April 2026

The global shortening market size reached at USD 5.42 billion in 2025 and is expected to rise from USD 5.65 billion in 2026 to nearly reaching USD 8.18 billion by 2035, growing at a CAGR of 4.2% during the forecast period from 2026 to 2035. The growing investments and innovative production methods in food processing industries enable the expansion of shortening products.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 4.2% |

| Market Size in 2026 | USD 5.65 Billion |

| Market Size in 2027 | USD 5.88 Billion |

| Market Size by 2035 | USD 8.18 Billion |

| Largest Market | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Shortening refers to any fat that is solid at room temperature and used in baking to give foods a crumbly and tender texture by preventing gluten formation. It includes vegetable-based, animal-based, and blended fats, commonly used in the baking, frying, and food processing industries. The market covers both bulk shortening (industrial use) and retail-packaged shortening.

The various sectors and products, including vegan, plant-based shortening, bakery, confectionery, are experiencing technological advancements and free trade agreements. There is a major competitiveness among industries due to changing consumer preferences. The government regulations related to food safety and labeling impact the growth of the market significantly.

With the elevated prices for basic goods like staples, flour, sugar, and others in the U.S. and globally, consumers are facing problems related to grocery shopping. Consumers are making smart food choices and preferring plant-based alternatives due to rising health concerns. There are supply chain issues with emerging technological advancements.

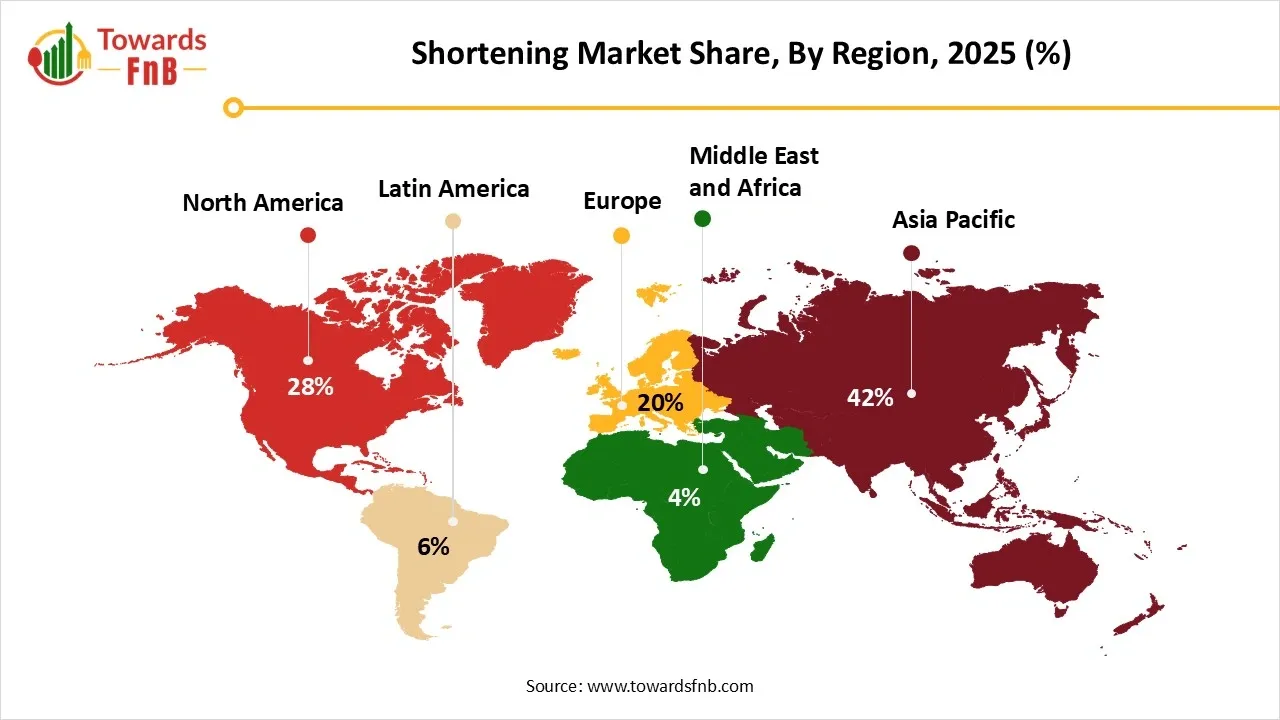

How Asia Pacific Dominated the Shortening Market in 2025?

Asia Pacific dominated the shortening market in 2025 owing to the initiatives and achievements of the food processing industries. The food processing sector plays a major role in offering farming jobs, increasing farm income, and reducing harvest losses in agriculture and related sectors. The Ministry budget and the government of India allocated Rs. 3290.00 crores to the Indian Ministry to develop and expand the food processing sector in the year 2024-25.

Asia Pacific Shortening Market Size 2025 to 2035

The Asia Pacific shortening market size was valued at USD 2.28 billion in 2025 and is expected to rise from USD 2.37 billion in 2026 to nearly reaching USD 3.48 billion by 2035, growing at a CAGR of 4.32% during the forecast period from 2026 to 2035.

How is the Growth of the Indian Food Processing Sector?

The Middle East and Africa are Expected to Grow at the Fastest CAGR in the Shortening Market During the Forecast Period

Due to economic diversification, sustainable practices, digitalization, and infrastructure development. The streamlining investments, public health initiatives, and child labor challenges also foster the growth of this region. The region is experiencing transformation in Africa’s exports and imports while introducing tools to resolve carbon emissions and climate change. The region is promoting sustainable economic development and increasing industrial transformation across the continent.

What is the Role of South African Governments in the Overall Growth and Achievements?

The government of South Africa is dedicated to health services, social welfare services, school education, housing, and agriculture. The national government provides leadership and formulates policies. The local government provides services related to health, education, housing, electricity, water, social development, roads, and municipal infrastructure services. The national government raises the revenue capacity, and this generated revenue is used to support initiatives and various services.

")

North America Shortening Market Trends

The demand for shortening in North America is being driven by the evolving consumer preferences toward healthier and plant-based products. Increasing awareness of dietary health benefits and a shift away from trans fats have prompted manufacturers to innovate with cleaner-label and non-hydrogenated options. The rise of vegan and vegetarian diets further contributes to this demand, as consumers seek versatile, plant-derived fats for culinary applications. Moreover, the expansion of the foodservice sector, inclusive of restaurants and bakeries, enhances market growth. Regulatory support for food safety and quality standards further accelerates this expansion.

The United States shortening market is experiencing consistent growth, primarily fueled by high demand from the commercial baking, processed food, and foodservice sectors. The increasing prevalence of plant-based and vegan shortenings is transforming the global food industry, driven by consumer preferences for healthier, more sustainable options. Prominent industry players such as Cargill, a global food corporation, and Bunge Limited, an agribusiness and food company, are leading this transformation by developing innovative shortening solutions derived from palm, sunflower, and soybeans.

How Palm Oil-Based Shortening Segment Dominated the Shortening Market in 2025?

The palm oil based shortening segment dominated the market in 2025 owing to the non-hydrogenated vegetable oil forms of palm oil, which make it a healthy alternative to traditional fats. The palm shortening is easily digestible and reduces the risk of digestive issues. The palm shortening has a high melting point due to which it helps to create stable structures in baked goods.

The canola oil-based shortening segment is expected to grow at the fastest CAGR in the market during the forecast period. Due to the nutritional benefits and culinary advantages of canola oil. It is low in saturated fat, vitamin K, vitamin E, and offers healthy fats for the heart. It is a healthy alternative to traditional shortenings like butter and lard and delivers various culinary applications.

What Made Solid Shortening the Dominant Segment in the Shortening Market in 2025?

The solid shortening segment dominated the market in 2025 owing to the improved texture, stability, and versatility of solid shortenings. It enables texture improvement, moisture retention, and stability.

The emulsified shortening segment is expected to grow at the fastest CAGR in the market during the forecast period. Due to the benefits of emulsifiers in terms of improved texture, enhanced aeration, and moisture retention. The emulsifiers allow the uniform distribution of fat in batter and dough.

How did the Bakery & Confectionery Segment Dominate the Shortening Market in 2025?

The bakery & confectionery segment dominated the market in 2025 owing to the improved texture, tenderness, crispiness, and longer shelf life of bakery and confectionery products. It also improves the functionality of doughs and batteries.

The ready meals/processed foods segment is expected to grow at the fastest CAGR in the shortening market during the forecast period. Due to benefits such as cost-effectiveness, extended shelf life and storage, and texture improvement in ready meals or processed food. It is a convenient alternative to butter which offers a neutral taste.

How Direct/B2B Segment Dominated the Shortening Market in 2025?

The direct/B2B segment dominated the market in 2025 owing to the smooth journey of buyers, improved control of salespeople, and efficient qualification of goods. The direct/B2B channels allow us to identify the pinpoints in businesses, address consumer needs, and use technologies.

The online retail segment is expected to grow at the fastest CAGR in the market during the forecast period. Due to fast order fulfilment, reduced customer frustration, increased sales, and improved customer satisfaction. The online retail channels allow us to streamline the website, offer various shipping options, and manage returns efficiently.

Shortening Market Share, By Packaging Type, 2025 (%)

| Segments | Shares (%) |

| Bulk Packs | 55% |

| Retail Packs (500g, 1kg, 2kg) | 10% |

| Sachets | 5% |

| Tubs/Cans | 17% |

| Industrial Drums | 13% |

What Made Bulk Packs the Dominant Segment in the Shortening Market in 2025?

The bulk packs segment dominated the market in 2025 owing to the cost savings, convenience, efficiency, and environmental benefits of these products. The bulk packs offer the potential for price stability, lower per-unit price, and reduced shipping costs.

The tubs/cans segment is expected to grow at the fastest CAGR in the shortening market during the forecast period. Due to the benefits of shortening in baking, cooking, high fat content, and neutral flavor. The tubs/cans offer enhanced moisture retention, stability at room temperature, and versatile applications.

Shortening Market Share, By End User, 2025 (%)

| Segments | Shares (%) |

| Industrial Food Manufacturers | 65% |

| Foodservice (QSRs, Bakeries) | 20% |

| Household | 15% |

How did the Industrial Food Manufacturers Segment Dominate the Shortening Market in 2025?

The industrial food manufacturers segment dominated the shortening market in 2025 owing to the advantages of shortening in industrial baked goods, which can avoid changes in product stability, and offer improved texture and structure. The use of vegetal fat, which is the most widely used shortening ingredient in the preparation of baked goods, raises the growth of industrial food manufacturers.

The foodservice (QSRs/Bakeries) segment is expected to grow at the fastest CAGR in the market during the forecast period. Due to the improved shelf life, texture, and flavor of food products due to the inclusion of shortening. The wide use of shortening in baked goods, pastries, and many other products raises its demand in food services.

Shortening Market Share, By Fat Type/Content, 2025 (%)

| Segments | Shares (%) |

| Hydrogenated | 25% |

| Non-Hydrogenated | 38% |

| Interesterified Fats | 12% |

| Trans Fat-Free | 15% |

| Low-Fat Shortening | 10% |

How Non-Hydrogenated Segment Dominated the Shortening Market in 2025?

The non-hydrogenated segment dominated the market in 2025 owing to the presence of lower saturated fat than butter and the non-hydrogenated products are free of cholesterol. The use of partially hydrogenated oil in most butter substitutes or shortenings raises the importance of these products.

The trans-fat-free segment is expected to grow at the fastest CAGR in the market during the forecast period. Due to the bakery potential of trans-fat-free products. It is possible to produce and introduce cookies from trans-fat-free stearic acid-rich and oleic acid-rich oils. Trans fats are advantageous for healthy hearts due to their flavor stability and extended shelf life.

Cargill, Bunge, and Wilmar

Fuji Oil Group

By Source

By Form

By Usage/Application

By Distribution Channel

By Packaging Type

By End-User

By Fat Type/Content

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Shortening Market