April 2026

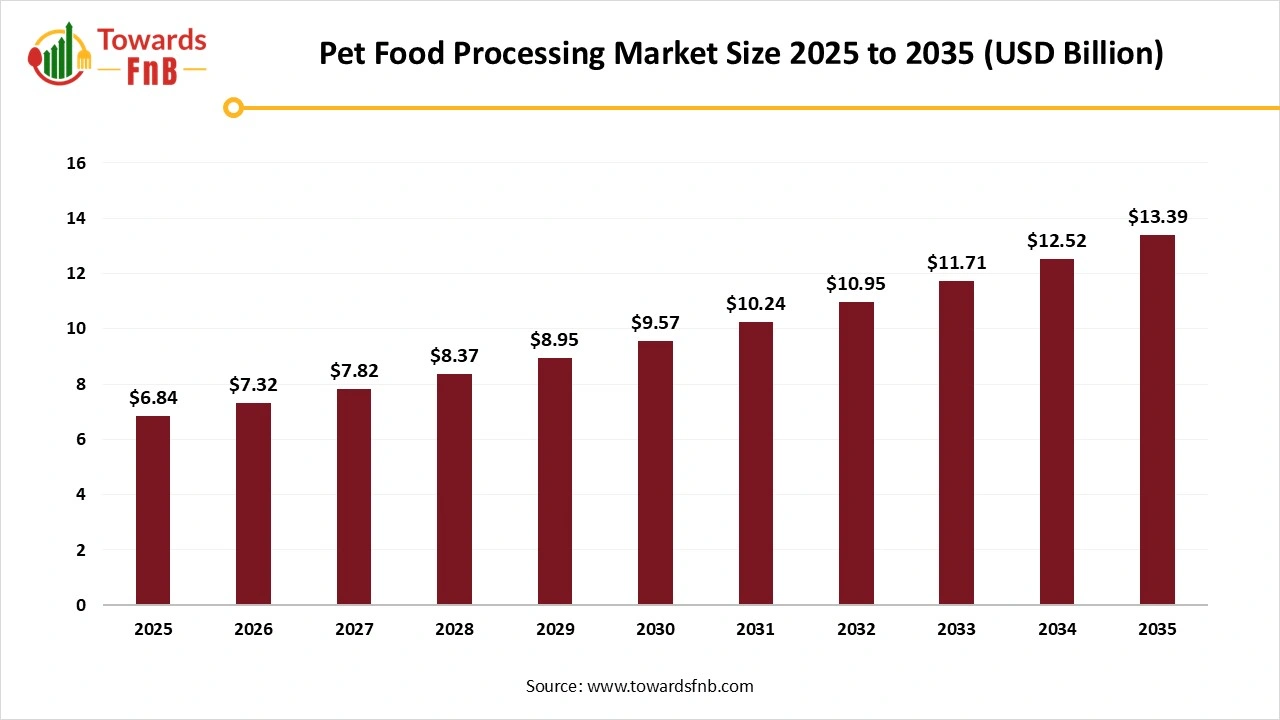

The global pet food processing market size stood at USD 6.84 billion in 2025 and is predicted to increase from USD 7.32 billion in 2026 to approximately USD 13.39 billion by 2035, expanding at a CAGR of 6.95% from 2026 to 2035. The growing demand for nutritious pet food and pet food premiumization drives market growth.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 6.95% |

| Market Size in 2026 | USD 7.32 Billion |

| Market Size in 2027 | USD 7.82 Billion |

| Market Size by 2035 | USD 13.39 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The pet food processing market refers to the process of converting raw materials into nutritious pet food products. It includes stages like preparation of ingredients, milling of ingredients, mixing, extrusion, retorting, drying of extruded kibbles, palatability optimization, and quality control. Its applications are wet food processing, fresh meat processing, kibble production, and coating enhancement. It offers benefits, such as enhancing nutritional availability, extended shelf life, sustainability, enhancing safety, precise formulation of nutrients, and improved texture. Pet food processing includes equipment like grinders, dryers, sterilization retorts, extruders, mixers, vacuum coaters, pre-breakers, material packaging, and coolers.

The pet food processing industry growth is driven by the development of high-quality pet food, increased pet health awareness, surging pet ownership, increased use of advanced technology, popularity of eco-friendly pet products, production of grain-free formulation, shift to advanced machinery, expansion of online retail, and the development of safe food.

The pet food processing industry is witnessing key technological shifts like the integration of machine learning, smart sensors, automation, smart packaging, digital twin, and robotics. Technological shifts are driven by demand for ingredient integrity, optimizing production, sustainability, and precision nutrition. The incorporation of artificial intelligence (AI) technology is a robust shift in the market, driven by demand for product personalization and optimizing formulation.

AI optimizes the equipment settings and identifies product defects. AI manufactures tailored pet recipes and prevents unexpected equipment failures. It optimizes the distribution of products and suggests customized products. AI lowers the rework and supports faster inspection. AI analyzes the availability of raw material and prevents stockouts. It also supports nutritional research and making operational decisions. Overall, AI enhances consumer trust and lowers operational costs.

Raw Material Procurement

Processing and Preservation

Quality Testing and Certifications

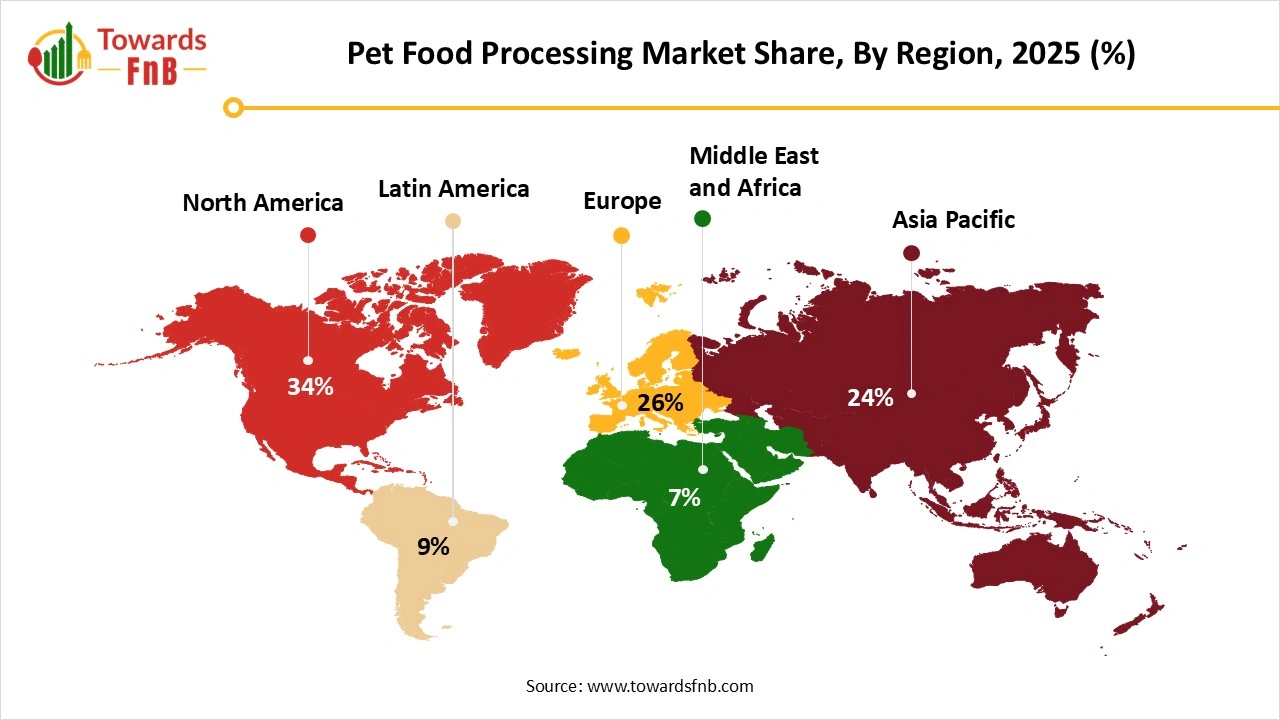

How did North America Dominate the Pet Food Processing Market?

North America held a major market share of 34% in 2025, due to the high rate of pet ownership. The growing demand for grain-free pet food and the high expenditure on pets increase the adoption of pet food processing. Regulations for pet food safety and the development of customized pet foods increase the adoption of pet food processing. Advanced pet food processing capabilities and the strong digital base drive the overall market growth.

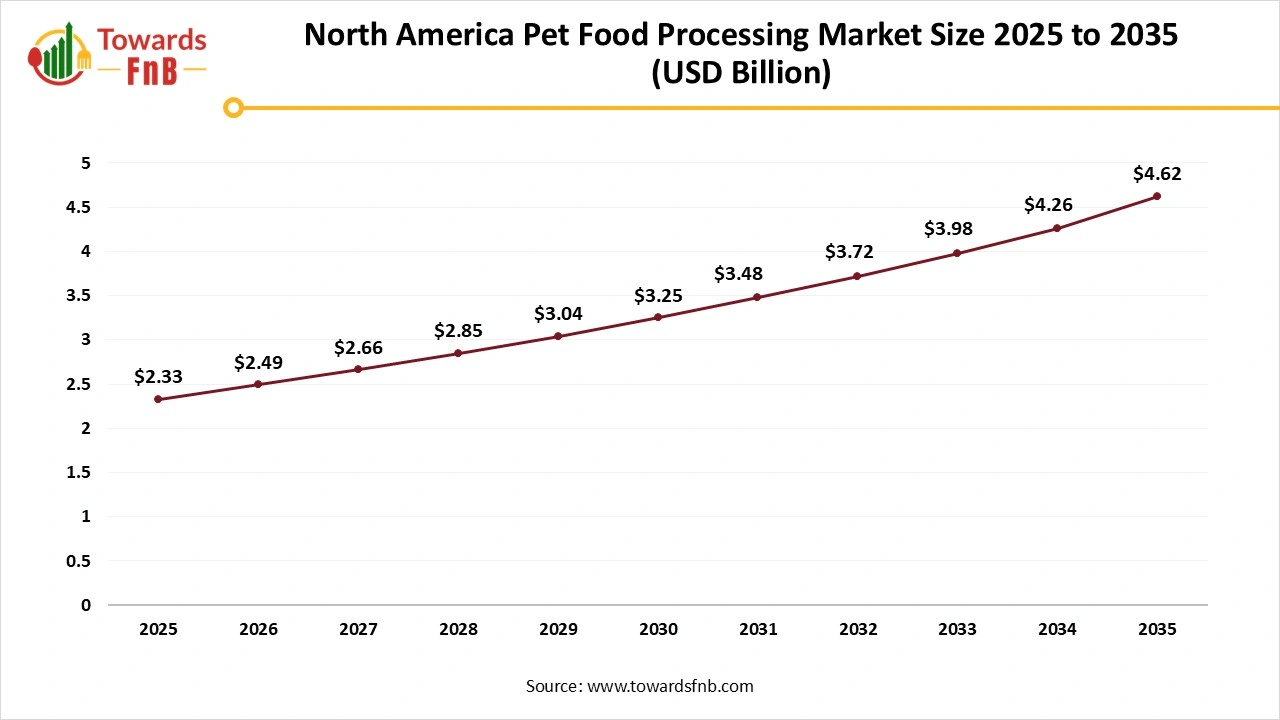

North America Pet Food Processing Market Size and Growth 2025 to 2035

The North America pet food processing market size was valued at USD 2.33 billion in 2025 and is predicted to grow from USD 2.49 billion in 2026 to hit around USD 4.62 billion by 2035, expanding at a CAGR of 7.08% from 2026 to 2035.

United States Role in Pet Food Processing

The United States is a prominent player in the market due to the premiumization of pet food. The strong focus on ingredient transparency and the development of specialized pet treats increases pet food processing. The huge consumption of dry pet food helps with expansion. The presence of key players like Hill’s Pet Nutrition, Mars Petcare, and Nestle Purina Petcare supports market growth.

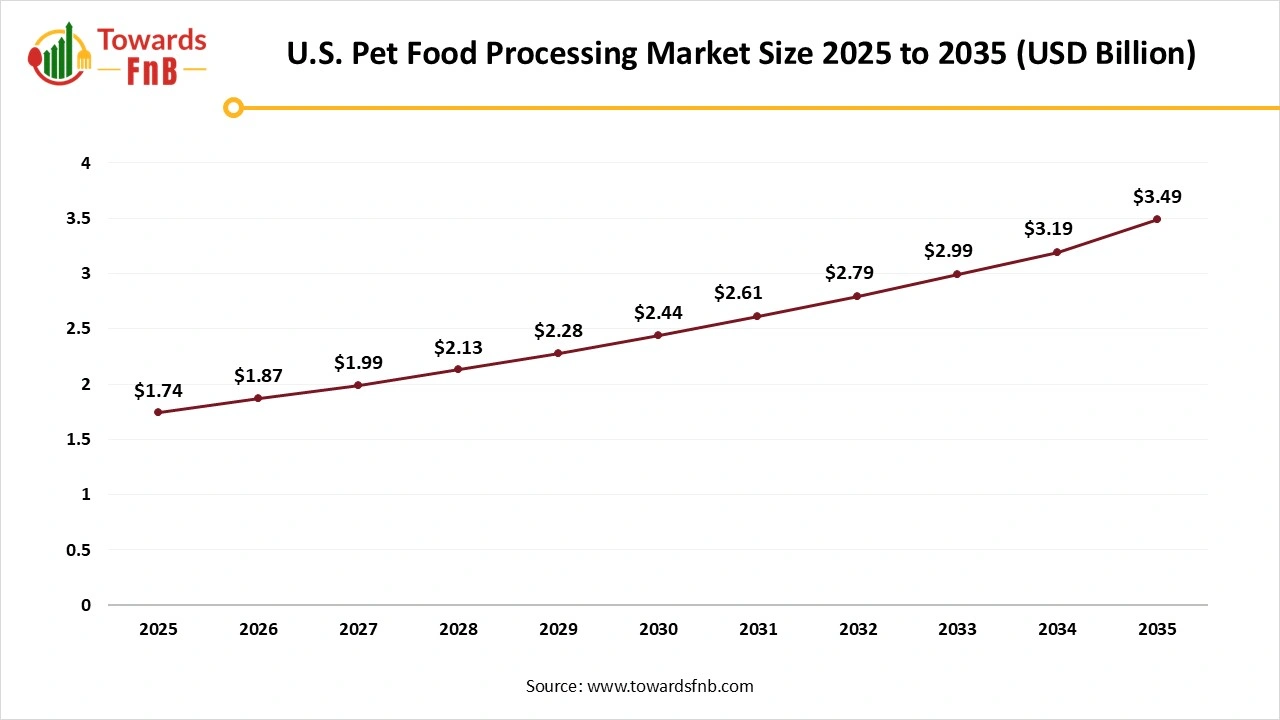

U.S. Pet Food Processing Market Size and Growth 2025 to 2035

The U.S. pet food processing market size was calculated at USD 1.74 billion in 2025 and is predicted to grow from USD 1.87 billion in 2026 to hit around USD 3.49 billion by 2035, expanding at a CAGR of 7.21% from 2026 to 2035.

How is Asia-Pacific Growing in the Pet Food Processing Market?

Asia-Pacific is expected to experience the fastest growth with a CAGR of 8.1% during the predicted timeframe, due to the growing pet adoption in middle-class demographics. The preference for high-quality pet products and the increased seeking of small pets increases demand for pet food processing. The focus on specialized pet nutrition and the expansion of wet food increases demand for pet food processing. The increased companionship with pets drives the market growth.

")

Japan’s Contribution to Pet Food Processing

Japan is substantially growing in the market. The growing demand for nutrition in older pets and the increased purchasing of high-quality ingredients increase demand for pet food processing. The surging number of single-person households and the focus on pet living longer increase the adoption of pet food processing. The focus on quality assurance of locally produced pet food supports the overall market growth.

The Extrusion Equipment Segment Dominated the Market with 26% of Market Share in 2025

The extrusion equipment segment dominated the pet food processing market with a 26% share in 2025 and is expected to grow at the fastest CAGR of 7.8% during the forecast period due to the increased manufacturing of kibble-based pet food. The need to increase starch gelatinization and the development of semi-moist foods increases the adoption of extrusion equipment. The excellent nutrient digestibility, high safety, excellent operational efficiency, and short-time processing of extrusion equipment drive the segment’s growth.

The mixing and blending equipment segment held the second-largest market share of 18% in 2025, due to a strong focus on uniform ingredient distribution. The demand for high-protein diets and the development of homogenous wet food batches increase demand for mixing & blending equipment. Reduced product damage, contamination control, and product consistency in mixing & blending equipment boost the segment’s growth.

The grinding and milling equipment segment held the third-largest market share of 14% in 2025 due to the rising demand for fine particle size food. The development of consistent texture pet food and the preparation of raw materials increases the use of grinding & milling equipment. The increased use of automated grinding equipment and the increased dry kibble production support the segment’s growth.

The drying and cooling equipment segment held the fourth-largest market share of 12% in 2025 due to the need for moisture control. The increased use of air-drying increases demand. The popularity of multi-stage drying helps with expansion. The spending on energy-efficient drying systems and the development of automated cooling systems support segment growth.

The Dogs Segment Led the Market with 48% of Market Share in 2025

The dogs segment led the pet food processing market with a share of 48% in 2025 due to the growing trend of premium dog food. The massive dog population and the rise of premiumization of dog foods increase demand for pet food processing. The high availability of the wet food product range and the robust growth in dog food production drive the segment growth.

The cats segment held the second-largest market share of 32% in the market in 2025 and is expected to grow at the fastest CAGR of 7.2% during the forecast period due to the increased adoption of cats in urban areas. The requirement of less maintenance and the growth of feline favoritism increase the demand. The increased buying of premium kibble for cats and accessibility to imported cat foods boost segment growth.

The fish segment held the third-largest market share of 8% in 2025 due to the expansion of the aquarium hobby. The robustly growing specialized treats sector and owners seeking premium options help with expansion. Healthy development and nutritional feed needs for fish support the overall growth of the segment.

The birds segment held the fourth-largest market share of 6% in 2025 due to the increased ownership of pet birds. The humanization of birds and certain dietary requirements of birds increase demand for pet food processing. The high spending of the middle class on bird's premium products and the expansion of seed processing technology boost segment growth.

The Dry Food Segment Held the Largest Market Share of 44% in 2025

The dry food segment held the largest revenue share of 44% in the pet food processing market in 2025 due to the availability of dry processing equipment and high shelf life. The strong focus on lowering plaque in pets and the preference for easy-to-manage feed increase the adoption of dry food. The lower price, convenience, efficient production, easy logistics, and functional benefits of dry food drive the segment growth.

The wet food segment held the second-largest market share of 26% in the market in 2025 and is expected to grow at the fastest CAGR of 7.3% during the forecast period due to the consumption of high-moisture diets. The development of human-grade pet options and the preference for pet hydration increase demand for wet food. The improved palatability and the availability of wet food in single-serve trays boost segment growth.

The treats and snacks segment held the third-largest market share of 12% in 2025 due to the ongoing innovations in functional treats. The rise in the use of gourmet ingredients and the huge pet care expenditure increases the adoption of treats & snacks. The demand for immunity boosters and the surging training culture increases the adoption of treats & snacks, supporting segment growth.

The semi-moist food segment held the fourth-largest market share of 10% in 2025 due to its balanced taste and convenience. The huge adoption of functional ingredients and longer shelf stability increases demand for semi-moist food. The efficient production technology for semi-moist food and innovations in preservation boost segment growth.

The Thermal Processing Segment Led the Market with a 58% of Market Share in 2025

The thermal processing segment led the pet food processing market with a 58% share in 2025 due to the growing use in baking processes. The high safety standards and the focus on retaining nutritional value increase the adoption of thermal processing. The high-volume pet food manufacturing and the development of moist chunks use thermal processing. The improved digestibility and shelf stability of pet food manufactured using thermal processing drives segment growth.

The cold processing segment held the second-largest market share of 24% in 2025 and is expected to grow at the fastest CAGR of 7.4% during the forecast period due to the huge consumption of minimally processed food. The popularity of raw pet food and the need to maintain nutritional integrity increase the use of cold processing. The extensive consumption of freeze-dried products and focus on quality over convenience requires cold processing. The excellent sustainability and nutritional retention of cold processing drive segment growth.

The advanced processing segment held the third-largest market share of 18% in 2025 due to the surging innovations in HPP. The development of organic pet food and the increased use of advanced coatings increase the adoption of advanced processing. The popularity of energy-efficient extrusion technology increases demand. The demand for premium products and the development of specialized textures require cold processing, boosting overall segment growth.

The Fully Automated Segment Contributed the Highest Market Share of 40% in 2025

The fully automated segment contributed the biggest revenue share of 40% in the pet food processing market in 2025 and is expected to grow rapidly with a CAGR of 7.8% during the forecast period due to the presence of smart factories. Complex cooking formulations and a strong focus on labor reduction increase demand for a fully automated level. Small-batch pet food production and the focus on end-to-end traceability increase the adoption of a fully automated level. The integration of the fully automated level with AI drives segment growth.

The semi-automated segment held the second-largest market share of 38% in 2025 due to the transition towards automation. The lower upfront investment and quick changeovers in a semi-automated system increase demand. The simplified maintenance, improved safety, product variety, and higher quality standards of the semi-automated system drive the segment growth.

The manual processing segment held the third-largest market share of 22% in 2025 due to the increased use in small-scale manufacturing. The production of limited-ingredient diets and the growth of niche brands increase the adoption of manual processing. The low capital investment and quality control in manual processing boost segment growth.

The Commercial Manufacturers Segment Dominated the Market with 62% of Market Share in 2025

The commercial manufacturers segment held a dominant revenue share of 62% in the pet food processing market in 2025 due to the expansion of global brands. Consistent pet food production and innovations in safe products increase the adoption of commercial manufacturers. Advancements in pet nutrition and the need for large-scale logistics increase the use of commercial manufacturers. The use of large-scale extrusion and tailored product options drives segment growth.

The private label manufacturers segment held the second-largest market share of 20% in 2025 and is expected to grow at the highest CAGR of 7.2% during the forecast period due to the growing expansion of private labels in retail stores. The lower price point and high-quality ingredients boost demand. The rise of launching retailers' pet food brands and the customized packaging of private labels support segment growth.

The contract manufacturers segment held the third-largest market share of 18% in 2025 due to rising startups. The demand for hygienic production and the scaling up of production requires contract manufacturers. The use of advanced extrusion fuels demand. The manufacturing flexibility and globalized supply chains support segment growth.

Purina

ORIJEN

FAMSUN

By Equipment Type

By Pet Type

By Food Type

By Processing Technology

By Automation Level

By End-User

By Distribution Channel (Equipment Sales)

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Pet Food Processing Market