April 2026

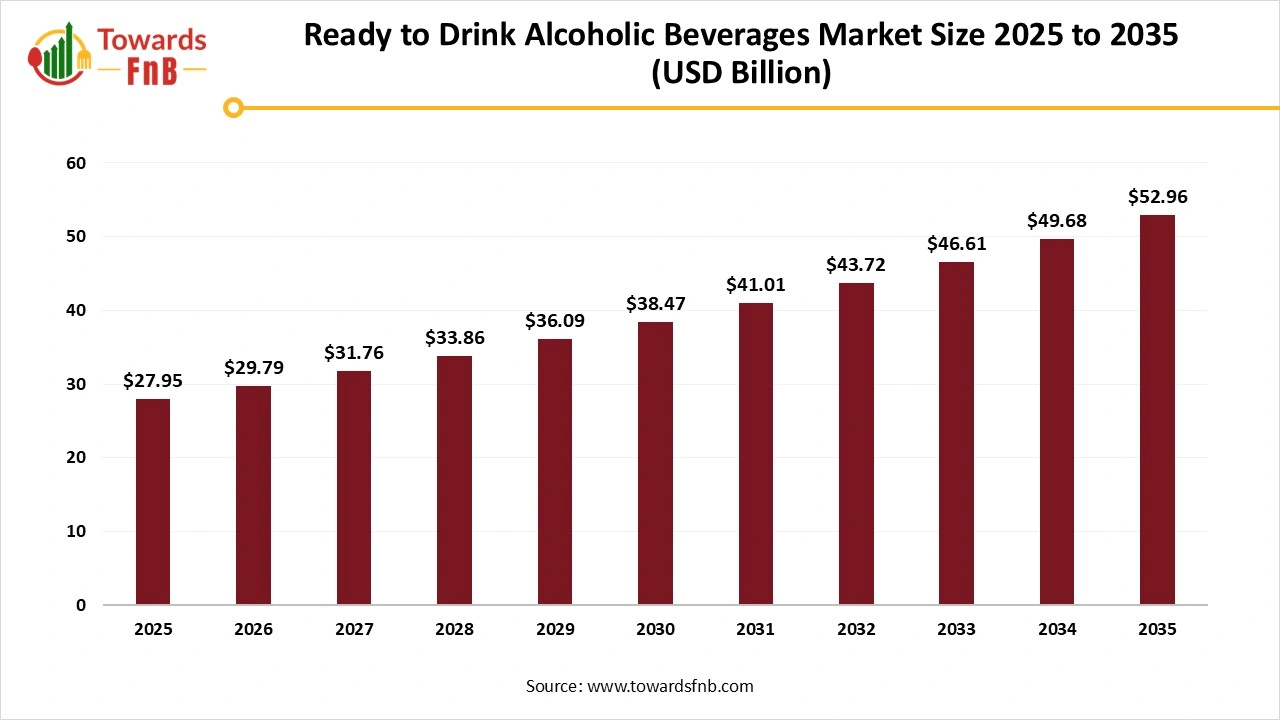

The global ready to drink alcoholic beverages market size stood at USD 27.95 billion in 2025 and is expected to grow steadily from USD 29.79 billion in 2026 to reach nearly USD 52.96 billion by 2035 with a CAGR of 6.6% during the forecast period from 2026 to 2035. Growing demand for portable and simple-to-consume beverage alternatives driving the market.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.6% |

| Market Size in 2026 | USD 29.79 Billion |

| Market Size in 2027 | USD 31.76 Billion |

| Market Size by 2035 | USD 52.96 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Ready to drink alcoholic beverages or ready to drink options, are pre-blended alcoholic drinks that are available in a convenient, ready-to-consume format. They usually mix spirits, wine, or beer with mixers and flavors, creating a simple method to savor a cocktail. These ready-to-drink beverages are available in multiple formats, such as bottles, cans, and cartons, catering to various tastes and situations.

Flavor innovation in the ready to drink alcoholic beverage sector is flourishing, fueled by a consumer appetite for distinctive experiences, functional wellness, and convenience. There are chances in broadening beyond known fruit flavors to present refined herbal and botanical infusions such as ginger, turmeric, mint, and lemongrass, along with distinctive tropical combinations and exotic fruits. Creating unique flavor combinations that prioritize natural components and health-oriented choices, like low-alcohol or functionally-augmented RTDs is essential for engaging the attention of bold and health-minded consumers.

The regulatory environment presents a notable obstacle for the ready to drink alcoholic beverages sector, as diverse regions enforce different regulations regarding production, labeling, and distribution. Strict marketing and labeling regulations demand explicit disclosures regarding ingredients, alcohol levels, and health warnings. In the U.S., the Alcohol and Tobacco Tax and Trade Bureau (TTB) implement these rules, raising the operational complexity and expenses, driven by a blend of convenience and a demand for quality, varied choices.

Raw Material Procurement

Processing and Preservation

Packaging and Branding

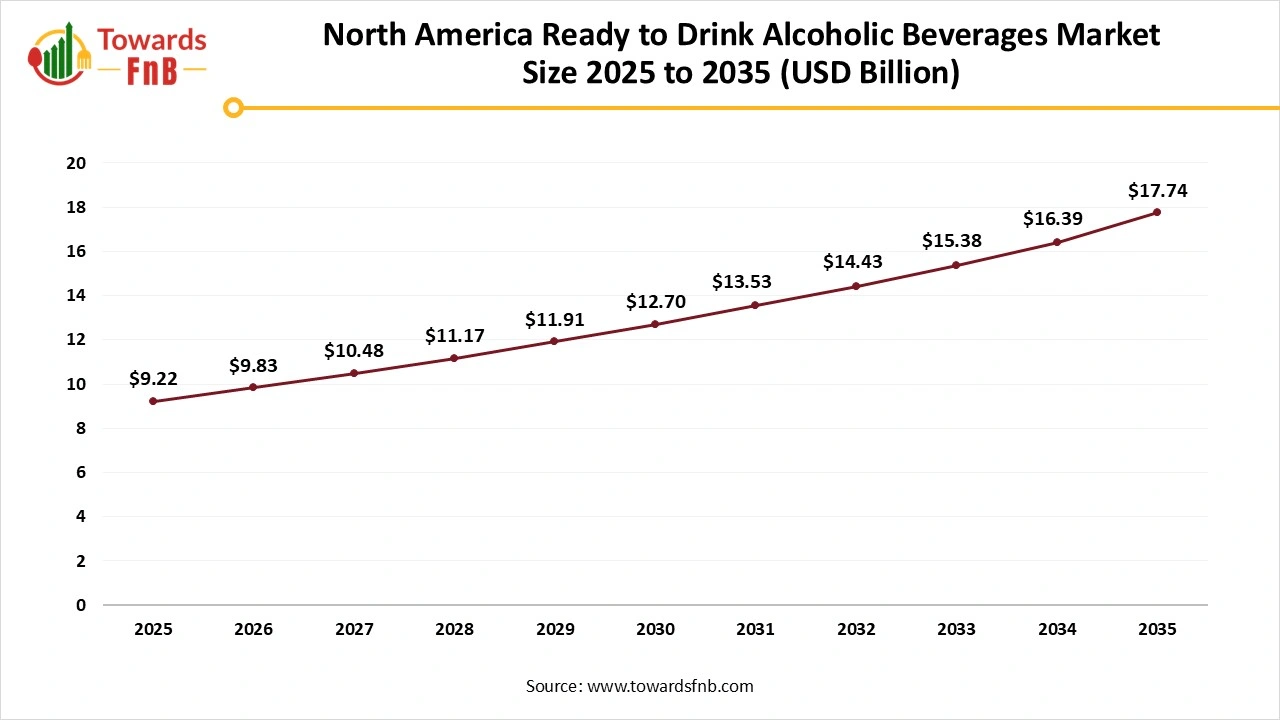

North America Dominated the Ready to Drink Alcoholic Beverages Market in 2025

Consumers are progressively looking for substitutes for conventional beer and wine, and RTDs provide a tasty and convenient option for social events, outdoor adventures, and home enjoyment. RTDs, including canned cocktails and pre-mixed beverages, offer convenience and simplicity for consumers who are on the move. This trend is influenced by evolving lifestyles and the need for convenient drinking choices. RTDs attract younger consumers seeking fashionable and Instagram-worthy beverages.

North America Ready to Drink Alcoholic Beverages Market Size and Growth 2025 to 2035

The North America ready to drink alcoholic beverages market size was valued at USD 9.22 billion in 2025 and is expected to grow steadily from USD 9.83 billion in 2026 to reach nearly USD 17.74 billion by 2035 with a CAGR of 6.76% during the forecast period from 2026 to 2035.

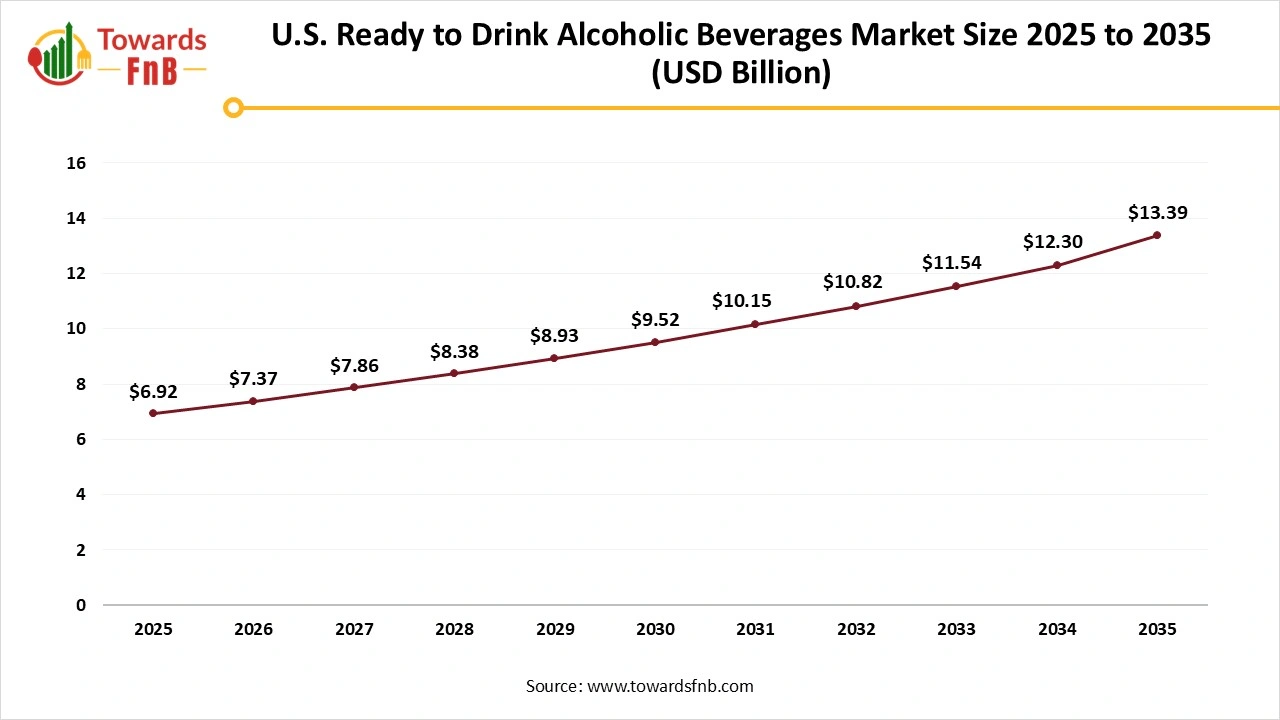

United States Ready to Drink Alcoholic Beverages Market

Ready to drink alcoholic beverage market expanded rapidly in United States. A significant trend is the rising need for convenience and portability. Consumers, particularly millennials and Gen Z, are attracted to RTDs as a convenient choice for social events, outdoor activities, and enjoying at home. Although convenience continues to be a primary factor, consumers are progressively looking for better-quality ingredients, distinctive flavor combinations, and elegant packaging, fueling the demand for high-end RTD choices.

U.S. Ready to Drink Alcoholic Beverages Market Size and Growth 2025 to 2035

The U.S. ready to drink alcoholic beverages market size was calculated at USD 6.92 billion in 2025 and is expected to grow steadily from USD 7.37 billion in 2026 to reach nearly USD 13.39 billion by 2035 with a CAGR of 6.82% during the forecast period from 2026 to 2035.

Asia Pacific Expects the Significant Growth During the Forecast Period

The region's market expansion is linked to major factors, including rising purchasing and spending capabilities resulting from economic advancements, the swift embrace of western culture, shifting consumer preferences, and enhanced living standards. Increasing disposable incomes, a growing middle class, and evolving social dynamics are motivating consumers to pursue premium spirits, wines, and artisanal beers. The movement of consumers towards healthier lifestyles, combined with adults' desire to experiment with new drink options, fuels the sales of ready-to-drink beverages in the area.

")

China Ready to Drink Alcoholic Beverages Market

The market for ready-to-drink alcoholic beverages in China is growing considerably because of several key factors. The rise of China's middle class and urban development has boosted disposable incomes, leading to a higher consumption of convenience items such as ready-to-drink beverages. Moreover, companies are compelled to innovate and attract younger demographics, who seek unique and daring drinking experiences due to changing consumer tastes that prioritize premium quality and exceptional flavors.

The 5th TaiKoo Hui Craft Beer Festival in Guangzhou showcased how young people in China are transforming drinking culture to favor lighter, fruitier, and more communal alcohol experiences. Showcasing low-ABV options such as strawberry milkshake cider and guava gose (typically 3 to 5% ABV), the event merged craft beer with lifestyle branding and music, appealing to young consumers who value flavor, aesthetics, and social experiences over excessive drinking.

Which Product Type Segment Dominated the Ready to Drink Alcoholic Beverages Market in 2025?

Hard seltzers segment led the market in 2025. Hard seltzers attract consumers mindful of their diet, offering low-calorie and low-sugar options as refreshing alternatives to conventional alcoholic drinks. This target market consists of people who emphasize wellness and seek alcoholic choices that correspond to their healthier lifestyle preferences. Numerous buyers seek less sugar, low-calorie, organic, and health-oriented drinks that not only meet their needs but also fit their keto and vegan lifestyles. Numerous producers have been providing items in this category. Dashmote’s recent data shows that the most featured brand on US food delivery services in Q4, 2022 was Polar Seltzer.

Pre-Mixed Cocktails and Flavored RTD Spirits Segment is Observed to Grow at the Fastest Rate During the Forecast Period

The surge in cocktail culture and the trend toward premium ready-to-drink alcoholic beverages are fueling market expansion. Consumers desire bar-quality cocktails crafted with premium ingredients, and there is an increasing trend in flavored, low-sugar, and organic premix alternatives.

Ready to Drink Alcoholic Beverages Market Share, By Packaging Type, 2025 (%)

| Segments | Shares (%) |

| Cans (200–500 ml) | 52% |

| Glass bottles (250–500 ml) | 19% |

| PET / plastic bottles | 17% |

| Cartons / Tetra Pak / aseptic | 12% |

Why did the Cans Segment Dominate the Ready to Drink Alcoholic Beverages Market in 2025?

Cans segment held the dominating share of the ready to drink alcoholic beverages market in 2025. Consumers favor cans as a packaging choice for their convenience, as they are lightweight and less likely to shatter. Their lids that can be resealed enable gradual use, minimizing waste. The secure seal also shields contents from light and oxygen, maintaining flavor integrity. Cans are perfect for outdoor gatherings and activities, providing a practical and convenient packaging option. Additionally, the eco-friendly characteristics of aluminum cans, their capacity to maintain product freshness and carbonation, and their economical shipping costs are essential elements contributing to their prevalence.

Glass Bottles and Aseptic Cartons Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Because of their attractiveness in premiumization, branding, and sustainability. Glass provides a strong perception of quality, personalization, and safety without releasing harmful chemicals, in line with consumer preferences for luxury items and health-focused decisions. Aseptic cartons offer portability, prolonged shelf life, and superior barrier characteristics for both alcoholic and non-alcoholic drinks, catering to the need for convenience and innovation, especially in single-serve formats for consumption on the go.

Ready to Drink Alcoholic Beverages Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Off-trade retail | 58% |

| On-trade | 18% |

| E-commerce / online alcohol retail | 13% |

| Convenience stores / specialty retail | 11% |

Which Distribution Channel Dominated the Ready to Drink Alcoholic Beverages Market in 2025?

Off trade retail segment dominated the market with the largest share in 2025. This encompasses supermarkets, convenience stores, hypermarkets, and online platforms, where consumers are progressively buying RTDs for home use and informal gatherings. The move to consuming alcohol at home, alongside attractive pricing and promotions, drives growth in off-trade sales. A variety of flavors and pack sizes, coupled with robust retail visibility, improves accessibility. Retailers boost product visibility through appealing packaging and promotions, encouraging impulse buys and raising sales via in-store campaigns and seasonal deals.

E-commerce & On-Trade Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

The swift growth of on-trade such as bars, restaurants, and hotels along with e-commerce channels is projected to offer substantial growth prospects for the market throughout the forecast period. The change in consumer preference for convenience, high-quality experiences, and online shopping has increased the demand for RTD alcoholic drinks in these channels.

Ready to Drink Alcoholic Beverages Market Share, By Alcohol Content, 2025 (%)

| Segments | Shares (%) |

| Low-alcohol RTDs (<5% ABV) | 57% |

| Mid-alcohol RTDs (5–8% ABV) | 26% |

| High-alcohol RTDs (>8% ABV) | 17% |

What Made the Low-Alcohol RTDs Segment Dominant in the Ready to Drink Alcoholic Beverages Market in 2025?

Low-alcohol RTDs segment held the largest share of the market in 2025. Health-conscious consumers seek the social experience of drinking while avoiding the negative effects linked to traditional alcohol. The demand for low-alcohol beverages has been enhanced by the development of ready-to-drink (RTD) low-alcohol cocktails and functional beverages. They are simple to eat and offer added health advantages, contributing to the wellness movement. Major companies in the beverage sector have assessed this segment and expanded their offerings to meet the growing demand.

Mid-Alcohol RTDs Segment is Observed to Grow at the Fastest Rate During the Forecast Period

This sector is quickly expanding due to the worldwide rise of the "mindful drinking" movement, which emphasizes lower-ABV, low-calorie, and low-sugar choices in a convenient format. Customers, particularly younger demographics, are looking for healthier options and equilibrium, increasing the popularity of lighter RTDs such as hard seltzers and wine-based drinks. Brands are addressing this demand by crafting lighter options such as hard seltzers, low-calorie cocktails, and beverages infused with wellness ingredients to provide healthier, balanced selections.

Kraft Heinz

Suntory Global Spirits

The Coca Cola Company and Bacardi Limited

By Product Type/Category

By Packaging Type

By Distribution Channel

By Alcohol Content

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Ready to Drink Alcoholic Beverages Market