U.S. Barley Flakes Market Size 2025 to 2035

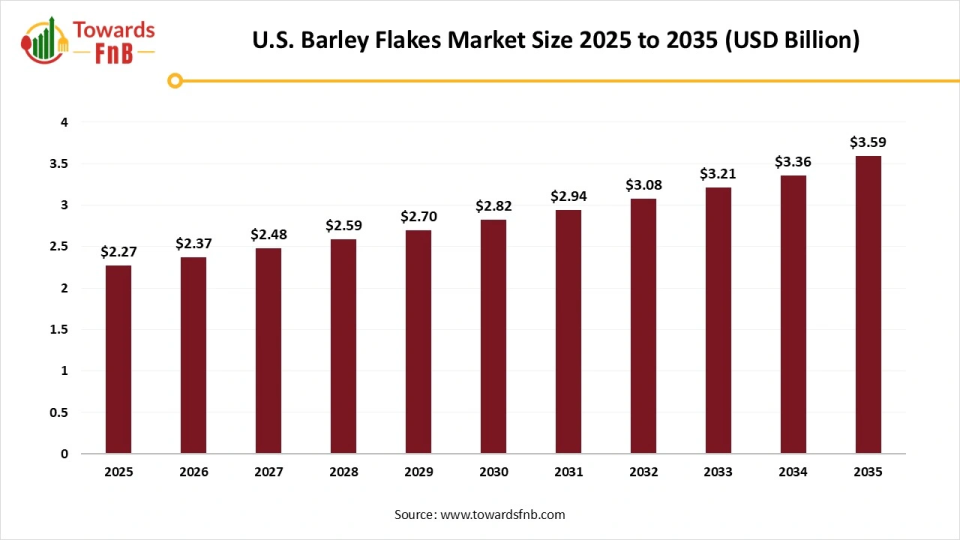

The U.S. barley flakes market size was valued at USD 2.27 billion in 2025 and is expected to grow steadily from USD 2.37 billion in 2026 to reach nearly USD 3.59 billion by 2035, with a CAGR of 4.69% during the forecast period from 2026 to 2035. The market is primarily driven by increasing health awareness, the increasing popularity of plant-based and on-the-go food products, and the convenience sought by busier lifestyles, including the rising number of working women.

Key Highlights

- By product type, the regular/rolled barley flakes segment held the major market share in 2025.

- By product type, the instant & fortified/functional flakes segment is expected to grow at the fastest rate during the forecast period.

- By source/ variety, the pearl/hulled varieties segment contributed the biggest market share in 2025.

- By source/ variety, the High-β-glucan/functional varieties segment is expected to grow at the fastest rate during the forecast period.

- By form/processing, the whole/rolled flakes segment dominated the U.S. barley flakes market in 2025.

- By form/processing, the quick/instant flakes segment is expected to grow at the fastest rate during the forecast period.

- By application, the breakfast cereals & porridge segment held the major market share in 2025.

- By application, the beverage premixes & functional foods segment is expected to grow at the fastest rate during the forecast period.

- By distribution channel, the hypermarkets/supermarkets segment held the major market share in 2025.

- By distribution channel, the online/e-commerce segment is expected to grow at the fastest rate during the forecast period.

U.S. Barley Flakes Industry Coverage

| Study Coverage |

Details |

| Growth Rate from 2026 to 2035 |

CAGR of 4.69% |

| Market Size in 2026 |

USD 2.37 Billion |

| Market Size in 2027 |

USD 2.48 Billion |

| Market Size by 2035 |

USD 3.59 Billion |

| Base Year |

2025 |

| Forecast Period |

2026 to 2035 |

What is The U.S. Barley Flakes Market?

Barley flakes are whole-grain cereal produced by steaming, rolling, and flattening barley kernels into flakes used in breakfast cereals, bakery, snacks, beverage premixes, and food-ingredient applications. The U.S. barley flakes market covers production, processing (instant vs regular), organic and conventional offerings, private-label and branded SKUs, and distribution across retail, food service and industrial channels. Demand is driven by health trends (high fiber, β-glucan), plant-based diets, and product innovation in ready-to-eat and functional food.

U.S. Barley Flakes Market Trends

- Industry Growth Overview: Barley flakes are experiencing growth across various sectors, with the growing consumer awareness of the health benefits of whole grains, particularly the high beta-glucan content in barley flakes, demand for convenience food, and rising popularity of vegan and plant-based diets, which is boosting the demand for barley flakes as a versatile, nutritious, and plant-derived ingredient.

- Sustainability Trends: Consumers are implementing efficient irrigation techniques to conserve water, which is a significant factor as barley requires less water to cultivate compared to some other grains. Reduced GHG emissions, a significant push towards sustainable packaging solutions to reduce waste, and barley-based bioplastics, to replace conventional plastics. Supply chain transparency, efficiency, and plant-based alignment.

- Startup Ecosystem: The barley flakes startup ecosystem is developing unique products featuring barley flakes, such as granola mixes, fortified cereals, and functional ingredients, to appeal to health-conscious consumers. Alternative protein source explored as a sustainable, plant-based protein source by a start-up innovating in the food tech space, value-added products. Utilizing technology to improve agricultural practices, enhance processing methods, and create a more efficient and transparent supply chain.

Key Technological Shift in the U.S. Barley Flakes Market

- The U.S. barley flakes market is undergoing significant technological shifts focused on efficiency, nutrition enhancement, and sustainability. Processing innovations like infrared micronization and advanced drying methods improve product quality, shelf life, and digestibility while reducing cooking times.

- The adoption of precision agriculture, AI-driven automation, and biotechnology in farming ensures a consistent, high-quality supply of raw materials and the development of nutritionally superior barley varieties. The integration of blockchain technology is facilitating greater supply chain transparency and traceability.

U.S. Barley Flakes Market of Supply Chain Analysis

Input Provision

- This initial stage involves the supply of essential agricultural inputs like high-quality seeds, fertilizers, pesticides, and machinery to farmers.

Production/Farming

- This stage is where barley grain is cultivated by smallholder farmers and large commercial farms, who perform all farming operations from land preparation to harvesting and initial post-harvest handling.

Processing

- The harvested barley is then transported to processing facilities where it is cleaned, steamed, rolled into flakes, dried, and packaged.

Distribution and Marketing

- In this stage, the finished barley flakes are distributed through various channels to reach the end consumer.

Consumption

- The final stage is the consumption of the barley flakes by the end-user in various applications such as breakfast cereals, snack bars, or baked goods.

U.S. Barley Flakes Country Insights

U.S. Barley Flakes Market Analysis

The U.S. barley flakes market is being driven by increasing consumer health awareness and a strong demand for convenient, plant-based food that fit busy lifestyles. Trends favor minimally processed, whole-grain options and rapid e-commerce expansion, despite competition from substitute grains. While Europe currently holds the largest share, the U.S. market is growing significantly due to these evolving consumer preferences and innovative product offerings.

U.S. Barley Flakes Market Segmental Insights

Product Type Insights

U.S. Barley Flakes Market Share, By Product Type, 2025 (%)

| Segments |

Shares (%) |

| Instant Barley Flakes |

10% |

| Regular/Rolled Barley Flakes |

55% |

| Dehulled/Hulled Barley Flakes |

12% |

| Pearled Barley Flakes |

8% |

| Flavored/Fortified Barley Flakes |

15% |

- Instant Barley Flakes: Does not dominate with 10%, as instant barley flakes are less common compared to regular or rolled varieties, typically used for convenience but not as widely adopted.

- Regular/Rolled Barley Flakes: Dominates with 55% due to their widespread use in breakfast foods, snacks, and as an ingredient in a variety of recipes.

- Dehulled/Hulled Barley Flakes: Does not dominate with 12%, though dehulled barley flakes are important for specific health-focused products.

- Pearled Barley Flakes: Does not dominate with 8%, though it is used for specific culinary purposes, such as in soups and stews.

- Flavored/Fortified Barley Flakes: Gaining momentum with 15% due to increasing consumer demand for flavored and fortified grains that offer both taste and added health benefits.

Why did Regular/Rolled Barley Flakes Segment Dominate the U.S. Barley Flakes Market?

The regular/rolled barley flakes segment led the U.S. barley flakes market in 2025, due to consumer demand for minimally processed, healthy, and versatile food options. Their perception as a wholesome, clean label product aligns with current health trends, making them a preferred choice over highly processed alternative. Established production methods ensure affordability and widespread availability, further solidifying their market lead. Consumers appreciate their versatility in traditional and modern culinary applications, from porridges to baked goods.

The instant & fortified/functional flakes segment is observed to grow at the fastest rate during the forecast period

The converging trends in consumer behaviour, the need for speed, and the desire for enhanced nutrition. The convenience of instant preparation directly caters to the fast-paced modern lifestyle. Moreover, fortification and functional enhancement appeal to heart health. Advancements in technology processing have made these value-added products possible and appealing. The instant barley flakes segment is also experiencing notable growth due to the merging demand for modern convenience with a desire for healthy nutrition. Technological advancements have made it possible to offer quick-cooking options that retain the full nutritional benefits of whole grains, such as high beta-glucose content. This convenience factor appeals directly to busy professionals and families seeking quick breakfast solutions for on-the-go lifestyles. Furthermore, product innovation and wider distribution through e-commerce channels are expanding market reach.

Source/Variety Insights

U.S. Barley Flakes Market Share, By Source/Variety, 2025 (%)

| Segments |

Shares (%) |

| Hulled Barley |

40% |

| Pearl Barley |

45% |

| Hull-Less Barley |

10% |

| High-β-Glucan Varieties |

5% |

- Hulled Barley: Does not dominate with 40%, as pearl barley is more commonly used due to its smoother texture and quicker cooking time.

- Pearl Barley: Dominates with 45% due to its ease of use, texture, and faster cooking time, making it the preferred choice in the food industry.

- Hull-Less Barley: Does not dominate with 10%, as hull-less barley is a more niche product with specific health benefits but less market penetration.

- High-β-Glucan Varieties: Gaining momentum with 5% as health-conscious consumers seek out barley varieties with higher levels of β-glucan for their heart-health benefits.

Why did the Pearl/Hulled Varieties Segment Dominate the U.S. Barley Flakes Market?

The Pearl/Hulled Varieties segment held the dominating share of the market in 2025. Due to its combination of high availability, affordability, and practical convenience. The pearling process results in a faster cooking time and a milder, softer texture that appeals to a wider consumer base compared to the tougher, longer-cooking whole-grain varieties. While slightly less nutritious than hulled barley, it is still perceived as a sufficiently healthy grain, offering an accessible balance of health benefits and ease of use that aligns well with modern, time-constrained lifestyles.

The High-β-glucan/functional varieties segment is the fastest-growing during the predicted timeframe

Because of a powerful combination of consumer health awareness and scientific validation. Consumers validation. Consumers are increasingly seeking preventative health solutions, with the proven cholesterol-lowering and blood-sugar-regulating properties of beta-glucan appealing to a health-conscious demographic.

Type Form/Processing

U.S. Barley Flakes Market Share, By Type Form/Processing, 2025 (%)

| Segments |

Shares (%) |

| Whole Flakes (rolled) |

60% |

| Quick/Instant Flakes (pre-cooked) |

15% |

| Pre-blended / Mixes (Oat/Barley blends) |

25% |

- Whole Flakes (rolled): Dominates with 60% due to their widespread use in cereals, granola, and baking, offering both texture and nutrition.

- Quick/Instant Flakes (pre-cooked): Gaining momentum with 15% due to the demand for convenient, easy-to-prepare breakfast options and snack foods.

- Pre-blended/Mixes (Oat/Barley blends): Does not dominate with 25%, though these blends are popular in health-focused products for added fiber and nutritional benefits.

How did the Whole/Rolled Flakes Segment Dominate the U.S. Barley Flakes Market?

The Whole/Rolled Flakes segment dominated the market with the largest share in 2025, due to consumers being increasingly aware of significant health benefits associated with whole grains, such as high fibre content, essential vitamins, and minerals. The demand for natural, organic, and clean-label products, versatility in home cooking, and their structure and high fibre content, whole/rolled flakes promote a feeling of fullness for longer, which appeals to consumers focused on weight management and healthy eating habits.

The quick/instant flakes segment is expected to grow at the fastest rate in the market during the forecast period

The powerful convergence of the demand for convenience and the pursuit of healthy eating habits in a busy modern lifestyle. Technological advancements ensure these quick-to-prepare products retain essential nutritional value and desirable texture. The needs of time-constrained consumers are seeking both speed and health benefits. The expansion of e-commerce and innovative product diversification further accelerates this growth trajectory.

The pre-blended/mixes segment is expanding significantly during the forecast period. It is offering consumers enhanced convenience and superior nutrition in a single package. These products save time and cater to the busy, on-the-go modern lifestyle. The ability to combine the benefits of barley with other functional ingredients like nuts, seeds, and fruits creates a high-value, nutrient-dense option for health-conscious consumers.

Application Insights

Which Application Segment Dominated the U.S. Barley Flakes Market?

The breakfast cereals & porridge segment held the largest share of the market in 2025. The leveraging of established consumer habits, strong distribution channels, and the alignment of barley's health benefits with modern wellness trends. The high nutritional value, specifically beta-glucan fiber content, and ease of preparation meet the demand for healthy and convenient breakfast options.

The beverage premixes & functional foods segment is seen to expand at the fastest rate during the forecast period

The perfect alignment of convenience and health-consciousness trends. Consumers are increasingly seeking on-the-go, easy-to-prepare products that offer specific, scientifically backed health benefits like cholesterol management. The segment effectively leverages barley's functional properties (high beta-glucan) while catering to the rise of plant-based diets and innovative, value-added food products.

The bakery & confectionery ingredients segment serves as a key growth catalyst in the market, by meeting consumer demand for healthier, value-added products. Barley flakes enhance the nutritional profile of baked goods (e.g., adding fiber and protein) and fit seamlessly into the growing "clean-label" and plant-based food trends. Their versatility in adding texture and flavor supports product innovation, leading to a wider variety of convenient, on-the-go snacks and specialty items.

Distribution Channel Insights

Which Hypermarkets/Supermarkets Segment Dominated The U.S. Barley Flakes Market?

The hypermarkets/supermarkets segment held the largest share of the market in 2025. The extensive reach, broad product assortments, and competitive pricing. They offer a convenient, one-stop shopping experience where consumers can physically inspect products and benefit from promotional deals. This combination of accessibility, variety, and convenience solidifies their dominant position as the primary channel for consumer purchases of barley flakes.

The online/e-commerce segment is seen to expand at the fastest rate during the forecast period

The unparalleled convenience, price transparency, and broad product selection it offers. By leveraging increasing internet penetration and consumer demand for quick and easy shopping experiences, online channels are capturing market share from traditional retailers. This shift underscores a fundamental change in how consumers prefer to shop for groceries, with digital platforms playing an increasingly vital role in the market's expansion.

Recent Developments in the U.S. Barley Flakes Market

- Development: In May 2025, scientists at Pant University developed a new, high-yielding barley variety with better disease resistance and protein content, improving raw material quality and supply (Source: The Times of India)

New specialty malts

- Launch: In April 2024, Briess introduced new specialty malts, including Crystal Red™ and Heritage Gold™, expanding their product line to serve both craft brewing and distilling industries. (Source: Briess Malt and Ingredients)

Top Companies In The U.S. Barley Flakes Market

PepsiCo/The Quaker Oats Company.

Corporate Information

- As a subsidiary of PepsiCo, The Quaker Oats Company contributes to the U.S. barley flakes market by leveraging its immense brand recognition and extensive distribution network to reach a vast consumer base. Through product diversification and innovation, Quaker introduces barley flakes in both traditional and modern formats, such as breakfast cereals and snack bars, aligning with consumer demand for convenient and healthy whole-grain options.

- Headquarters: Purchase, New York, in the United States.

- Foundation / Origin: Founded in 1965 in New Bern, North Carolina.

History and Background

- PepsiCo, Inc. was formed in 1965 through the merger of the Pepsi-Cola Company and Frito-Lay, Inc., combining beverage and snack food operations.

- Today, it is a food and beverage giant that has diversified its portfolio with numerous brands acquired over the decades, including Quaker Oats and Gatorade.

Key Developments and Strategic Initiatives

- This holistic sustainability agenda places health and sustainability at the core of the company's business model. It involves initiatives to achieve net-zero greenhouse gas emissions by 2040, use more sustainable packaging (including recyclable and paper-based materials), and evolve their product portfolio towards healthier options like grains and reduced sugar drinks.

- PepsiCo continues to expand its portfolio through strategic acquisitions, such as SodaStream and Rockstar Energy, to adapt to changing consumer preferences in health-conscious and energy drink markets. They also continuously innovate within existing brands, such as Quaker, to offer new products tailored to convenience, health, and specific regional tastes.

Mergers & Acquisitions

- In May 2025, PepsiCo completed the acquisition of the fast-growing prebiotic soda brand Poppi for $1.95 billion, aligning with the trend of functional beverages and gut health products.

- In July 2029, PepsiCo acquired Pioneer Foods, a major food and beverage company in South Africa, for approximately $1.7 billion, as a key part of its growth strategy for the African continent.

Partnerships & Collaborations

- In May 2025, PepsiCo and AWS collaborate to accelerate digital transformation, leveraging AWS for cloud migration, generative AI platforms (PepGenX), and real-time data insights for marketing and supply chain optimization.

- In July 2025, PepsiCo and Cargill are collaborating to empower farmers and advance sustainable agriculture. The initiative aims to expand regenerative agriculture practices across 240,000 acres of Iowa farmland by 2030, with PFI leading local implementation and farmer support.

Product Launches / Innovations

- In July 2025, PepsiCo launched a "first-ever" Prebiotic Cola, a significant innovation in the traditional cola category in 20 years. It contains three grams of prebiotic fiber, 5 grams of sugar, and no artificial sweeteners, targeting the functional beverage trend.

- In November 2025, PepsiCo introduced its Australian gourmet chip brand Red Rock Deli to the Indian market. The products are manufactured locally using three advanced technologies (Kettle Cooked, Baked, and Popped) and feature inspired flavors to cater to the premium snacking segment.

Key Technology Focus Areas

- PepsiCo heavily invests in AI, big data, and analytics to understand consumer preferences in real-time, optimize product development cycles, and inform business decisions across all functions. This includes using generative AI to analyze social media trends, predict demand, and even co-create new flavors like the Y3000 Zero Sugar variant.

- The company leverages cloud platforms, primarily Microsoft Azure and Amazon Web Services (AWS), as the foundational infrastructure for its digital transformation. This focus allows for scalable data unification and enables the deployment of sophisticated AI models across its operations.

R&D Organisation & Investment

- The company is actively researching and incorporating functional ingredients, like beta-glucans in barley flakes and new protein sources (e.g., from chickpeas and peas), into its food and beverage portfolio.

- PepsiCo invested $216 million in partnerships to support regenerative agriculture, focusing on improving soil health, water quality, and biodiversity.

SWOT Analysis

Strengths

- Extensive portfolio of over 23 billion-dollar brands (Lay's, Doritos, Quaker Oats, Gatorade, Pepsi) provides stability and broad market reach across snacks, beverages, and cereals.

- A robust and efficient worldwide supply chain ensures wide product availability in retail, e-commerce, and food service channels.

Weaknesses/Challenges

- A significant portion of revenue is still tied to CSDs, a category facing declining consumption trends and health scrutiny in key markets.

- Operates in highly competitive markets against rivals like Coca-Cola and Nestlé, which pressure pricing and demand constant investment in marketing and R&D.

Opportunities

- A major shift towards healthier, functional, and plant-based food options provides significant growth potential for PepsiCo's evolving product lines (e.g., functional beverages and healthier snacks).

- The rapid growth of online retail and grocery delivery offers opportunities to optimize digital marketing, leverage data analytics, and reach consumers more efficiently through platforms like AWS and Microsoft Azure.

Threats/Risks

- Governments are implementing "sugar taxes" and stricter labeling laws on high-sugar/fat products, posing financial threats and impacting brand perception.

- Supply chains are vulnerable to geopolitical conflicts, climate change impacts on agriculture (droughts, floods), and economic volatility, which can disrupt sourcing and cause price fluctuations.

Recent News & Strategic Updates

- Launched (July 22, 2025): PepsiCo launched a "first-ever" Prebiotic Cola, containing prebiotic fiber and reduced sugar, aligning with wellness trends.

- Partnership (December 2, 2025): PepsiCo announced a landmark partnership with the Mercedes-AMG Petronas F1 Team for the 2026 season. This collaboration will feature the Gatorade, Sting, and Doritos brands to engage the rapidly expanding F1 fanbase.

Other Key Players in the Market

- WK Kellogg Co: As a breakfast cereal leader, WK Kellogg Co incorporates barley flakes into various cereal and snack bar products to provide healthy, whole-grain options to a massive consumer base.

- Nestlé S.A. (selected brands): Nestlé leverages its R&D capabilities and brand trust to develop fortified and functional breakfast cereals that include barley flakes, targeting health-conscious consumers worldwide.

- King Arthur Baking Company (King Arthur Flour): King Arthur Baking Company contributes to the market by offering high-quality barley flour and flakes for home bakers and professional chefs, focusing on specialty baking applications.

- Bob’s Red Mill Natural Foods: Bob's Red Mill is a key player known for its range of whole-grain, minimally processed, and often organic barley flakes, catering to a niche of health-conscious and clean-label consumers.

- Honeyville, Inc. (Honeyville Grain): Honeyville primarily contributes to the ingredient and bulk market, supplying a consistent volume of high-quality barley flakes to other food manufacturers and institutional buyers. They ensure a steady supply of processed barley for use in a wide variety of secondary manufactured food products across North America.

- Briess Malt & Ingredients Co.: Briess serves as a critical supplier of specialty grain ingredients, providing high-quality malted barley products that can be used in both food applications and the brewing industry. Their focus on ingredient innovation directly supports other manufacturers in creating unique and high-quality functional food products.

- Rude Health: This UK-based health food company contributes to the European market with premium, "clean-label" breakfast cereals and porridges that feature barley flakes. Their marketing emphasis on natural ingredients and minimal processing appeals strongly to the health-conscious European consumer base.

- Nature’s Path Foods: As a major organic cereal brand, Nature’s Path incorporates organic barley flakes into its various granolas and hot cereals, meeting strong consumer demand for certified organic and sustainable products. They help drive the market in the organic segment across North America and beyond, leveraging sustainability as a key selling point.

- Shiloh Farms: Shiloh Farms provides a range of natural and organic barley products, including flakes, focusing on consumers who prioritize traditional, wholesome, and minimally processed ingredients. They serve a niche market focused on authentic and less refined food sources.

- Vitasana Foods / Vitasana: As a regional or specialty supplier, Vitasana contributes by catering to specific regional tastes or dietary requirements, offering localized accessibility to barley flake products. They help address regional demands where larger players may have less focused distribution.

- Urban Platter: Operating as a consumer brand and retail platform, Urban Platter helps expand the reach and awareness of barley flakes in markets like India by offering curated, healthy food options.

- Grain Millers, Inc.: Grain Millers is a major ingredient supplier and miller that provides high-quality barley flakes to the food manufacturing industry on a large scale, facilitating the production of many other branded consumer goods.

- Post Holdings / Attune Foods: Through brands under the Attune Foods umbrella, Post Holdings incorporates barley flakes into various healthy, sometimes organic, cereal options that compete with other major cereal brands. They utilize their large retail presence to ensure availability and visibility of barley-based products.

- Bob’s Red Mill Competitor / regional millers (e.g., Helsinki Mylly Oy): Regional millers like Helsinki Mylly Oy serve specific geographic markets with locally sourced and produced barley flakes, leveraging regional trust and shorter supply chains.

Segments Covered in the Report

By Product Type

- Instant Barley Flakes

- Regular / Rolled Barley Flakes

- Dehulled / Hulled Barley Flakes

- Pearled Barley Flakes

- Flavored / Fortified Barley Flakes

By Source/Variety

- Hulled Barley

- Pearl Barley

- Hull-Less Barley

- High-β-Glucan Varieties

By Form/Processing

- Whole Flakes (rolled)

- Quick / Instant Flakes (pre-cooked)

- Pre-blended / Mixes (Oat/Barley blends)

By Application

- Breakfast Cereals & Porridge

- Bakery & Confectionery Ingredients

- Snacks & Granola Bars

- Beverage Premixes (functional drinks)

- Animal Feed / Pet Food Ingredients

- Foodservice & Institutional Use

By Distribution Channel

- Hypermarkets / Supermarkets

- Convenience Stores

- Specialty & Health Food Stores

- Online / E-commerce

- HORECA / Foodservice