April 2026

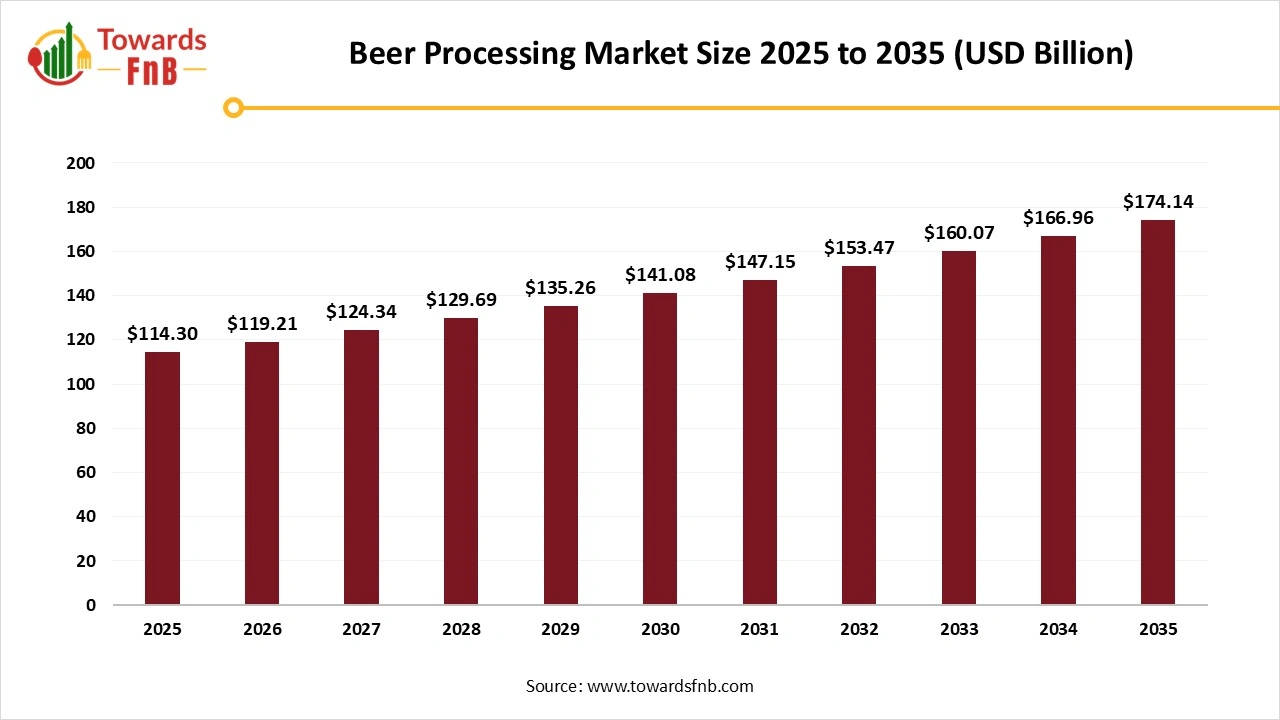

The global beer processing market size estimated at USD 114.30 billion in 2025 and is predicted to increase from USD 119.21 billion in 2026 to reach approximately USD 174.14 billion by 2035, expanding at a CAGR of 4.3% from 2025 to 2035. The market is primarily driven by rising consumer demand and demographic shift, the adoption of new brewing technologies, and the expansion of the middle-income population in emerging markets.

| Study Coverage | Details |

| Growth Rate from 2025 to 2035 | CAGR of 4.3% |

| Market Size in 2026 | USD 119.21 Billion |

| Market Size in 2027 | USD 124.34 Billion |

| Market Size by 2035 | USD 174.14 Billion |

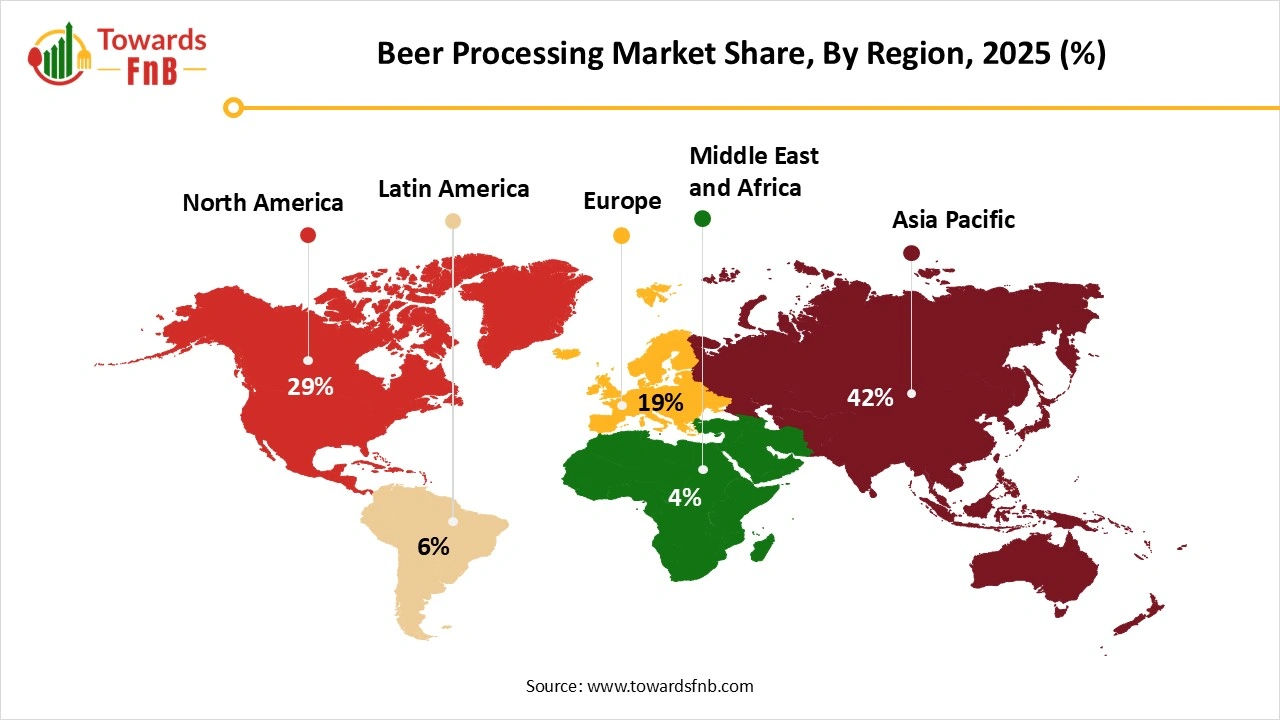

| Largest Market | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The beer processing market encompasses industrial activities involved in transforming raw ingredients malted barley, hops, yeast, and water, into finished alcohol beverages through stages, such as brewing, fermentation, maturation, and packaging. The primary benefits of this market include generating immense economic value globally and producing a stable, safe, and diverse range of products that cater to varied consumer performance and social occasions.

Breweries are increasingly implementing fully automated systems, from raw materials handling to packaging lines, using sensors and programmable logic controllers for precision control. IoT sensors are integrated throughout the entire production process to collect real-time data on critical parameters like temperature, pressure, and pH levels during mashing, fermentation, and maturation. AI algorithms are used for various applications, from optimizing energy consumption and predicting maintenance needs to developing new recipes based on consumer feedback and market trends. An advanced processing and filtration system, and supply chain traceability.

Key Players: Cargill, Incorporated, Rahr Malting Company (RahrBSG), Lallemand Inc. (yeast), and John I. Haas (hops), Anheuser-Busch InBev, and Heineken N.V.

Key Players: Anheuser-Busch InBev, Carlsberg Group, Sierra Nevada Brewing Co., and The Boston Beer Company, Inc.

Key Players: AB InBev, Molson Coors Beverage Company, and Diageo plc

Key Players: AB InBev, Heineken, and Carlsberg

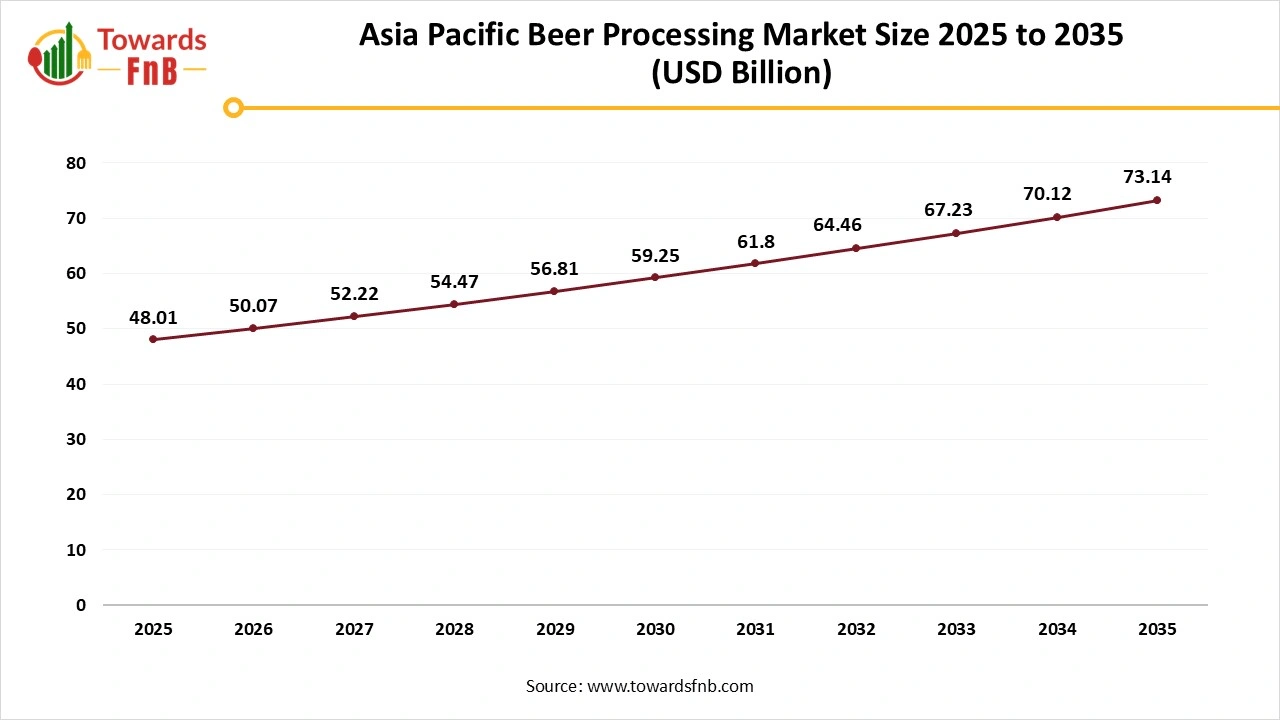

Why did Asia Pacific Dominate the Beer Processing Market?

Asia Pacific dominated the market in 2025, With its enormous population base, particularly in China and India, which drives immense consumption volumes. Rapid economic growth and rising disposable incomes have led to an expanding middle class willing to spend on both mass-market lagers and premium, specialty brands. Rapid urbanization and changing lifestyles further contribute to increased social drinking in on-trade channels. The combination of a massive consumer base, economic prosperity, and strong domestic production infrastructure ensures the region maintains its leading market position.

The Asia Pacific beer processing market size was valued at USD 48.01 billion in 2025 and is expected to grow steadily from USD 50.07 billion in 2026 to reach nearly USD 73.14 billion by 2035, with a CAGR of 4.3% during the forecast period from 2026 to 2035.

India Beer Processing Market Analysis

The significant premiumization and the booming growth of craft breweries that offer diverse, unique flavors. Although strong beer dominates the market, there is a nascent but growing interest in healthier, non-alcoholic options. The market is embracing technological adoption in brewing and capitalizing on the rise of e-commerce for better accessibility, despite navigating a complex regulatory landscape and high taxation.

North America is the Fastest-Growing Beer Processing Market

North America fastest growth in the market in 2025, propelled by the United States’ immense and innovative craft brewing culture. High disposable incomes fuel the premiumization trend, as consumers willingly pay more for quality, unique, and authentic beer experiences. The region benefits from advanced technology and highly efficient, extensive distribution networks, allowing producers to meet rapidly evolving consumer demand for diverse options, including no/low-alcohol and organic choices.

U.S. Beer Processing Market

The beer processing market is shifting towards premium, high-quality, and NOLO beers. Technological integration, including AI and IoT in brewing, is optimizing efficiency and sustainability efforts. Furthermore, shifting distribution channels, particularly the rise of e-commerce and taproom sales, are altering how breweries reach consumers.

")

Europe's Beer Processing Market: Rise of NOLD Beers and Technological Integration

Europe has a massive rise in the craft beer segment and the expansion of high-quality non-alcoholic and low-alcohol (NOLO) options, driven by health-conscious consumers. Brewers are increasingly adopting advanced technologies like AI and IoT for efficiency and product consistency.

Germany's Beer Processing Market Analysis

The German market for beer processing is a notable and expanding segment within Europe, driven by the premiumization, with consumers willing to pay more for quality, craft, and specialty options beyond the traditional Reinheitsgebot styles. Brewers are adopting advanced technology and sustainable practices to manage rising costs and meet environmental demands. Despite declining overall alcohol consumption, these trends in innovation, quality, and NOLO alternatives present key growth areas for the German market.

Growing MEA Beer Processing Market

The beer processing market in the Middle East and Africa (MEA) is driven by a young population and rising disposable incomes. The non-alcoholic (NOLO) beer segment is a major growth area in the Middle East due to cultural factors, while premiumization and the rise of craft breweries are key trends across Africa. Brewers are leveraging local ingredients like sorghum and expanding e-commerce channels to navigate the region's diverse regulatory landscape and meet growing consumer demand.

UAE Beer Processing Market Analysis

In the UAE, the beer processing market is driven by significant growth in the non-alcoholic segment due to health and cultural factors, alongside a strong demand for premium international and emerging craft beers. The market is also capitalizing on e-commerce growth and the integration of beer with the premium hospitality and tourism sectors. These dynamics foster a quality-driven and innovative market landscape.

South America Beer Processing Market Potential

The market for beer processing in South America is a swiftly expanding industry, driven by the expansion of craft beer and microbreweries across the region, rising demand for premium and super-premium brands, and increasing demand for specialty, flavoured, and better-for-you options. Expansion of on-trade and draught systems and growth in e-commerce.

Brazilian Beer Processing Market Analysis

As the Brazilian beer processing market is driven by a significant surge in non-alcoholic (NOLO) options, health and wellness trends influence consumer choices. The growth of e-commerce platforms and a vibrant on-trade culture further enhances accessibility and distribution channels.

Beer Processing Market Share, By Raw Material Type, 2025 (%)

| Segments | Shares (%) |

| Malt | 55% |

| Hops | 25% |

| Yeast | 12% |

| Water | 8% |

Why did Malt Segment Dominate the Beer Processing Market?

The malt segment led the beer processing market in 2025, due to the most crucial function of the malt is to provide the carbohydrates and sugars necessary for the yeast to perform fermentation, which produces alcohol and carbon dioxide. Without malt, the fundamental chemical reactions that create beer cannot occur in the traditional brewing process. Core of flavour and aroma profiles, color and body contribution, their health and nutritional properties, and high-volume requirement.

The Hops Segment is Observed to Grow at the Fastest Rate During the Forecast Period.

The enduring global popularity of craft beer, particularly hop-forward styles like IPAs. The shift reflects a change in consumer preferences, moving from simple bitterness to demand for intense fruity, citrusy, and aromatic flavour profiles provided by specialty hops.

The yeast segment is also notable growth due to technological innovation and the increase in the demand for craft and non-alcoholic beers. Advanced genetic engineering and hybridization methods are enabling the creation of novel yeast strains that produce specific flavour profiles for specialty beers. For non-alcoholic and low-alcohol beverages, specialized yeast strains are being developed to ferment at lower alcohol levels while retaining desirable aromas.

Why did the Brewing Segment Dominate the Beer Processing Market?

The brewing segment held the dominating share of the market in 2025. The brewing segment requires significant investment in heavy machinery and equipment, such as mash kettles, lauter tuns, wort kettles, and steam generators. Brewing requires foundational and critical steps, an impact on product quality and consistency, and continuous innovation in brewing techniques.

The Filtration Segment is Seen to Fastest Growth During the Predicted Timeframe.

Because rapid technological innovation and a strong focus on sustainability. The shift from hazardous diatomaceous earth to eco-friendly membrane and cross-flow filtration systems addresses environmental concerns while enhancing efficiency. Furthermore, consumer demand for aesthetically clear beers with extended shelf lives necessitates superior filtration technology.

The maturation segment is notable growth in the forecast period, due to increasing consumer demand for premium and super-premium beers that require refined aging processes. Investment in advanced technologies like IoT sensors and automated systems ensures optimal flavour development, clarity, and product consistency. Technologies such as barrel-aging cater to consumers seeking complex and unique flavour profiles, pushing breweries to invest further in specialized equipment.

Beer Processing Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Lager | 50% |

| Ale | 30% |

| Stout | 10% |

| Porter | 6% |

| IPA | 4% |

How did the Lager Segment Dominate the Beer Processing Market?

The lager segment dominated the market with the largest share in 2025, with the adoption of modern trends, with major brands and craft breweries introducing new variations, including premium lagers, low-calorie options, and non-alcoholic versions that cater to health-conscious consumers and evolving lifestyles. The historical and cultural significance, affordability and availability, and mass production efficiency.

The Ale Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period.

With the global craft beer revolution and a significant shift in consumer preferences towards unique, bold, and experimental flavour profiles. Ale yeasts are ideal for smaller-batch, high-turnover production cycles, making them perfectly suited for the agile operations of craft breweries. Innovation within the ale category, including flavorful non-alcoholic options and niche styles like hazy IPAs, meets consumer demand for variety, quality, and healthier choices.

The stout segment is expanding significantly during the forecast period, because craft beer revolution and consumer demand for complex, premium flavours like coffee, chocolate, and barrel-aged notes. Brewers are innovating with specialty additives and barrel-aging to offer unique, high-quality products that command premium prices. Shifting demographics, particularly traditional seasonal consumption. Furthermore, packaging innovations, such as nitrogen-infused cans, and the introduction of non-alcoholic variants are enhancing accessibility and appealing to health-conscious consumers.

Beer Processing Market Share, By Packaging Format, 2025 (%)

| Segments | Shares (%) |

| Kegs | 45% |

| Cans | 30% |

| Bottles | 15% |

| Draught | 10% |

Why did the Kegs Segment Dominated the Beer Processing Market in 2025?

The kegs segment led the beer processing market in 2025. Growth is driven by expanding craft beer production, rising on-premise consumption, and sustainability preferences favoring reusable or recyclable kegs. The segment also benefits from innovations like smart tracking and automated cleaning systems.

The Cans Segment Expects the Fastest Growth in the Market During the Forecast Period.

The cans segment is grown rapidly due to cans being lightweight, portable, easily stackable, and highly recyclable. Cans also offer excellent protection from light and oxygen, helping maintain beer freshness. Rising demand for craft beer, convenient packaging formats, and sustainable materials has fueled this segment’s expansion.

The bottles segment expects the significant growth in the market. Glass bottles remain popular due to their premium feel, strong barrier properties, and ability to preserve flavor without reacting with the product. This segment is supported by consumer preference for traditional packaging and the premium and craft beer categories.

Heineken Silver

Woodpecker Premium Beer

By Raw Material Type

By Processing Method

By Type

By Packaging Format

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Beer Processing Market