April 2026

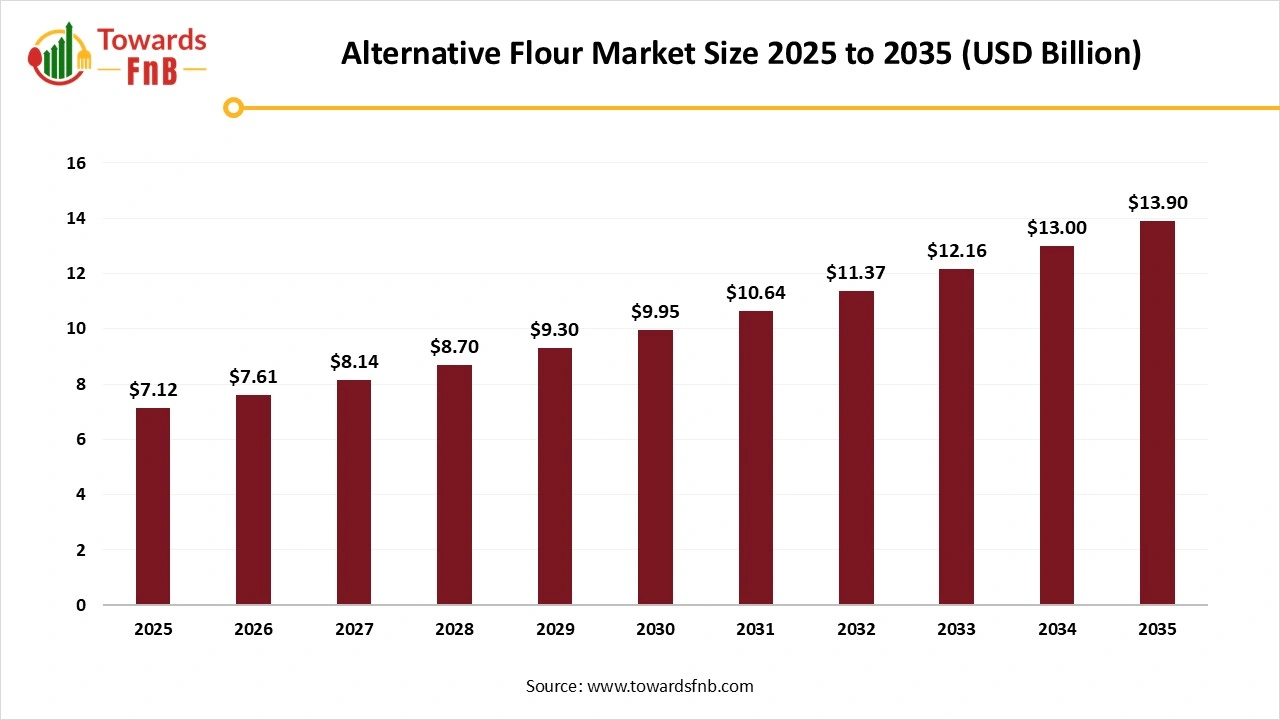

The global alternative flour market size stood at USD 7.12 billion in 2025 and is expected to grow steadily from USD 7.61 billion in 2026 to reach nearly USD 13.90 billion by 2035, with a CAGR of 6.92% during the forecast period from 2026 to 2035. This market is growing due to rising consumer demand for gluten-free, plant-based based and nutrient-rich baking and cooking options.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.92% |

| Market Size in 2026 | USD 7.61 Billion |

| Market Size in 2027 | USD 8.14 Billion |

| Market Size by 2035 | USD 13.90 Billion |

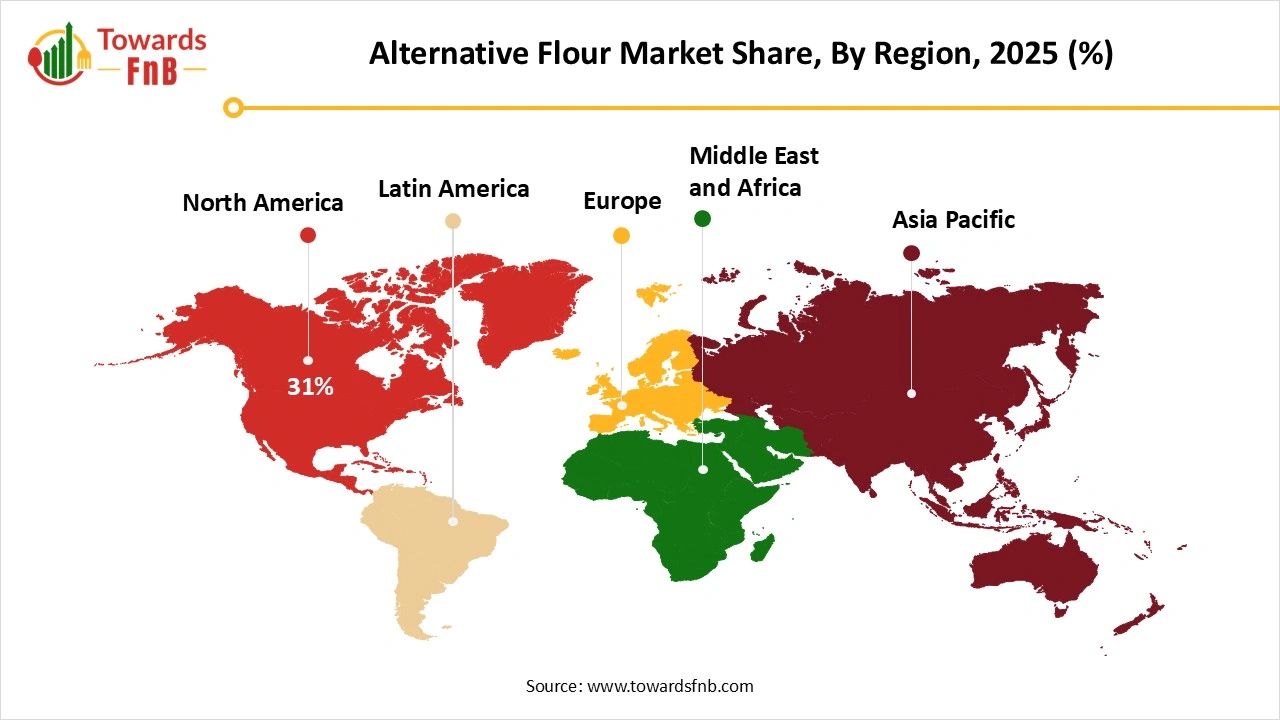

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The alternative flour market refers to the production, distribution, and consumption of flours made from non-traditional sources such as nuts, seeds, legumes, grains, and tubers. These flours serve as substitutes for conventional wheat flour, providing various health benefits such as gluten-free, low-carb, and nutrient-rich options. Alternative flours are increasingly being used in food products like bakery items, snacks, pasta, and meat substitutes, driven by growing consumer demand for gluten-free, allergen-free, and health-conscious ingredients.

Bread flour, whole wheat flour, and Italian 00 flour are examples of specialty flours that are becoming more popular, according to Instacart; their use could increase by as much as 50% by 2025. Home bakers who began baking during the pandemic and have since made baking a way of life are primarily responsible for this growth. Because of their capacity to produce artisan-style results, these flours are being used in recipes for homemade sourdough pizza and cakes. To satisfy this demand, supermarkets and online retailers are expanding their selection of high-quality flours, and customers are learning more about how various flours affect hydration, gluten formation, and overall bake quality. (Source: Real Simple)

Pistachio flour and other exotic flours are becoming popular pantry staples in 2025 because of their rich flavor, health advantages, and compatibility with keto and gluten-free diets. Because of their distinctive colors and textures, as well as their nutritional value, consumers are increasingly choosing functional flour made from unusual ingredients like bananas, cassava, tiger nuts, and now pistachios. Pistachio was even named the 2025 biggest trending flavor by Food and Wine, and it can be found in everything from smoothie bowls to crusts to pastries. Particularly among gourmet and health-conscious consumers, the growing interest in superfoods and a variety of cuisines is promoting this trend toward flours that combine style and functionality. (Source: Better Homes & Garden)

With the rapid rise of regenerative farming techniques, sustainability has emerged as a key factor in the alternative flour sector. As an illustration, consider the introduction of the King Arthur Baking Company's Climate Blend, a flour made from wheat that has been regeneratively grown to enhance soil health, biodiversity, and carbon capture. Growing environmental consciousness has led to consumers actively seeking out products that lessen their ecological impact. Regenerative flours offer superior quality and versatility for baking, in addition to helping the environment. Eco-conscious consumers are becoming more trusting and loyal to brands that use sustainable sourcing, pointing to a time when environmental responsibility will be just as significant as taste and functionality. (Source: EatingWell)

For lifestyle health or medical reasons, consumers are increasingly adhering to plant-based keto gluten gluten-free, and paleo diets. The market and paleo diets. The market for non-wheat flours derived from rice, oats, almonds, coconut, and legumes is growing as a result of this change. Customers are being pushed to look into alternatives due to the rising prevalence of gluten sensitivity, celiac disease diagnoses, and knowledge of the inflammatory reactions to refined grains. Market visibility has also increased as a result of celebrity chefs and health influencers advocating grain-free recipes. Opportunities to market alternative flours as commonplace items rather than specialized goods are presented by this trend.

Many alternative flours behave differently when baked; if not prepared correctly, they can produce textures that are dense, crumbly, or dry. Additionally, some taste strong or strange (e.g., chickpea or buckwheat), which might not be to everyone's taste. One of the biggest challenges is reproducing the softness and elasticity of products made from wheat. Producers frequently have to use additives or mix different flours to get around this, which raises the complexity and expense of formulation. If the final product doesn't taste as good as expected, customer satisfaction and repeat business may suffer.

North America Dominated the Alternative Flour Market in 2025

Driven by the increasing consumer preference for gluten-free, plant-based based and clean-label food products. The region witnessed a strong demand for cereal and nut-based flours due to growing health awareness and the popularity of low-carb and paleo diets. An established food processing industry and rising innovations in health-centric baking contributed to its dominant market share.

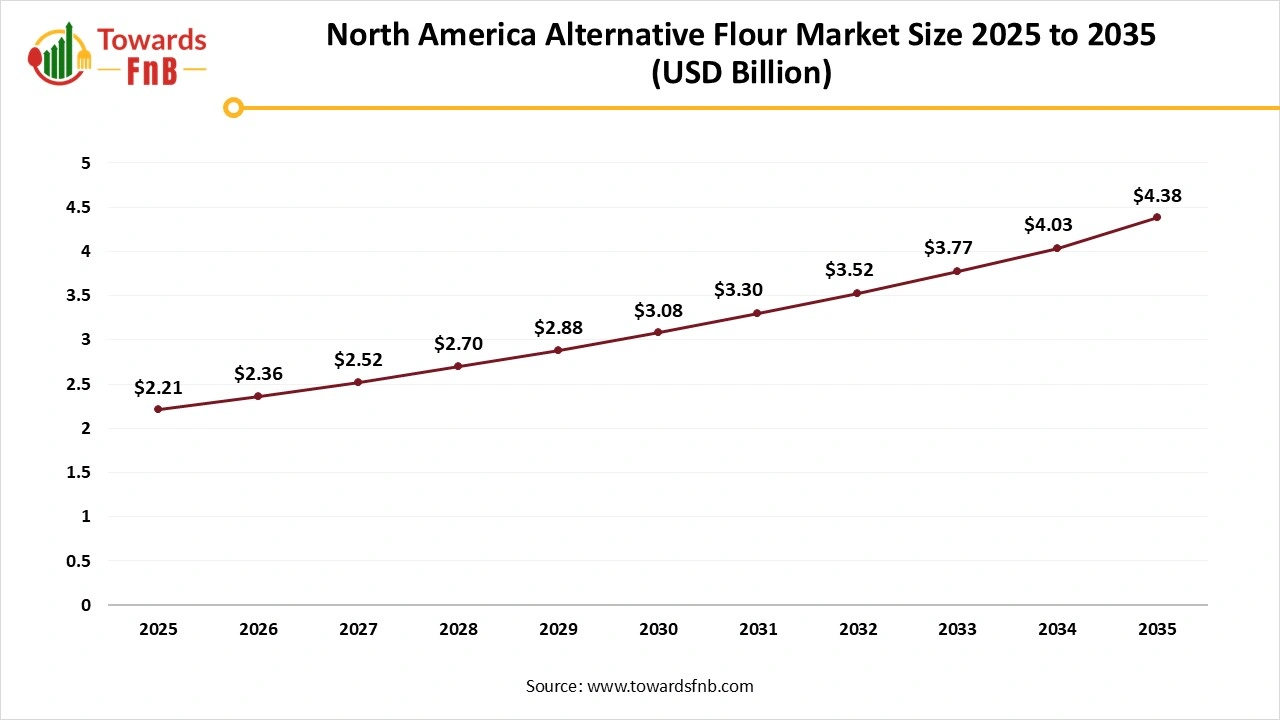

North America Alternative Flour Market Size and Growth 2025 to 2035

The North America alternative flour market size was valued at USD 2.21 billion in 2025 and is expected to grow steadily from USD 2.36 billion in 2026 to reach nearly USD 4.38 billion by 2035, with a CAGR of 7.08% during the forecast period from 2026 to 2035.

Canada Alternative Flour Market Trends

Alternative flour market in Canada is experiencing strong growth, driven by the growing demand from consumers for plant-based based organic, and gluten-free products. The growing popularity of flour made from quinoa, chickpeas, almonds, and oats in Canada is indicative of a trend toward nutrient-dense and allergy-friendly ingredients. Clean label products popularity and increased knowledge of gluten sensitivity and celiac disease have further sped up market growth. As dietary preferences change, local food brands are also experimenting with indigenous crops and ancient grains. A major factor in the recent rise in demand for alternative flours through physical and virtual retail channels has been the rise in home baking.

Asia Pacific Alternative Flour Market Trends

Asia Pacific expects significant growth in the market during the forecast period, driven by dietary trends toward nutrient-dense and gluten-free flours and growing health consciousness. Traditional use in regional cuisines and growing adherence to healthier eating practices are driving up demand for flours made from millets, rice, and pulses. Also, the number of food brands and startups in the area that promote local alternative grain flours is increasing.

")

Indian Alternative Flour Market Trends

The alternative flour market in India is witnessing rapid growth, driven by rising lifestyle-related illnesses, growing health consciousness, and a resurgence of interest in traditional grains. Because of their high nutrient profiles and gluten-free qualities, consumers are increasingly choosing flours made from chickpeas, amaranth, brown rice, and millets. Domestic consumption and awareness of millets have increased dramatically as a result of government initiatives to promote them as nutri cereals, particularly through the International Year of Millets 2023 campaign. The demand for value-added products and ready-to-use premix flour blends that fit their hectic schedules is also being driven by urban consumers. Alternative flours are now more widely available and accessible nationwide thanks to the growth of health food brands and e-commerce sites.

How did the Cereal-Based Flours Segment Dominate the Alternative Flour Market in 2025?

Cereal-based flours segment dominated the alternative flour market in 2025 because they're widely used in baking, food packaging, and daily cooking because of their familiarity affordability and ease of Flours like rice, corn, and millet are the go-to option for both home and commercial bakers. Their market dominance was further strengthened by their established distribution channels and inherent gluten-free status.

Legume-Based Flours Segment is Observed to Grow at the Fastest Rate During the Forecast Period

As customers look for high fiber, protein-rich substitutes. Lentils, peas, and chickpea flours are becoming increasingly popular in gluten-free baking as well as main ingredients in plant-based meat substitutes and snacks. They appeal to customers who are concerned about their health and the environment because of their nutritional profile and sustainability benefits.

Why did the Baker's & Confectionery Segment Dominate the Alternative Flour Market in 2025?

Bakers & confectionery segment held the dominating share of the alternative flour market in 2025, as alternative flours became widely accepted in cakes, cookies, pastries, and breads. The demand surged for gluten-free and low-carb baked goods made using almonds, coconut, oat, and millet flours. The availability of a broad range of products in both artisanal and packaged categories contributed to the segment's leading market position.

Meat Alternatives Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Since flours made from legumes and pulses are being used more because of their ability to improve texture and provide a high protein content. These flours are essential for creating plant-based meat substitutes, which fit in with the growing popularity of vegan and flexitarian diets. Constant advancements in food processing have increased their use in common meat alternatives.

Why did the Flour Segment Dominate the Alternative Flour Market in 2025?

Flour segment dominated the alternative flour market in 2025, owing to its wide availability and adaptability in various culinary applications. Consumers continue to favor raw flours for home cooking, baking, and customizing recipes based on dietary needs. The clean label appeal and ease of sourcing contribute to its commanding market share.

Premixed Flour Blends Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Driven by customer demand for time-saving and convenient solutions. These blends combine several different flours and suitable ingredients to provide a consistent taste and texture. They are frequently made for recipes, such as bread or pancakes. They are especially popular with busy city dwellers and inexperienced bakers.

Why did the Offline Retail Segment Dominated the Alternative Flour Market in 2025?

Offline retail segment held the largest share of the alternative flour market in 2025, as supermarkets, health food stores, and specialty retailers continue to be the primary purchase points. The ability to physically inspect products, access a wide variety of brands, and take advantage of in-store promotions contributed to strong sales through this channel.

Online Retail Segment is Expected to Grow at the Forecast CAGR During the Forecast Period

As more customers look to online retailers for health food items. Online shopping has become the go-to choice for alternative flour buyers due to the growth of digital grocery services, access to niche brands, and subscription-based products.

Nature’s Path

Bread Free

By Source

By Application

By Form

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Alternative Flour Market