April 2026

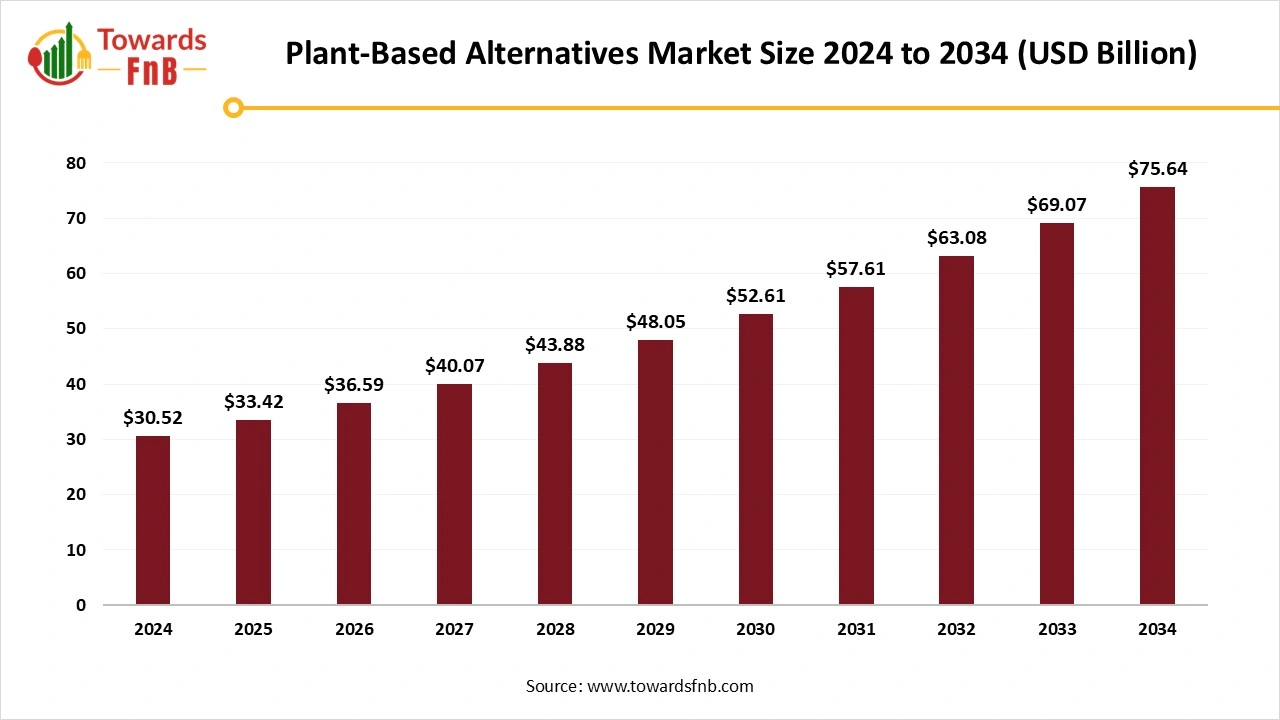

The global plant-based alternatives market size reached at USD 33.52 billion in 2025 and is expected to grow steadily from USD 36.72 billion in 2026 to reach nearly USD 83.45 billion by 2035, with a CAGR of 9.55% during the forecast period from 2026 to 2035. The market is driven by health consciousness, environmental concerns, and dietary shifts towards vegan and flexitarian diets.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 9.55% |

| Market Size in 2026 | USD 36.72 Billion |

| Market Size in 2027 | USD 40.23 Billion |

| Market Size by 2035 | USD 83.45 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The plant-based alternatives market is a growing industry focused on producing and selling products that substitute traditional animal-based foods, such as meat, dairy, and eggs. These alternatives aim to replicate the taste, texture, and functionality of their animal counterparts to appeal to a broad consumer base that includes vegans, vegetarians, and those who want to reduce their meat or dairy consumption for health, environmental, or ethical reasons.

Innovations in plant-based substitutes are improving product authenticity, nutritional benefits, and sustainability via methods such as 3D printing, precision fermentation, and sophisticated structuring techniques. Technologies like high-pressure processing, pulse electric fields, and AI are enhancing flavor, texture, and longevity, whereas computational protein design enables the creation of novel ingredients from the ground up to better replicate animal products. Numerous additional groundbreaking technologies are surfacing that are elevating plant-based food processing to new heights. These comprise ohmic heating, shear-cell technology, and electrospinning, enabling companies to produce genuine products with unmatched accuracy and speed.

Raw Material Procurement

Processing of Plant Based Alternatives

Packaging of Plant Based Alternatives

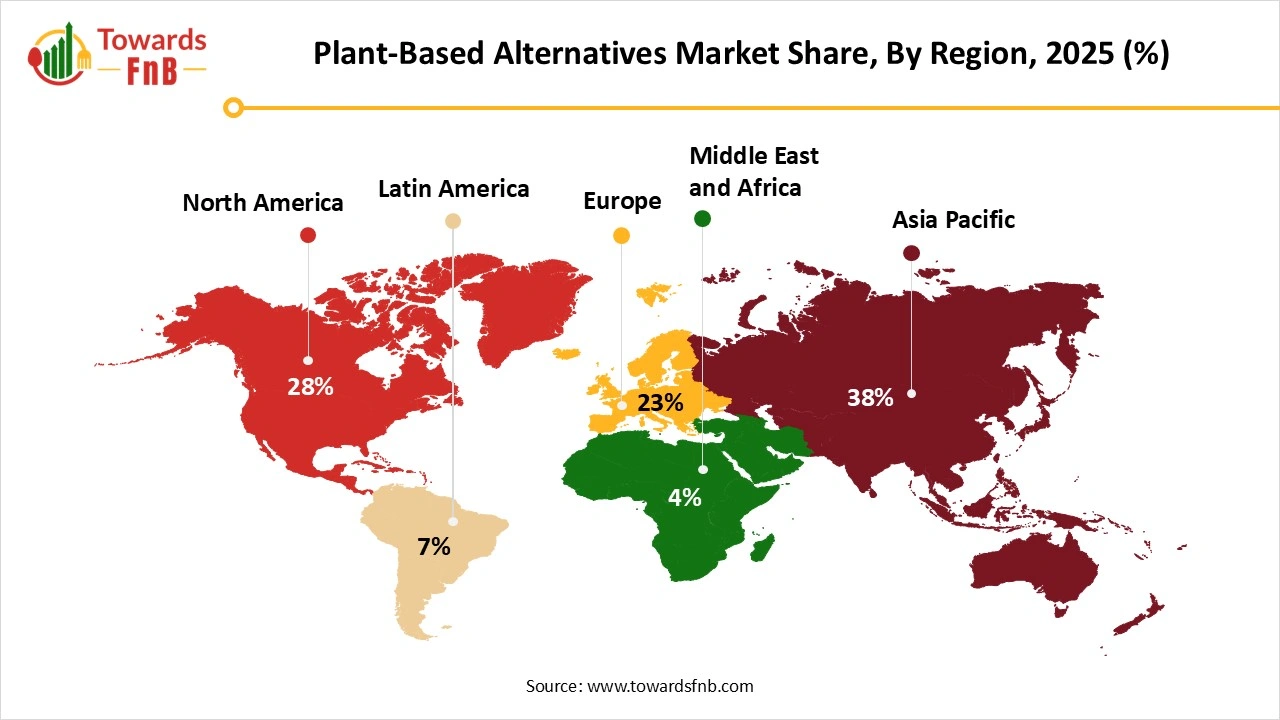

Asia Pacific Region Dominance in the Plant-Based Alternatives Market

Asia Pacific dominated the plant-based alternatives market in 2025. The expansion of the market in the Asia Pacific area is shaped by various significant elements. Heightened health consciousness among consumers has resulted in greater recognition of the advantages connected to a plant-based diet, especially its ability to lower the risk of chronic diseases and improve overall wellness. Drinks such as soy, rice, oat, and almond milk are quite popular. The on-trade sector, including restaurants and cafes, is witnessing a rise in the adoption of plant-based choices for drinks like coffee. Important markets consist of China, India, and Japan, showcasing substantial investment in plant-based food innovations and a robust presence of both major corporations and new ventures. India, home to one of the globe’s largest vegetarian populations and a rich history of plant-based culinary traditions, is experiencing a major shift in its food sector.

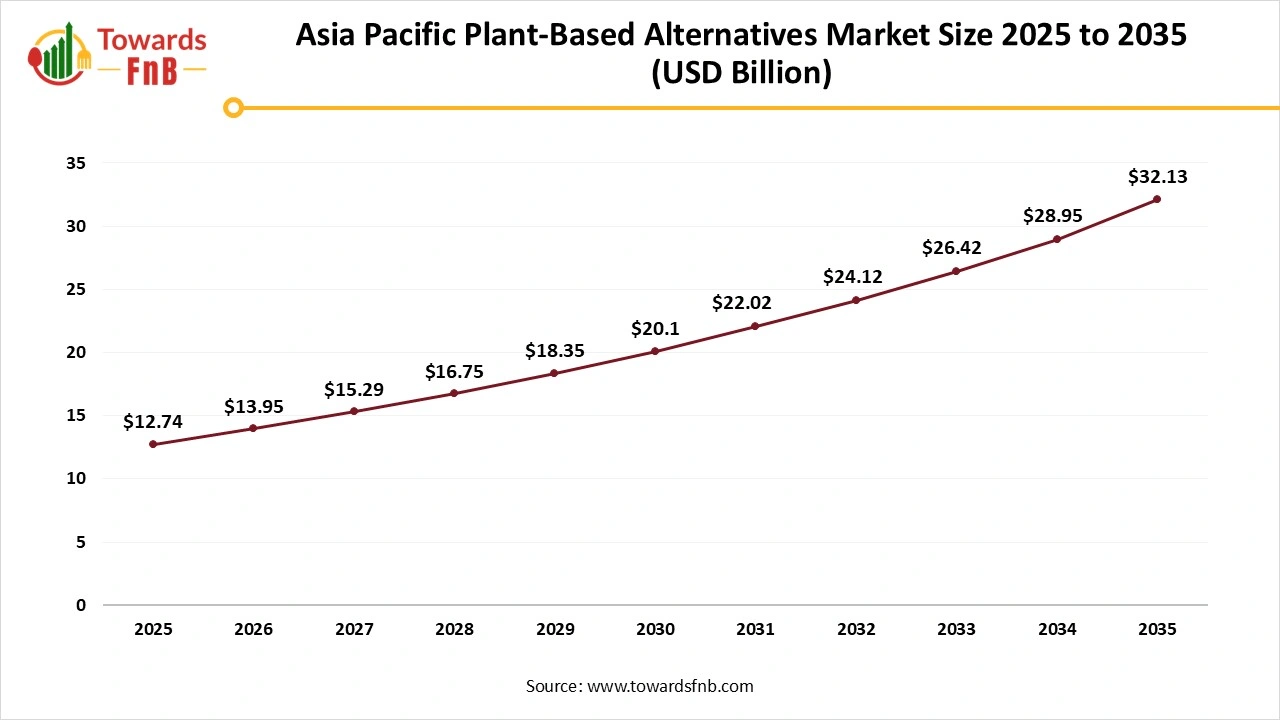

Asia Pacific Plant-Based Alternatives Market Size 2025 to 2035

The Asia Pacific plant-based alternatives market size was valued at USD 12.74 billion in 2025 and is expected to grow steadily from USD 13.95 billion in 2026 to reach nearly USD 32.13 billion by 2035, with a CAGR of 9.69% during the forecast period from 2026 to 2035.

India Plant-Based Alternatives Market Analysis

The Indian market for plant-based alternatives has seen significant expansion lately, driven by increasing consumer interest in healthier and more sustainable options compared to conventional food products. A variety of SMEs and FMCGs have already penetrated India's plant-based food market, providing plant-derived substitutes for meat, poultry, seafood, dairy, and vegan food for dogs and cats. The industry is experiencing growth with more than 50 start-ups currently operating in the field.

Growing Demand of Plant Based Alternatives in the North America

North America expects the significant growth during the forecast period. Increasing health consciousness and environmental issues, the rising appeal of vegan and flexitarian diets, the embrace of technological innovations and novel products, along with heightened investments in alternative food items are projected to boost the North America Plant-based Food Market during the forecast period. Increasing investments in plant-based startups and collaborations with food service chains have improved accessibility. The market is further driven by consumer demand for sustainable and cruelty-free alternatives, along with the increasing rates of lactose intolerance and obesity. Millennials and Gen Z play a significant role in the rising popularity of plant-based food.

U.S. Plant-Based Alternatives Market Analysis

The plant-based alternatives market in the United States is an expanding sector of the food industry, fueled by an increasing appetite for healthier and more sustainable dining choices. Data from the Good Food Institute indicates that almost 75% of consumers worldwide are open to adopting plant-based options for environmental purposes. In the United States, nearly 50% of restaurant menus now feature plant-based options, reflecting a 62% increase over the last ten years. Interest in health, sustainability, and ethics fuels the demand for plant-based alternatives in the U.S., resulting in notable market expansion.

")

Europe Plant-Based Alternatives Market Growth

More Europeans are adopting flexitarian diets due to health concerns such as obesity, heart disease, and food intolerances. This is driving the demand for plant-based meat alternatives that are regarded as healthier, lower in fat, and free of cholesterol. Germany, the UK, and the Netherlands, along with several other nations, have demonstrated significant growth in the market. Younger buyers are driving demand due to their openness to new ideas and responsible consumption. Major retail chains across Europe are rapidly expanding their range of plant-based offerings, introducing private labels and partnering with startups to enhance selection. Major retail chains across Europe are rapidly expanding their range of plant-based offerings, introducing private labels and partnering with startups to enhance variety.

Germany Plant-Based Alternatives Market Analysis

Germany has a strong demand for plant-based alternatives, being Europe's largest market for such products, fueled by a significant flexitarian demographic and growing environmental consciousness. Sales volumes are increasing, with growth in segments such as plant-based milk, beverages, and meat, while prices for private-label items are becoming more competitive, occasionally even lower than their animal-based equivalents. In 2023, plant-based packaged food products in Germany reported total value sales of US$659.5 million. The plant-based food categories with the highest value sales primarily consisted of plant-based dairy items and substitutes, accounting for a total share of 89.8% (including milk, yogurt, cheese, dairy desserts, cream), plant-based ice cream (3.9%), and plant-based meat and seafood substitutes (3.7%) in the sector in 2023.

Expanding Plant-Based Alternatives Market in the Middle East and Africa

The market for plant-based alternatives in the Middle East and Africa is witnessing substantial and swift expansion, largely fueled by rising health awareness, a high rate of lactose intolerance, and government efforts supporting sustainable food practices. The market is expected to grow considerably in the next few years, with the UAE and Saudi Arabia driving the expansion in the Middle East and South Africa in Africa. Programs such as Saudi Arabia's Vision 2030 and the UAE's National Food Security Strategy 2051 are advocating for sustainable farming and requiring plant-based choices in public cafeterias, thereby facilitating faster market adoption.

UAE Plant-Based Alternatives Market Analysis

The expansion of the UAE's plant-based alternatives market is mainly fueled by a growing health awareness among consumers, heightened recognition of environmental sustainability, and a transition toward ethical dietary practices. The UAE's varied population, which includes a large expatriate community, creates a demand for diverse food choices, such as plant-based items.

Latin America Plant-Based Alternatives Market Potential

The market for plant-based alternatives in Latin America is seeing impressive growth, fueled by consumer interest in healthier and more eco-friendly choices. The market is anticipated to keep growing, with plant-based meat and dairy items demonstrating robust performance. A recent study by Veganuary and HappyCow revealed that vegan-friendly food establishments in Latin America rose by 21% in 2024. Brazil had the highest number of vegan-friendly eateries, with Mexico and Colombia following.

Brazil Plant-Based Alternatives Market Analysis

The market in Brazil is propelled by increasing health awareness among younger buyers, governmental backing for sustainable farming practices, and the development of retail infrastructure combined with improved e-commerce platforms that boost product availability. Moreover, growing consumer consciousness about the environmental and ethical advantages of plant-based diets is driving the market share for plant-based foods in Brazil. In Brazil, plant-based sales are increasing due to the demand for alternatives to meat and dairy for health and ethical motivations, along with the push for enhanced sustainability within the food sector.

Plant-Based Alternatives Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Dairy Alternatives | 50% |

| Meat Alternatives | 20% |

| Egg Substitutes and Condiments | 17% |

| Others | 13% |

Why did the Dairy Alternatives Segment Dominate the Plant-Based Alternatives Market?

Dairy alternatives segment led the market in 2025. The demand for dairy substitutes is mainly propelled by consumers who are lactose intolerant. Additionally, the general consumers are increasingly viewing lactose-free products as healthy substitutes for traditional dairy. Milk alternatives such as almond, soy, and oat options are seen as healthier choices, providing reduced saturated fats, absence of cholesterol, and occasionally enriched with vitamins and minerals.

Meat Alternative Segment is Observed to Grow at the Fastest Rate During the Forecast Period

The growing popularity of vegan and vegetarian diets, heightened health awareness among millennials, and escalating worries about environmental effects propel the market's expansion. Progress in food science and technology is resulting in more authentic plant-based meat alternatives. Consumers are progressively worried about the moral treatment of animals in industrial farms. This has resulted in an increasing trend towards cruelty-free items, with meat alternatives providing a distinct option.

Egg substitutes and condiments segment is expanding significantly, fueled by increased plant-based diets, vegan lifestyles, egg allergies, and health-focused decisions. Major market segments consist of plant-based proteins such as soy and wheat, uses in baking and sauces, and distribution via online platforms and grocery stores. Key companies are creating new formulations to enhance flavor and texture in order to seize this expanding market.

Plant-Based Alternatives Market Share, By Source, 2025 (%)

| Segments | Shares (%) |

| Soy | 50% |

| Almond | 25% |

| Wheat | 15% |

| Others | 10% |

How did the Soy Segment Dominate the Plant-Based Alternatives Market?

The soy segment held the dominating share of the plant-based alternatives market in 2025, owing to its significant nutritional benefits, featuring a complete amino acid profile that renders it a nutritional powerhouse. Its prevalence is also attributed to its adaptability in producing various textures (such as tofu, TVP, and isolates) for numerous meat and dairy substitutes, its lower price and ready accessibility for producers, and a lengthy history of consumer approval as a meat alternative.

Almond Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Because of a mix of its appealing flavor and consistency, believed health advantages, and broad consumer approval. Its smooth, subtle taste serves as a flexible alternative to dairy, attracting individuals who are lactose intolerant and those adhering to vegan or vegetarian lifestyles. Prominent brands have extensively promoted almond milk, making it a well-known and reliable option.

The wheat segment is growing rapidly, due to its capacity to deliver a preferred meat-like texture, plentifulness, and flexibility, making it a favored option for producers of items such as burgers, sausages, and seitan. The characteristics of wheat protein, including its superior binding capabilities, position it as a favored option for food producers. In areas where wheat is intensely grown, such as India, this can render wheat protein a more economical choice.

Plant-Based Alternatives Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Supermarkets and Hypermarkets | 55% |

| Convenience Stores | 14% |

| Online Stores | 15% |

| Others | 16% |

Which Distribution Channel Dominated the Plant-Based Alternatives Market?

Supermarkets and Hypermarkets segment dominated the market with the largest share in 2025, owing to their extensive product range that offers consumers a convenient one-stop shopping experience across diverse categories such as meat and dairy alternatives. These big retailers can carry a wide selection of brands and items, allowing customers to easily discover various choices, from well-known brands to innovative products.

Online Stores Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Driven by the ease of e-commerce, direct-to-consumer (DTC) choices, and the capability to connect with a broader audience. This is backed by the rising need for home delivery, the broader range of products usually found online, and the capacity of e-commerce to serve niche and specialty items. The digital realm enables brands to leverage social media, influencer marketing, and targeted advertisements to engage with consumers and enhance brand visibility.

The convenience store segment for plant-based alternatives is growing due to the demand for convenient, grab-and-go options that align with consumers health, ethical, and environmental concerns. This growth is fueled by busy lifestyles, increased health awareness, a desire for sustainable products, and improvements in food technology. Convenience stores are stocking these products to cater to a wider demographic of consumers looking for quick and accessible choices.

ACCRO

Kate Farms

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches / Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

Recent News & Strategic Updates

By Type

By Source

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Plant-Based Alternatives Market