

| Market Size in 2027 | USD 889.58 Million |

| Market Size by 2035 | USD 4,107.05 Million |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The U.S. food robotics market is experiencing significant growth, driven by rising automation adoption to counter labor shortages, enhance efficiency and safety, and meet high consumer demand for processed food. The market refers to the adoption of robotic systems and automation technologies within the food and beverage sector to enhance processing, packaging, handling, and quality assurance. These robotics solutions improve productivity, hygiene, precision, labor efficiency, and cost-effectiveness, while addressing workforce shortages and increasing demand for high-quality, consistent food products.

Incorporation of AI and machine learning, sophisticated grippers for fragile foods, and the rise of collaborative robots (co-bots) that collaborate with humans. These technological changes seek to tackle labor shortages, enhance efficiency and reliability, uphold elevated food safety standards, and facilitate increased product customization to satisfy consumer preferences for convenience. AI and ML enable robots to learn, helping them refine intricate tasks, adjust to product differences, and enhance their performance progressively.

Innovations such as AI/Machine Learning incorporation, the emergence of collaborative robots (cobots), and the growth of IoT along with Industry 4.0 technologies are generating considerable prospects in the US food robotics sector. Robotic systems ensure that food processing adheres to safety regulations, reducing the risk of contamination. They can uphold precision and tidiness that human workers cannot achieve. Improvements in AI, machine learning, and smart vision systems are boosting robot abilities, providing increased flexibility, improved product sorting, and adaptability to various industry requirements. Another significant development pertains to the creation of advanced end-of-arm tooling (EOATs) and grippers, specifically designed for managing fragile, sticky, or irregularly shaped food products without harm, including soft fruits and raw meats

Most food and beverage companies are reluctant to adopt automated processes because of the extra installation costs. Market growth is limited by the additional expense of incorporating standalone robots into a complete robotic system, which includes auxiliary equipment like safety barriers, sensors, programmable logic controllers (PLC), human-machine interface (HMI), and safety systems. Moreover, engineering costs encompass installation, programming, and commissioning activities. These higher costs restrict the expansion of the market.

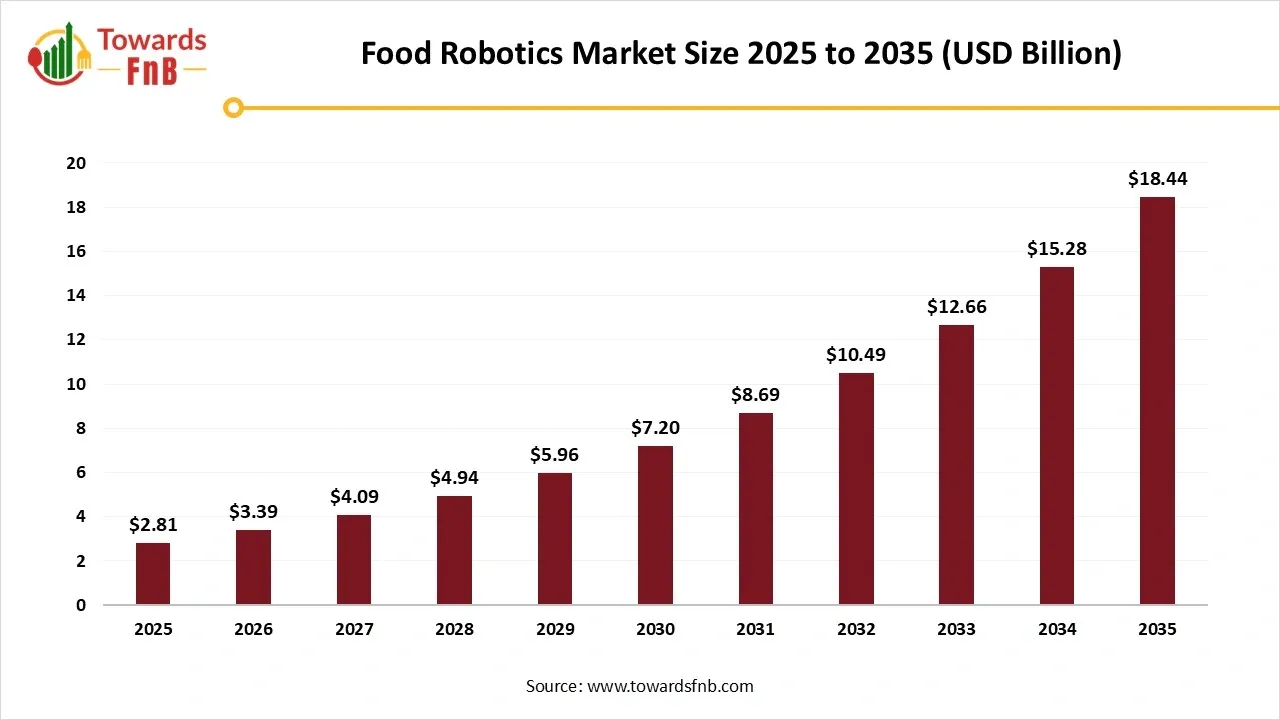

The global food robotics market is expected to grow significantly, starting from USD 2.81 billion in 2025 and rising to an estimated USD 18.44 billion by 2035. This growth, driven by the increasing adoption of automation, a greater emphasis on food safety, and advancements in artificial intelligence, is projected to occur at a compound annual growth rate (CAGR) of 20.7% from 2025 to 2034.

U.S. Food Robotics Market Share, By Robot Type, 2025 (%)

| Segments | Shares (%) |

| Articulated Robots | 45% |

| SCARA Robots | 15% |

| Delta & Parallel Robots | 12% |

| Collaborative Robots (Cobots) | 8% |

| Cartesian/Linear Robots | 13% |

| Others | 7% |

Why did the Articulated Robot Segment Dominate the U.S. Food Robotics Market in 2025?

Articulated robot segment led the U.S. food robotics market in 2025. The demand for precision, elevated efficiency, and the ability to perform complex tasks has led to an increasing reliance on articulated robots in manufacturing and assembly processes. Articulated robots are favored for their versatility and excel in tasks like palletizing, packaging, and picking. Additionally, the ongoing advancements in robotic technology have made articulated robots increasingly accessible and cost-effective for food producers of different sizes. The reduction in costs, along with increased payload capacity and extended range, ensures that articulated robots remain a preferred choice for many food processing companies.

Collaborative Robots (Cobots) Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Collaborative robots (cobots) are transforming the food industry by offering innovative solutions to labor shortages, production flexibility, and safety concerns. Cobots, a fast-growing segment of industrial robotics, are designed to work alongside humans, improving efficiency while maintaining safe and productive workflows. Collaborative robots are essential in smart factories, facilitating smooth cooperation between humans and robots by incorporating IoT, AI, and machine learning technologies.

Which Application Segment Dominated the U.S. Food Robotics Market in 2025?

Packaging & repackaging segment held the dominating share of the U.S. food robotics market in 2025. An increasing consumer preference for ready-to-cook and ready-to-eat meals fuels the necessity for extensive packaging of food items. Robotics aids in automating tasks to guarantee uniform quality and prolong the shelf life of packaged products. The US faces elevated labor expenses, prompting companies to invest in robotics for packaging and various tasks to lower operational costs. The large-scale manufacturing of processed, frozen, dried, and chilled packaged foods, especially in areas like dairy and baked items, requires and promotes the use of food robotics for reliable production.

Quality Inspection & Food Safety Testing Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

As it addresses critical industry issues concerning food safety, consistency, and traceability. Quality inspection robots can operate continuously, handle hazardous situations, and perform intricate assessments that are challenging for human employees. This automation enhances safety in the workplace while also ensuring consistent quality of output, which is essential in industries such as food and beverage. Improvements in sensor technology, artificial intelligence, and connectivity have greatly enhanced the capabilities and applications of quality inspection robots.

U.S. Food Robotics Market Share, By Payload Capacity, 2025 (%)

| Segments | Shares (%) |

| Low (Up to 10 kg) | 15% |

| Medium (10–100 kg) | 60% |

| High (Above 100 kg) | 25% |

Why did the Medium (10–100 Kg) Segment Dominate in the U.S. Food Robotics Market in 2025?

Medium (10–100 kg) segment dominated the market with the largest share in 2025. The 10–100 kg capacity range addresses a large segment of food production requirements, from medium-sized packaging to managing fresh produce. This adaptability enables producers to utilize identical robotic systems for multiple functions by merely swapping the end-of-arm tool. This payload class provides an effective mix of speed and power, rendering them suitable for high-throughput uses. For instance, they can manage palletizing tasks at high cycle speeds without compromising precision.

Low (up to 10 kg) Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Small payload robots usually need a lesser upfront cost compared to bigger industrial versions. This cost-effectiveness allows small and medium-sized food businesses, which were previously excluded from the robotics market to access automation. Light payload robots are constructed using food-safe materials that can be easily cleaned to comply with strict health and safety regulations. Their small dimensions facilitate seamless incorporation into current production systems without needing major facility renovations.

Which End Use Industry Segment Dominated the U.S. Food Robotics Market in 2025?

Meat, poultry & seafood segment held the largest share of the market in 2025. Handling meat, poultry, and seafood entails complex and repetitive tasks like deboning, slicing, trimming, and portioning, which are well-suited for automation. Robotics provides greater speed, precision, and accuracy in these intricate tasks. Robotics ensures the adherence to stringent hygiene standards crucial in meat, poultry & seafood processing. The increasing consumer demand for processed and packaged meat, poultry & seafood products further propel the necessity for automated solutions to enhance efficiency, guarantee food safety and hygiene, minimize waste, and offer supply chain transparency.

Ready-to-Eat & Packaged Foods Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Driven by rising consumer demand for convenience, elevated labor expenses, and the necessity for uniform quality in large-scale production. Robots are highly efficient in operations such as packaging, sorting, and pick-and-place activities, which are essential for fulfilling the increased demand for packaged products necessary to cater to the rising popularity of ready-to-eat and processed food items. Stringent food safety regulations further promote the use of robots to guarantee cleanliness and minimize contamination risks in processing and packaging.

U.S. Food Robotics Market Share, By Function, 2025 (%)

| Segments | Shares (%) |

| Processing Robots | 12% |

| Handling Robots | 50% |

| Packaging Robots | 8% |

| Inspection Robots | 17% |

| Others | 13% |

What Made the Handling Robots Segment Dominant in the U.S. Food Robotics Market in 2025?

Handling robots segment led the market in 2025, because of the demand for automation in pick-and-place operations such as packaging and palletizing, which call for speed, accuracy, and adaptability. Elements contributing to this dominance consist of elevated labor expenses, rigorous food safety standards, and heightened consumer appetite for packaged foods. Contemporary robots provide enhanced agility, rapidity, and accuracy in managing fragile food products, rendering them ideal for intricate food processing and assembly tasks.

Inspection Robots Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

The implementation of rigorous global and regional food safety standards requires improved inspection techniques that inspection robots can deliver. Incorporating AI, edge computing, and advanced vision sensors into inspection robots facilitates more accurate, autonomous inspections and detailed data analysis, driving market expansion. Food manufacturers in the U.S. continually pursue enhancements in their processes, with robotics providing reliable and high-quality inspection and quality assurance.

U.S. Food Robotics Market Share, By Deployment Mode, 2025 (%)

| Segments | Shares (%) |

| On-Premises Robotics Systems | 60% |

| Cloud-Integrated Robotics Platforms | 15% |

| Hybrid Systems | 25% |

Which Deployment Mode Segment Dominated the U.S. Food Robotics Market in 2025?

On-premises robotics systems segment held the dominating share of the market in 2025, due to the demand for enhanced control over production, strict data security, and adherence to food safety regulations. These systems enable manufacturers to oversee production processes directly and integrate effortlessly with current systems, guaranteeing constant uptime and immediate customization essential for food operations with high volume and strict compliance.

Cloud-Integrated Robotics Platforms Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

As they facilitate shared data, AI-driven decision-making, and adaptable, cost-effective solutions that meet industry demands for efficiency, customization, and ongoing advancement in food processing. Factors encompass the rising intricacy of food processing, the demand for adherence to food safety regulations, and the expanding acceptance of Robotics as a Service (RaaS) models, which lower initial expenses and enhance access to sophisticated automation.

DoorDash

Chef Robotics

Sodexo and ART

By Robot Type

By Application

By Payload Capacity

By End-Use Industry

By Function

By Deployment Mode

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

U.S. Food Robotics Market