April 2026

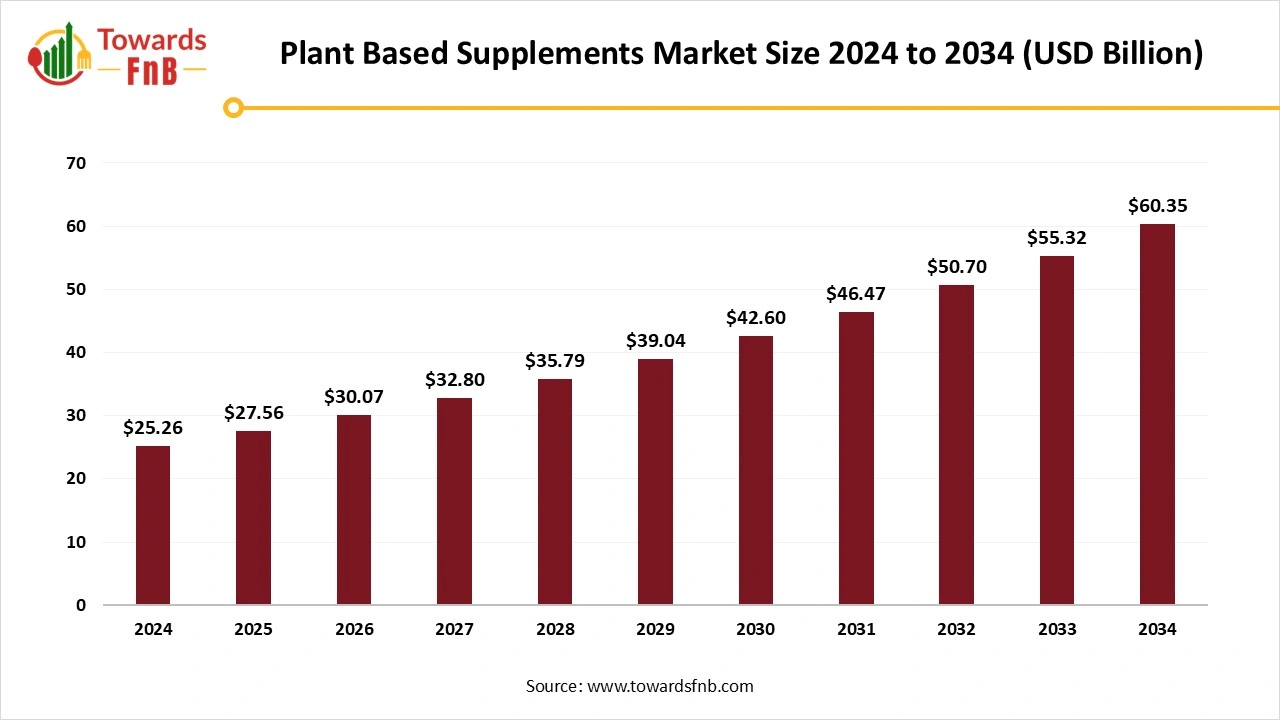

The global plant based supplements market size was valued at USD 25.26 billion in 2024 and is expected to grow steadily from USD 27.56 billion in 2025 to reach nearly USD 60.35 billion by 2034, with a CAGR of 9.1% during the forecast period from 2025 to 2034. With innovation expanding across beverages and personal care, plant-based alternatives are reshaping consumer expectations and product development across industries.

| Study Coverage | Details |

| Growth Rate from 2025 to 2034 | CAGR of 9.1% |

| Market Size in 2025 | USD 27.56 Billion |

| Market Size in 2026 | USD 30.07 Billion |

| Market Size by 2034 | USD 60.35 Billion |

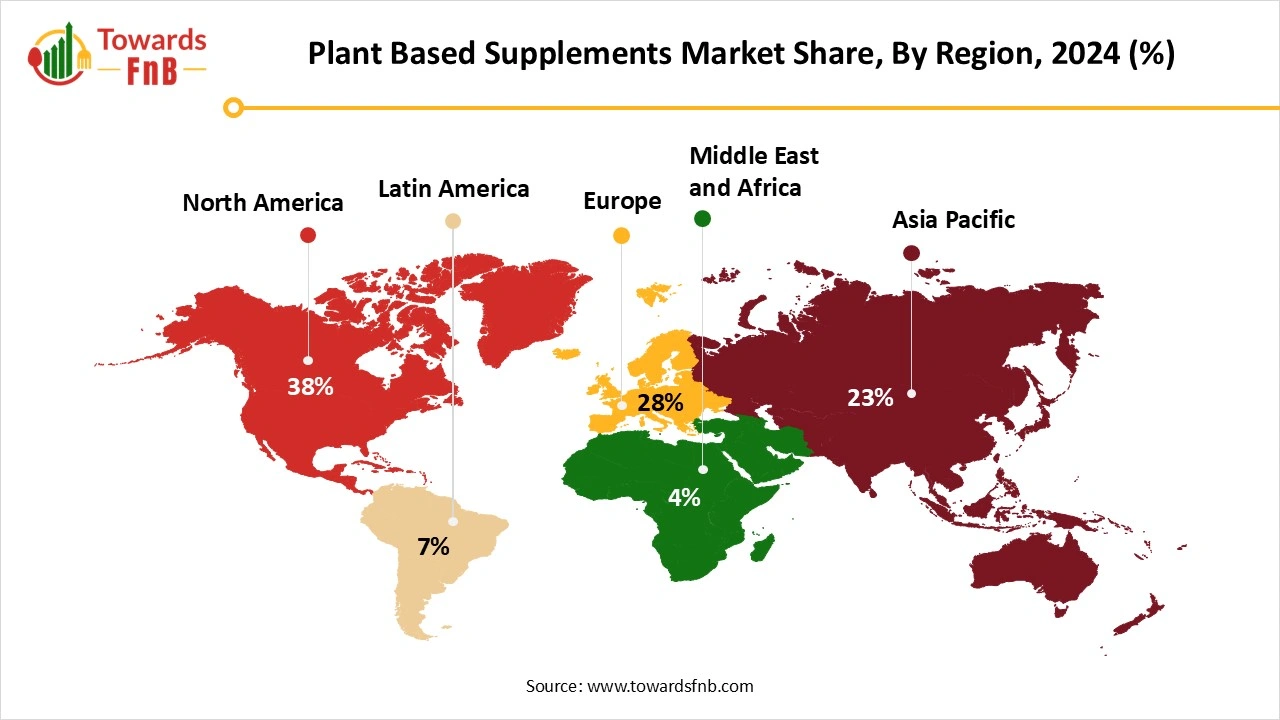

| Largest Market | North America |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The plant based supplements market includes the production, distribution, and consumption of dietary supplements derived entirely from botanical sources such as herbs, fruits, vegetables, roots, seeds, and algae. These supplements exclude animal-derived ingredients and are commonly offered in the form of capsules, powders, gummies, tinctures, or functional beverages. Increasing demand is driven by rising health consciousness, vegan/vegetarian lifestyles, clean label trends, and concerns over synthetic or animal-based ingredients. Applications span across immunity, digestion, weight management, mental health, beauty, and sports nutrition.

It is driven by shifting consumer values and advancements in food science. Once limited to soy milk and tofu, the category now spans alternative protein, vegan snacks, dairy-free desserts, and even plant-based seafood. Health-conscious consumers, flexitarians, and climate-aware millennials are fuelling demand for cleaner, greener food options. The market is also expanding beyond food into supplements, personal care, and textiles. Retailers and foodservice operators are dedicating more shelf space and menu options to plant-based products. As taste and texture parity with animal-based products improves, plant-based consumption is becoming a daily lifestyle choice rather than an occasional alternative.

Opportunities in the plant based supplements market extend far beyond meat and dairy substitutes. Emerging segments like seafood alternatives, high-protein plant snacks, and plant-based baby food are gaining traction. Functional plant-based products infused with vitamins, nootropics, or probiotics are opening up new wellness-oriented niches. Markets in Asia-Pacific, Latin America, and the Middle East are underpenetrated and represent strong potential for culturally adapted, locally sourced offerings. There's also an opportunity in ingredient innovation using jackfruit, mung beans, fava, lupin, and microalgae for differentiated product development.

Despite its momentum, the plant-based market faces several challenges that could impede growth. One major restraint is the perception of high cost, which discourages mass adoption in price-sensitive regions. Taste and texture, although improving, still lag behind conventional animal-based counterparts for many consumers.

Label complexity and ingredient unfamiliarity can also lead to skepticism, especially in emerging markets. Supply chain instability, particularly for crops like peas, almonds, and coconut, can create bottlenecks and price volatility. Nutritional equivalence and fortification remain concerns, especially in products targeting children and seniors. Additionally, regulatory scrutiny and debates around labeling are creating legal hurdles in certain geographies.

How is North America Being Plant-Based Powerhouse in the Market?

North America dominated the market in 2024, driven by advanced food innovation, high consumer awareness, and strong demand for clean-label product. The U.S. and Canada have witnessed widespread adoption of plant-based diets, supported by an expanding range of meat and dairy alternatives in mainstream retail. Celebrity endorsements, health documentaries, and plant-forward influencers have further fueled consumer interest. The government should support sustainable agriculture and nutrition transparency has also helped the category flourish. North American consumers and more willing to pay a premium for products with functional benefits, organic labels, and sustainability claims. Foodservice giants and QSR chains offering plant-based options have played a major role in normalizing consumption patterns.

")

The U.S. represents the dominance in North America; functional gummies and fortified snacks are gaining traction through e-commerce and wellness subscription platforms. Retailers are increasingly segmenting shelves with plant-based zones, making the category easier to discover and shop. The rise of flexitarians, choosing plant-based without going fully vegan, is a defining trend in North America's evolving food culture. Technological advancements in fermentation, cell-based processing, and ingredients extraction are further driving product innovation. With strong purchasing power and a mature regulatory ecosystem, North America in the global plant-based movement.

How Ancient Wisdom Meets Modern Wellness in Asia Pacific?

Asia Pacific fastest growing in the market in 2024, fueled by rising health consciousness, rapid urbanization, and deep-rooted plant-forward culinary traditions. Countries like India, China, Japan, and South Korea are witnessing surging demand for plant-based foods, beverages, and supplements. The prevalence of lactose intolerance in Asian populations has also driven the success of dairy-free and non-allergenic alternatives. Younger consumers in metropolitan areas are embracing plant-based diets not just for health, but also for ethical and environmental reasons. Plant-based innovation in Asia often blends traditional ingredients like turmeric, ginger, soy, and matcha with modern delivery formats. As disposable incomes rise and western wellness trends influence urban lifestyles, Asia-Pacific’s appetite for plant-based wellness is intensifying.

India is emerging as the key player in the Asia Pacific, and functional food formats such as ready-to-drink beverages, herb-infused teas, and holistic nutrition powders are becoming popular across the region. Supplements focused on beauty, from within, immunity, and digestive health are gaining traction among both men and women. Startups and legacy herbal brands alike are investing in DTC and e-commerce platforms to reach younger demographics. Governments in several countries are promoting local, plant-based sourcing as a part of food security and sustainability efforts. Cultural familiarity with herbal medicine and natural remedies offers a unique advantage in product adoption. With its mix of traditional health systems and modern wellness demand, Asia Pacific is poised to be the next global epicenter of plant-based innovation.

How Herbal/ Botanical Supplements Dominates the Plant Based Supplements Market in 2024?

The herbal/ botanical supplements dominated segment dominated the market in 2024, due to their long-standing integration in traditional health systems and growing clinical validation. Ingredients like ashwagandha, turmeric, ginseng, and elderberry are recognized for their adaptogenic, anti-inflammatory, and immune-modulating properties. Their versatility across health needs, stress relief, cognition, digestion, and hormonal balance has made them highly marketable. Consumers often view herbal supplements as safer, more natural alternatives to synthetic solutions. Their appeal extends across demographics, from millennials seeking energy and focus to seniors managing chronic wellness goals. Brand storytelling around heritage, sustainability, and efficacy further reinforces their stronghold.

The global resurgence of ayurveda, traditional Chinese medicine, and herbal wellness rituals has positioned botanicals at the forefront of holistic nutrition. Scientific advancements in standardization and extraction technologies have improved potency and formulation consistency. These supplements are now found in capsules, teas, tinctures, powder and functional beverages, broadening their consumer base. Clean-label preferences and minimal processing have made herbal products synonyms with trust and wellness. With regulatory approvals and consumer education improving globally, herbal botanical supplements continue to anchor the plant-based health movement. Their proven legacy and evolving formats make them the most resilient category in the market.

The Plant-Based Omega-3s Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

Driven by growing demand for sustainable, non-fish alternatives to traditional omega-3s. Sourced from algae, flaxseed, China, and walnuts, these supplements offer EPA and DHA benefits without the environmental toll of marine harvesting. Increased awareness of cardiovascular, cognitive, and inflammatory health benefits of omega-3s is accelerating adoption. As vegan and vegetarian lifestyles rise, plant-based omega solutions fill an essential nutritional gap. These products are also gaining popularity among pregnant women, athletes, and aging populations seeking joint and brain support. Their clean-label, mercury-free profile further boosts consumer trust.

Manufacturers are now focusing on enhancing the bioavailability of omega-3s through microencapsulation and emulsification techniques. Plant-based omega is also being incorporated into food products like milks, bars, and spreads, creating crossover appeal. Retailers are expanding shelf space for algal oil capsules and soft gels, especially in eco-conscious markets. Brands are emphasizing traceability and third-party testing to build confidence in performance. As plant-based omega sources offer comparable health outcomes to marine oils, they are gaining traction as mainstream alternatives. With sustainability concerns and dietary preferences aligning, this segment is poised for exponential growth.

How Fruits & Vegetables are Dominating the Plant Based Supplements Market in 2024?

The fruits & vegetables dominated segment dominated the market in 2024, due to their dense nutritional value and broad consumer acceptance. Packed with antioxidants, vitamins, fiber, and phytonutrients, these sources offer functional benefits for immunity, digestion, skin, and energy. Ingredients like beetroot, spinach, blueberries, and carrots are being integrated into everything from capsules to smoothies. Their versatility across product formats and health claims makes them a staple in formulations. Consumers strongly associate fruit and veggie-based products with real food and health authenticity. Additionally, their widespread cultivation ensures a relatively steady supply and competitive pricing.

Manufacturers are leveraging the appeal of whole-food derived nutrition to meet clean-label expectations. Freeze-dried powders, cold-pressed extracts, and concentrates are preserving nutrient integrity while allowing convenient delivery. These sources are also being fortified into kid-friendly and genetic nutrition products, expanding demographic reach. Fruits and vegetables are prominent in beauty from within offerings, often marketed for skin radiance and detoxification. Marketing messages around daily serving and plant-powered wellness resonate with mainstream audiences. As food-as-medicine gains traction, fruits and vegetables continue to be the dominant pillars of the plant-based revolution.

The Algae & Leafy Greens Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

Algae varieties like spirulina, chlorella, and marine microalgae are rich in protein, omega-3s, iron, and B12 key nutrients often deficient in vegan diets. Leafy greens like kale, moringa, and wheatgrass are also being used in immunity, detox, and energy formulations. These ingredients appeal to consumers seeking concentrated superfoods with minimal caloric load. Their eco-efficiency in terms of water, space, and carbon output also aligns with environmental concerns. As more research highlights their therapeutic potential, demand is quickly accelerating.

Innovations in algae cultivation and extraction have enabled scalable, flavor-neutral formats for food and supplement integration. Algae-derived protein and omega-3s are also being used in infant nutrition and elderly care formulations. Functional drinks, green powders, and daily shots with algae and leafy greens are gaining traction in wellness routines. High antioxidant and chlorophyll content positions them as detox and anti-inflammatory agents in natural health spaces. These sources are also gaining clinical interest for their role in cholesterol regulation and metabolic health. With high value in small doses, algae and greens are fast becoming the elite tier of plant-based ingredient sourcing.

Why Capsules & Tablets are Leading the League?

The capsules & tablets segment dominated the market in 2024, due to their precision, convenience, and long shelf life. These formats allow for controlled dosing, protection of sensitive ingredients, and consistent quality. Consumers trust capsules and tablets for serious, result-driven health outcomes like energy, hormone balance, and inflammation control. Their compact design makes them ideal for travel and discreet daily use. Brands are also offering plant-based capsules (vegan shells) to align with clean-label and cruelty-free preferences. The pharmaceutical-style format reinforces the credibility and perceived effectiveness of the products.

Innovations in time-release and dual-layer tablets are enhancing nutrient absorption and performance. Capsules remain the preferred choice for herbal blends and omega oils, while tablets dominate vitamin and mineral formulations. Consumers often view capsule and tablet supplements as more clinical, especially when supported by scientific claims. They are widely distributed through pharmacies, e-commerce, and DTC platforms due to ease of packaging and logistics. As multi-ingredient blends become common, these forms provide formulation flexibility. Their universal familiarity and efficiency keep them at the forefront of plant-based supplement delivery.

The Gummies Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

Originally popularized in the vitamin space, plant-based gummies now span adaptogens, nootropics, immunity boosters, and beauty supplements. Their candy-like texture and flavour reduce supplement fatigue and increase adherence. As more consumers seek enjoyable wellness routines, gummi offers a sweet spot between indulgence and health. Vegan gummy formulations using pectin instead of gelatin are expanding market reach to ethical and plant-based consumers. Their on-the-go convenience and bright branding resonate strongly with Gen Z and millennials.

Innovation is now focused on low-sugar, sugar-free, and functional ingredients enriched gummy formats. Brands are also exploring layered or dual-texture gummies for stress, sleep, gut, health, and cognitive support are becoming top sellers in both retail and online. Single-serve packaging supports portion control and freshness, especially for travel or busy lifestyles. With cross-generational appeal and growing shelf presence, gummies are evolving into a serious supplement category. As health merges with the secondary supplement category. As health merges with sensory pleasure, gummy formats are well-positioned for explosive growth.

Why General Health & Wellness Dominate the Plant Based Supplements Market in 2024?

The general health & wellness segment dominated the market in 2024, with products designed for stress management, energy, digestion, and metabolic balance are widely adopted. These formulations often include a blend of botanicals, vitamins, and adaptogens for a broad-spectrum effect. Consumers prefer multi-benefit supplements that address core well-being rather than isolated conditions. Brands are marketing everyday wellness solutions as part of lifestyle integration, not just reactive healthcare. This university makes general wellness the largest and most inclusive category.

General health products are frequently bundled in subscription packs or daily sachets, boosting consistency and consumer retention. Market leaders are formulating products based on trending health goals like gut health, detox, and hormonal balance. Cross-functionality, such as immunity and energy or sleep and mood, is enhancing appeal. This category attracts the widest demographic reach, from young professionals to aging populations. General wellness products are also less likely to trigger regulatory barriers, allowing for faster global expansion. As preventive health becomes a priority, general wellness remains the cornerstone.

The Immunity Support Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

Driven by heightened global health awareness and post-pandemic behavior. Consumers are proactively turning to plant-based formulations with ingredients like echinacea, elderberry, zinc, and vitamin C. Mushroom-based immunity blends are also gaining significant momentum. Immunity support now goes beyond cold and flu defense its about enhancing long-term resilience. These products are positioned for daily use rather than seasonal spikes, reflecting a shift to sustained immune optimization. Their perceived safety and natural origin make them ideal for families and sensitive groups.

Immunity products are being delivered in formats like shots, lozenges, chewable, and fortified drinks for variety and convenience. Companies are also blending immunity with other functions like energy or gut health to appeal to wellness multitaskers. Plant-based immunity brands are using bold claims and science-backed transparency to build trust. Functional ingredients with anti-inflammatory and antimicrobial properties are especially popular. Retail and e-commerce platforms are highlighting this category through curated immunity sections. As immune health continues to anchor preventive wellness, plant-based solutions will dominate this evolving segment.

Why Adult is Leading the League?

The adult segment dominated the market in 2024, driven by increased health consciousness and lifestyle shifts toward sustainability. Whether targeting stress, digestion, metabolism, or sleep, plant-based solutions are addressing a wide range of adult wellness concerns. Adults are the most consistent buyers of supplements, with strong brand loyalty and interest in clinical validation. The rise of workplace wellness, digital health tools, and functional nutrition has made daily supplementation the norm. Adults are also more likely to make value-driven decisions, choosing products with clean labels and traceable ingredients. Their consistent purchasing power makes them the cornerstone of the market.

Adult-focused products span diverse forms capsules, powders, shots, and fortified snacks, tailored to busy, modern lifestyles. Targeted campaigns around energy, hormonal balance, and aging support are resonating deeply. Adults are also increasingly turning to preventive care instead of reactive solutions, aligning with the ethos of plant-based nutrition. The growth of DTC platforms and personalized health apps is supporting deeper engagement with this segment. Brands also addressing sub-groups such as working professionals, parents, and caregivers with specialized messaging. With the widest functional demand and steady purchasing behavior, adults remain the driving force behind market momentum.

The Athletes & Fitness Enthusiasts Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

Seeking plant-based products that enhance performance and recovery. Protein powders, hydration mixes, joint support capsules, and energy-boosting adaptogens are in high demand. This segment values clean-label, allergen-free, and non-GMO credentials, especially among vegan and flexitarian athletes. Plant-based products are increasingly viewed as effective alternatives to whey and animal-based performance aids. Consumers are also driven by inflammation reduction, muscle repair, and endurance support from natural sources. Influencer marketing and fitness-centric branding are accelerating adoption in this space. Brands are developing specialized SKUs tailored to pre-workout, intra-workout, and recovery phases.

Ingredients like beetroot, turmeric, and BCAAs are commonly featured. Plant-based products are also entering sports drinks, snack bars, and creatine alternatives. Fitness-focused consumers are tech-savvy and often track results, creating opportunities for measurable outcomes. Subscription-based models and gym partnerships are expanding market access. As fitness merges with holistic wellness, this segment is quickly becoming one of the most dynamic drivers in the plant-based market.

Why did the Distribution Channel Segment Dominated the Plant Based Supplements Market in 2024?

The online retail segment dominated the market in 2024, primarily due to its unparalleled convenience. Consumers appreciated the ability to shop from the comfort of their homes, which saved time and effort. A vast product variety was available on e-commerce platforms, catering to diverse customer needs and preferences. Access to global brands became more seamless, allowing consumers to purchase internationally with ease. The user-friendly interfaces and secure payment options further boosted customer confidence and loyalty. Overall, the online retail segment continued to expand its market share, shaping the future of shopping.

The Direct-to-Consumer (DTC)/E-commerce Segment Expects the Fastest Growth in the Plant Based Supplements Market During the Forecast Period.

These platforms allow startups to build niche audiences with personalized wellness solutions and flexible purchasing models. DTC enables richer brand-consumer relationships through email marketing, AI-driven curation, and loyalty incentives. Many DTC platforms offer personalized quizzes or telehealth tie-ins to match users with products that suit their needs. Brands are using clean aesthetics, minimalist branding, and mission-driven messaging to connect emotionally with customers. Social media integration allows rapid feedback and real-time management.

Eat Just

Tom Brady

By Product Type

By Source

By Form

By Function

By End-User

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

March 2026

February 2026

Plant Based Supplements Market