April 2026

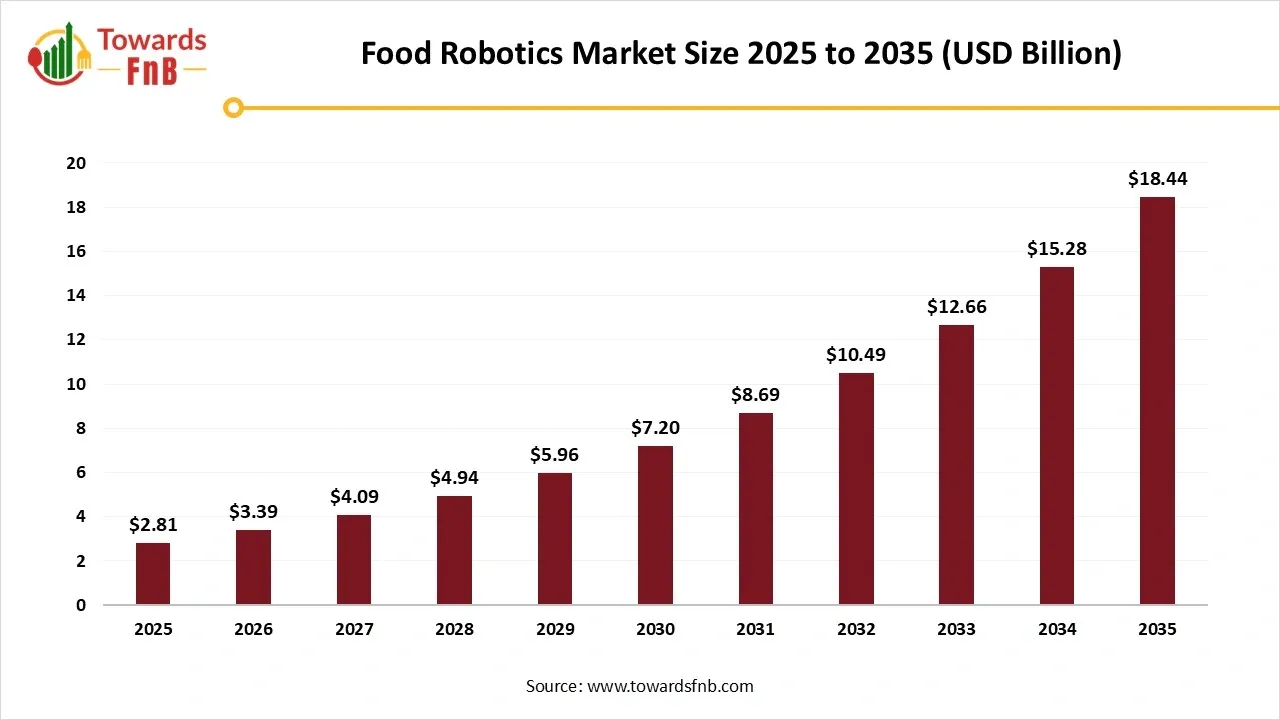

The global food robotics market size estimated at USD 2.81 billion in 2025 and is anticipated to increase from USD 3.39 billion in 2026 to an estimated USD 18.44 billion by 2035, witnessing a CAGR of 20.7% during the forecast period from 2026 to 2035. Market is driven by rising automation, demand for enhanced food safety, and advancements in AI.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 20.7% |

| Market Size in 2026 | USD 3.39 Billion |

| Market Size in 2027 | USD 4.09 Billion |

| Market Size by 2035 | USD 18.44 Billion |

| Largest Market | Europe |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Food robotics market is driven by factors such as labor shortages, increasing production costs, growing consumer demand for convenience and quality, and the need for enhanced food safety and hygiene. Food robotics is the application of automated robots and systems to perform a wide range of tasks in the food industry, from manufacturing and processing to packaging, delivery, and even cooking.

Improvements in artificial intelligence (AI), enhanced hardware, and the incorporation of intelligent systems. These advancements are pushing food robots from basic, repetitive roles to intricate, flexible, and cooperative tasks, fundamentally changing food production, packaging, and services. The incorporation of the Internet of Things (IoT) enables robots to link with various smart devices, sensors, and data analysis platforms. Advancements in 3D printing and materials science are opening avenues for creating edible robots and custom food production.

Investment By Companies in Food Robotics

| Company | Description | Latest funding round | Amount (USD) | Key investors |

| Chef Robotics | Develops AI-enabled robotic systems for automated meal assembly in the food service industry. | Series A (Equity and debt) | $43.1 million | Avataar Ventures, Construct Capital, Bloomberg Beta, Silicon Valley Bank |

| Miso Robotics | Provides autonomous robots, such as "Flippy" for assisting chefs with tasks like frying and grilling. | Series E | $137 thousand | Acacia, Avista Investments, Juvo Capital |

| Dexai Robotics | Manufactures a robotic arm that automates food assembly using utensils in commercial kitchens. | Series A | $6.7 million | Rho Capital Partners, Alumni Ventures, Hyperplane |

| Hyphen | Offers an automated kitchen operation platform to prepare meal bowls with the help of AI and sensors. | Series A | $34.4 million | Tiger Global Management, AgFunder, Compound |

| Botinkit | Provides AI-driven digital kitchen solutions with robots that automate cooking processes. | Series B | Undisclosed | 5Y Capital, Forebright Capital, The Hina Group |

The integration of AI, IoT, and collaborative robotics (cobots) offers significant opportunities for the food robotics market. These technologies allow smarter, adaptive systems capable of handling complicated processes such as quality inspection, sorting, and predictive maintenance. The rising adoption of Industry 4.0 practices enhances connectivity and real-time monitoring, further improving efficiency and reducing downtime.

The successful adoption of food robotics needs technical expertise for installation, programming, and maintenance. Various regions face a shortage of skilled professionals capable of handling advanced robotic systems, posing a hurdle for seamless integration. Additionally, technical complications such as system interoperability, software upgrades, and customization add to the operational hurdles.

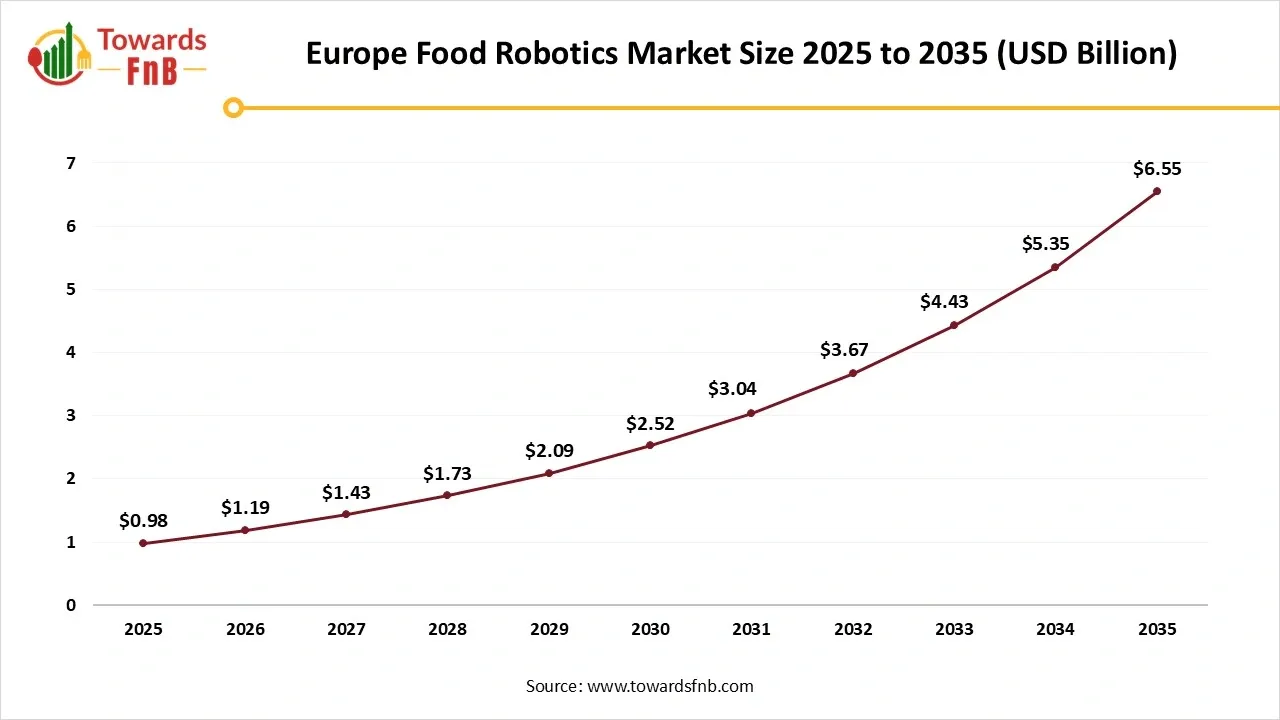

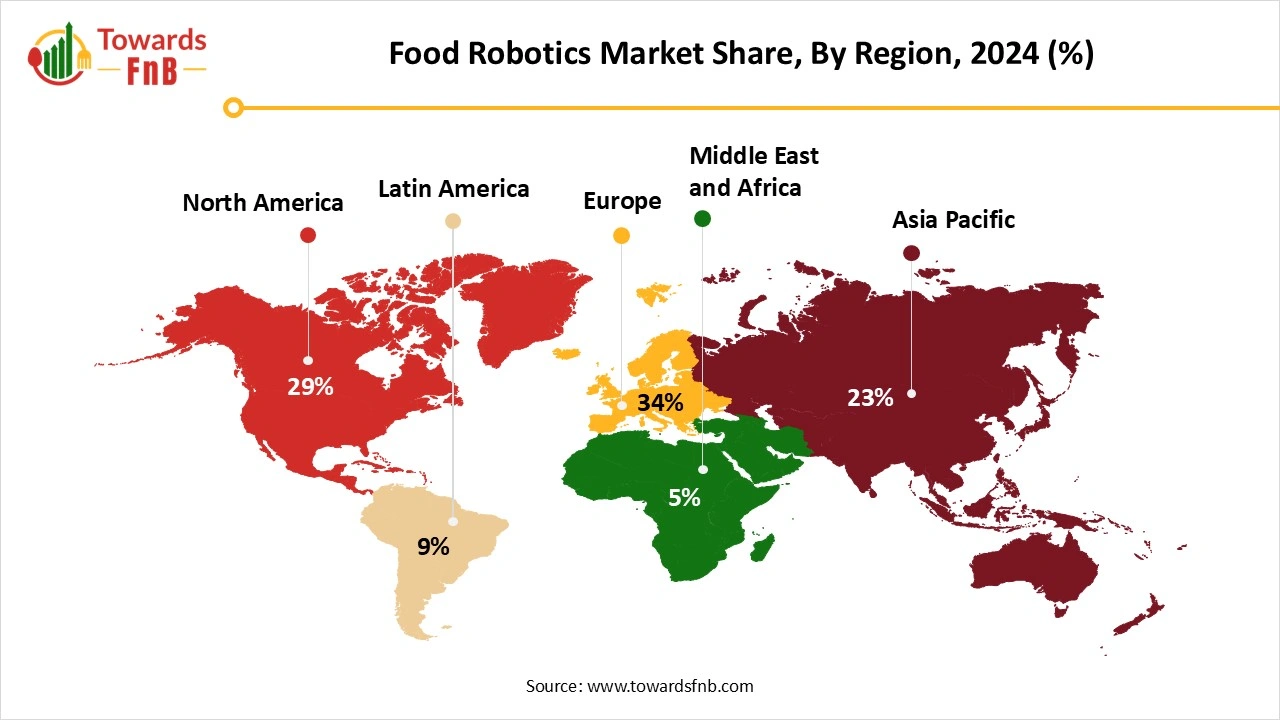

Europe Held the Largest Share of the Market in 2025

The food robotics market in Europe is witnessing substantial expansion, mainly propelled by the need for greater efficiency, better food safety, and lower labor expenses in the food processing and packaging sectors. Producers are progressively utilizing robotics to tackle issues like workforce shortages, the requirement for uniform product quality, and the growing need for varied, tailored food items. Moreover, the incorporation of cutting-edge technologies such as artificial intelligence, machine learning, and advanced vision systems is enhancing the functionalities of food robots, enabling them to perform more intricate and delicate tasks.

Europe Food Robotics Market Size 2025 to 2035

The Europe food robotics market size estimated at USD 0.98 billion in 2025 and is anticipated to increase from USD 1.19 billion in 2025 to an estimated USD 6.55 billion by 2034, witnessing a CAGR of 20.92% during the forecast period from 2026 to 2035.

United Kingdom Food Robotics Market Trends

The United Kingdom is undergoing considerable expansion driven by various important factors. Businesses are progressively embracing robotic technologies to improve production efficiency and lower labor expenses as automation optimizes food processing and packaging activities. Producers are incorporating AI and machine learning into robots, allowing them to execute intricate tasks like sorting, packaging, and quality control with great accuracy. With the increasing consumer demand for customized food items and quicker delivery, robotics is addressing these requirements by enhancing production speed and personalization.

Asia Pacific is Expected to Grow at the Fastest Rate in the Food Robotics Market During the Forecast Period

This can be linked to elements like increasing awareness about food safety, strict government regulations, and rising competition within the FMCG industry. A decrease in operational expenses and labor costs is expected to enhance the need for robotics within the food sector, which will, in turn, support the growth of the food robotics market in this area. The increasing disposable income of consumers in developing economies is boosting the demand for packaged and processed food, which consequently enhances the need for automation technologies to elevate food production capabilities. Elements like evolving lifestyles, increasing population, and the persistent craving for convenience food drive the expanding use of robotic systems in food processing facilities.

India Food Robotics Market

The growth of the food robotics market in India is fueled by the rising implementation of automation in food processing. Due to increasing labor expenses and the demand for uniform product quality, food manufacturers are adopting robotic technologies for sorting, packaging, and processing. The increasing popularity of ready-to-eat meals and packaged foods is further fueling the adoption of robotics in the sector. Collaborative robots, known as cobots, are becoming popular in India’s food robotics sector because they can effectively operate alongside humans. These robots are used for tasks like ingredient management, quality assurance, and secondary packaging. The need for clean and contamination-free food production is driving producers to adopt robotic systems that require little human involvement.

")

North America expects the significant growth during the forecast period. The food robotics market in North America is witnessing substantial expansion, mainly propelled by the need for greater efficiency, better food safety, and lower labor expenses in the food processing and packaging sectors. Producers are progressively utilizing robotics to tackle issues like workforce shortages, the requirement for uniform product quality, and the growing need for varied, tailored food items. Moreover, the incorporation of cutting-edge technologies such as artificial intelligence, machine learning, and advanced vision systems is enhancing the functionalities of food robots, enabling them to perform more intricate and delicate tasks.

United States Food Robotics Market

The United States is undergoing considerable expansion driven by various important factors. Businesses are progressively embracing robotic technologies to improve production efficiency and lower labor expenses as automation optimizes food processing and packaging activities. Producers are incorporating AI and machine learning into robots, allowing them to execute intricate tasks like sorting, packaging, and quality control with great accuracy. With the increasing consumer demand for customized food items and quicker delivery, robotics is addressing these requirements by enhancing production speed and personalization.

Food Robotics Market Share, By Robot Type, 2025 (%)

| Segments | Shares (%) |

| Articulated robots (multi-axis) | 38% |

| SCARA robots | 14% |

| Delta/parallel-kinematic robots | 15% |

| Cartesian/gantry robots | 10% |

| Autonomous mobile robots (AMRs)/AGVs | 12% |

| Collaborative robots (cobots) | 5% |

| Specialized food-grade manipulators (washdown/hygienic) | 6% |

Why did the Articulated Robot Segment Dominate the Food Robotics Market in 2025?

Articulated robot segment led the food robotics market in 2025. The need for accuracy, high efficiency, and the capability to execute intricate tasks has resulted in a growing dependence on articulated robots in production and assembly operations. Articulated robots are preferred for their adaptability and lead in areas such as palletizing, packaging, and picking. Furthermore, the continuous progress in robotic technology has rendered articulated robots more attainable and affordable for food producers of various scales. The decrease in expenses, combined with greater payload capability and longer reach, guarantees that articulated robots continue to be a favored option for numerous food processing enterprises.

Collaborative Robots (Cobots) Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Collaborative robots (cobots) are revolutionizing the food sector by providing inventive answers to workforce shortages, manufacturing adaptability, and safety issues. Cobots, the rapidly expanding category of industrial robotics, are engineered to collaborate with humans, enhancing efficiency while ensuring safe and effective workflows. Collaborative robots play a crucial role in smart factories, enabling seamless interaction between humans and robots through the integration of IoT, AI, and machine learning technologies.

How did the Packaging Segment Dominate the Food Robotics Market in 2025?

Packaging segment held the dominating share of the food robotics market in 2025, due to increased consumer demand for Fs, a higher need for automation for efficiency and consistency, labor shortages, and the importance of strict hygiene and safety standards for packaged items. Packaging robots enhance speed, precision, and cleanliness, while also guaranteeing adherence to food safety standards, making them essential for large-scale food manufacturing.

Inspection & Quality Control Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

As it directly tackles essential industry concerns related to food safety, consistency, and traceability. Quality inspection robots can work tirelessly, manage dangerous conditions, and conduct complex evaluations that are difficult for human workers. This automation improves workplace safety while also guaranteeing uniform output quality, which is vital in sectors like food and beverage. Advancements in sensor technology, artificial intelligence, and connectivity have significantly contributed to the growth of capabilities and uses for quality inspection robots.

Food Robotics Market Share, By Technology/Capability, 2025 (%)

| Segments | Shares (%) |

| Machine vision & optical sorting | 28% |

| Artificial intelligence/ML/predictive analytics | 12% |

| Force/torque sensing & tactile feedback | 15% |

| Advanced end-effectors (vacuum, soft grippers, hygienic grippers) | 9% |

| Motion control & path planning (vision-guided) | 5% |

| Sterilizable/IP-rated hardware designs | 8% |

| Food-safe material coatings & cleanability features | 7% |

Which Technology/Capability Segment Dominated the Food Robotics Market in 2025?

Machine vision & optical sorting segment dominated the market with the largest share in 2025. More stringent global government food safety regulations, like the Food Safety Modernization Act (FSMA) in the U.S., require manufacturers to implement enhanced sorting technology. In addition to conventional cameras, systems now employ advanced sensors like short-wave infrared (SWIR) and hyperspectral imaging to identify a broader spectrum of contaminants and defects according to their chemical composition. Machine vision systems effortlessly blend with other robotic operations, like robotic arms for selecting and positioning items, to form a completely automated and smart production line.

AI/ML & Predictive Analytics Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

The incorporation of artificial intelligence within the food sector has led to notable improvements in efficiency, safety, and sustainability. These technologies allow for immediate tracking and validation, thus improving transparency and confidence throughout the supply chain. Additionally, AI-based predictive analytics are employed to anticipate demand and decrease waste, enhancing inventory management and lessening the ecological footprint of food production and distribution.

Food Robotics Market Share, By Component, 2025 (%)

| Segments | Shares (%) |

| Hardware (robots, end-effectors, AMRs, conveyors) | 45% |

| Software (control software, vision analytics, fleet management) | 20% |

| Systems integration & controls (PLC/SCADA integration) | 18% |

| Services (installation, commissioning, maintenance, spare parts) | 17% |

What Made the Hardware Segment Dominant in the Food Robotics Market in 2025?

Hardware segment held the largest share of the market in 2025. Hardware encompasses a range of devices throughout the food value chain, including voice assistants, cooking robots, and self-ordering kiosks in restaurants, as well as robots and drones for deliveries. Additionally, IoT sensors can reduce waste by tracking temperature. The demand to achieve regulatory compliance, enhance customer experience, and boost efficiency throughout the supply chain is propelling segment expansion. Intricate manufacturing procedures and substantial upfront costs for these unique, durable parts reinforce the hardware segment's market presence in the food sector.

Software Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Software is crucial for robots to perform complicated tasks such as detailed processing, accurate packaging, and high-precision material handling, which are challenging to automate solely with hardware. Cloud-based software improves immediate data exchange, facilitating remote oversight, anticipatory upkeep, and increased connectivity throughout the food supply network. Robotics powered by software assists food producers in satisfying the need for processed foods, packaged items, and ready-to-eat meals.

Which End Use Industry Segment Held the Largest Share of the Food Robotics Market in 2025?

Meat & poultry segment led the market in 2025, where precision and efficiency are crucial. Robotics in this field not only improve task speed and precision but also tackle labor-intensive issues, guaranteeing consistent product quality. Automated systems are adept at managing intricate tasks like deboning, trimming, and portioning, thus enhancing production processes. Upholding food safety and hygiene standards in poultry production is essential to avoid contamination and guarantee quality. The blend of intelligent technology and robotics enhances traceability and transparency in the meat supply chain, boosting consumer trust.

Ready Meals/Frozen Foods Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Contemporary ways of living, marked by hectic routines and active workforces, are driving a significant need for fast and convenient meal options. Robotics improve productivity in the manufacturing of frozen food by automating routine tasks, minimizing human mistakes, and maintaining quality and uniformity. There is a necessity for robotic automation to guarantee reliable quality and efficiency in the bulk production of packaged foods to satisfy this requirement. Automation reduces operational expenses in food production, making it more viable to manufacture frozen meals in large quantities.

DoorDash

ABB Robotics

By Robot Type

By Function/Application

By Technology/Capability

By Component

By End-Use Industry

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Food Robotics Market