March 2026

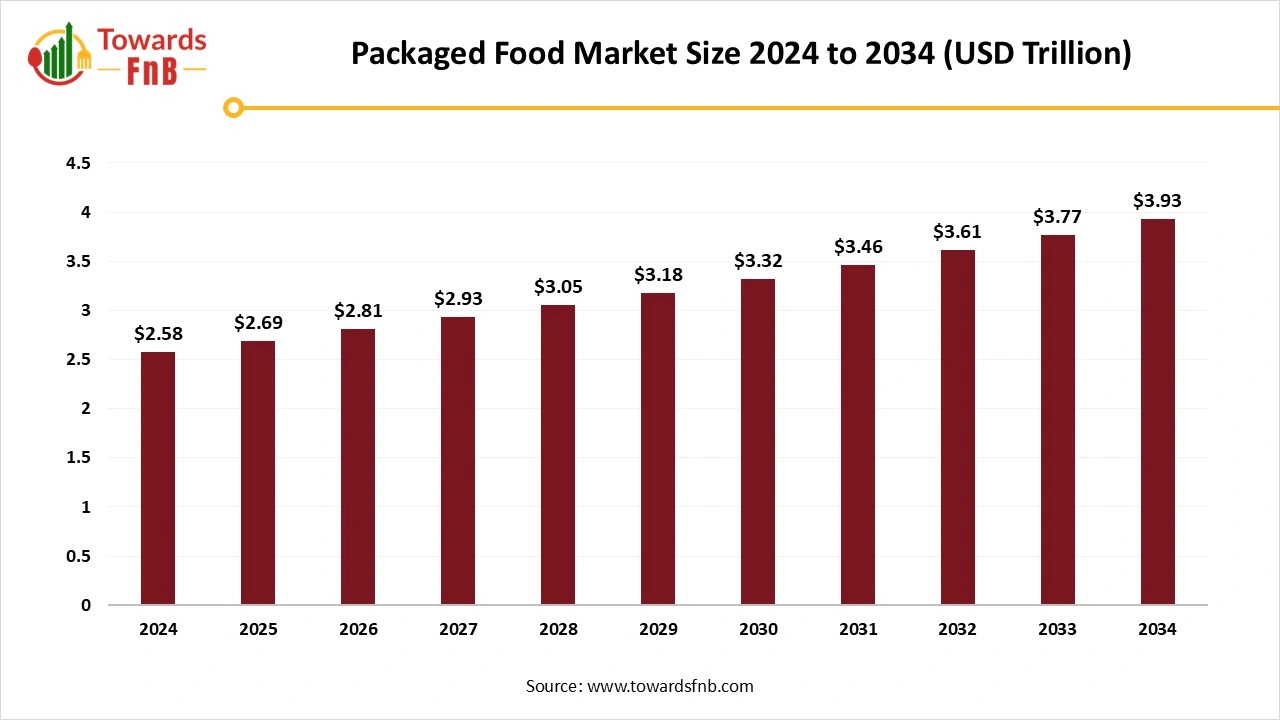

The global packaged food market size reached at USD 6.52 trillion in 2025 and is anticipated to increase from USD 6.80 trillion in 2026 to an estimated USD 9.95 trillion by 2035, witnessing a CAGR of 4.32% during the forecast period from 2026 to 2035. This market is fueled by urbanization, convenience-driven consumer lifestyles, and an increasing demand for sustainable and healthier options.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 4.32% |

| Market Size in 2026 | USD 6.80 Trillion |

| Market Size in 2027 | USD 7.10 Trillion |

| Market Size by 2035 | USD 9.95 Trillion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The packaged food market comprises all branded and private-label food and beverage products that are processed, prepared, portioned, and packaged for retail sale to consumers and food service channels. It includes dry, frozen, chilled and shelf-stable items such as snacks, ready-to-eat meals, dairy & alternatives, bakery products, confectionery, culinary ingredients, processed meat, soups & sauces, and beverage concentrates; distribution channels include supermarkets/hypermarkets, convenience stores, e-commerce, and food service.

The market is driven by convenience, urbanization, longer shelf-life requirements, evolving consumer lifestyles (on-the-go consumption), and product innovation (clean label, functional/healthier formulations), while manufacturers also manage complexity from global supply chains, regulatory compliance, and packaging/ sustainability demands.

Food producers are reluctant to implement new technologies in their production processes for various reasons, such as rising costs, limited employee acceptance, or potential disruptions to their operations. Nonetheless, food producers that have embraced innovative technologies have experienced considerable benefits, like Nestlé. The brand adopted innovative IoT technology in its production line, enabling it to minimize downtime, enhance capacity, boost resource efficiency, and elevate the quality of products for the consumer. The creative combination of nanotechnology and smart packaging utilizes nanoscale materials and devices to create intelligent packaging systems capable of monitoring, safeguarding, and engaging with packaged food. Nanotechnology aids sustainable packaging options by reducing the need for excess materials and enhancing the recyclability of packaging.

Nestlé has committed that by 2025; all of its packaging will be either recyclable or reusable. For instance, the company has transitioned to using entirely recycled PET for its Gerber baby food containers, demonstrating a dedication to circular economy values. This shift not only satisfies consumer demands for sustainability but also demonstrates how companies can grow environmentally conscious while ensuring effective product performance.

Raw Material Procurement

Processing of Packaged Food

Logistic and Distribution

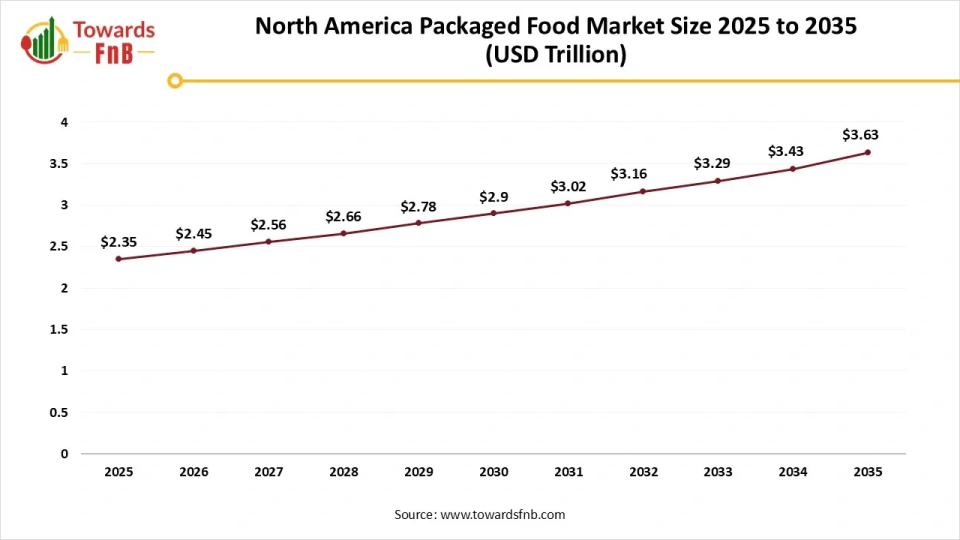

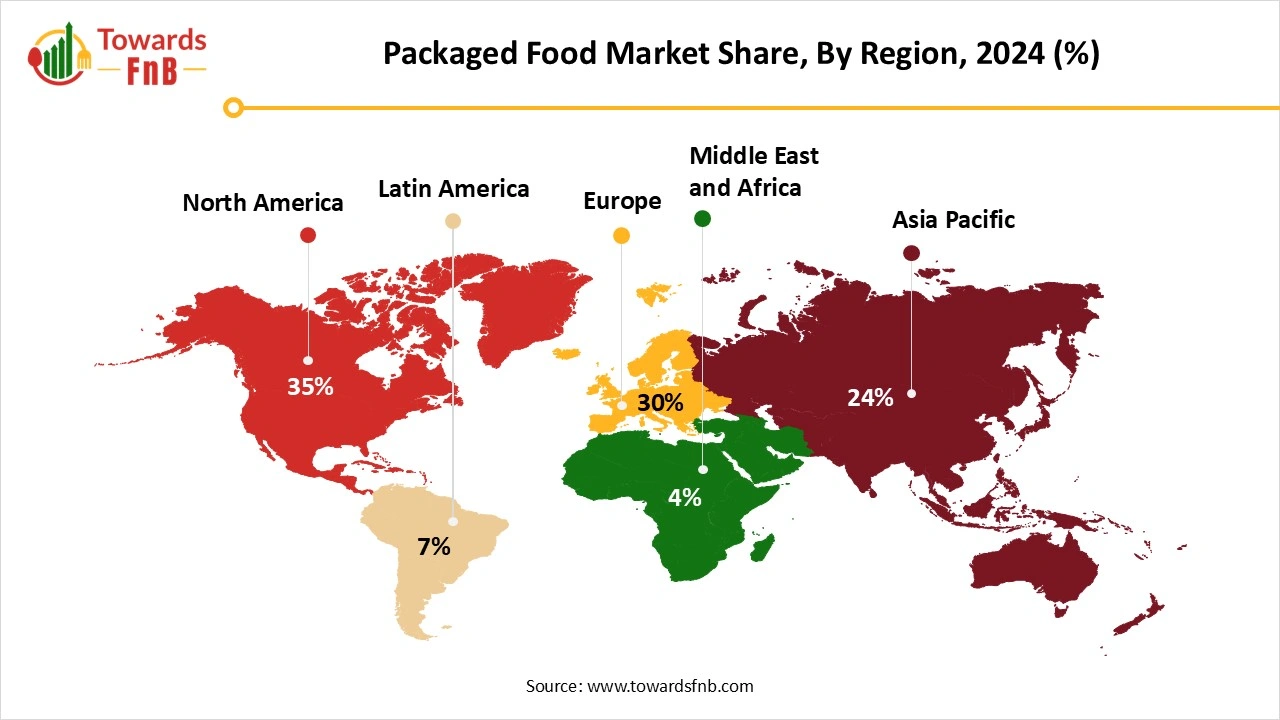

Why did the North America Dominated the Packaged Food Market?

North America held the largest share of the packaged food market in 2025. North America has a growing population residing in urban regions noted for their rapid lifestyles. This demographic change has resulted in an increase in the demand for packaged foods, especially ready-to-eat dishes. E-commerce has become a significant influence on the food packaging market, altering packaging designs to satisfy safety standards during shipping. As online grocery shopping continues to increase each year after the pandemic, the demand for robust and efficient packaging options has escalated. Technological progress in packaging is becoming prominent, with innovations like smart packaging solutions improving product freshness and safety.

North America Packaged Food Market Size 2025 to 2035

The North America packaged food market size was valued at USD 2.35 trillion in 2025 and is anticipated to increase from USD 2.45 trillion in 2026 to an estimated USD 3.63 trillion by 2035, witnessing a CAGR of 4.44% during the forecast period from 2026 to 2035.

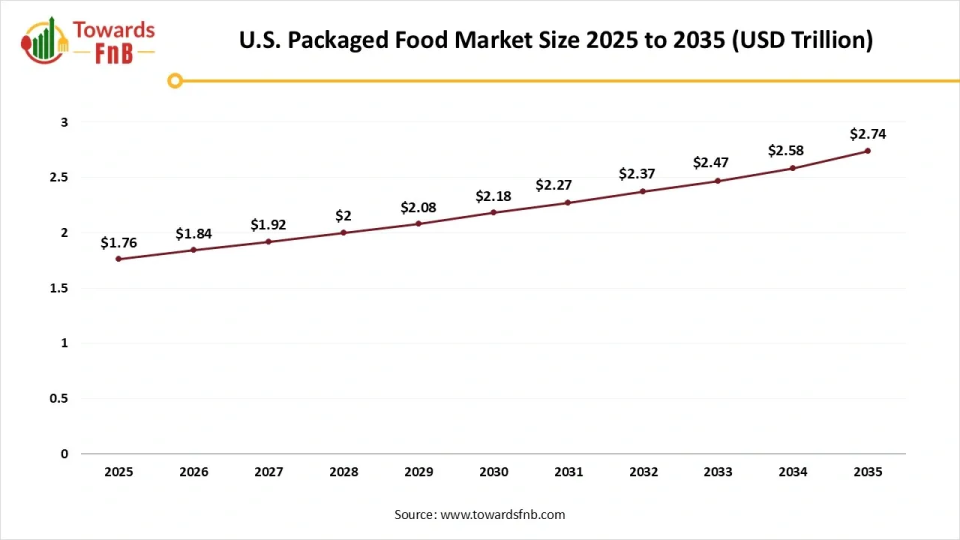

U.S. Packaged Food Market Trends

The busy work and personal routines of consumers nationwide, along with the increasing desire for convenience, have been fueling the market over time. Moreover, the rapid growth of e-commerce in the U.S. increases product sales across the country. Moreover, advancements in food packaging, plant-based items, intense flavors, and nutritious components have played a role in the expansion of the U.S. in the coming years.

U.S. Packaged Food Market Size 2025 to 2035

The U.S. packaged food market size was calculated at USD 1.76 trillion in 2025 and is anticipated to increase from USD 1.84 trillion in 2026 to an estimated USD 2.74 trillion by 2035, witnessing a CAGR of 4.53% during the forecast period from 2026 to 2035.

What Factors are Influencing the Packaged Food Market of the Asia Pacific?

Asia Pacific expects the significant growth during the forecast period. The packaged food market in the Asia-Pacific region is expanding rapidly because of higher consumer demand for convenient foods, swift urban growth, a broadening retail industry, and increasing disposable income. Moreover, robust government programs advocating for sustainability and environmentally friendly packaging materials enhance regional development. Businesses are concentrating on innovative products and broadening their selections to align with changing consumer demands for healthier alternatives.

India Packaged Food Market Trends

The packaged food market in India has experienced significant growth lately, driven by changing consumer habits, urban development, and a rising need for convenience. The growth of this market can be linked to reasons including increasing disposable incomes, evolving dietary choices, and a rise in dual-income families, which have caused a change in consumer habits favoring ready-to-eat and convenient food products. Additionally, in a diverse nation like India, characterized by various culinary traditions, the packaged food sector has adjusted by providing a selection of products that address local preferences.

")

Expanding Packaged Food Market of Europe

Packaged food market of Europe is growing at a notable rate. Major factors consist of rising consumer appetite for convenient and packaged fresh foods, an increased focus on sustainable and environmentally friendly packaging, and the necessity to prolong food shelf life. Flexible packaging is now the biggest and quickest-growing segment, showing robust performance in areas such as ready meals, chilled and frozen food, and breakfast cereals. The European Commission has programs such as the "5 R's" (Refuse, Reduce, Reuse, Recycle, Renewable) to encourage a more sustainable packaging value chain.

UK Packaged Food Market Trends

The packaged food market in the United Kingdom is expected to grow throughout the forecast period. The market is growing because of heightened health awareness, greater demand for convenient food options, and government efforts to minimize food waste and enhance nutritional labeling. A significant trend in the market is the increasing demand for gluten-free, low-sugar, and fortified packaged foods, especially in breakfast products, baby food, and functional snacks. The UK's robust private label sector is fostering innovation, providing cost-effective premium-style packaged food options on both grocery and e-commerce platforms.

Growing Packaged Food Market of Latin America

Latin America packaged food market is growing rapidly. Different factors, including shifts in lifestyle, rising disposable income, and swift urbanization in developing nations particularly the expanding middle-income demographic are boosting the need for bags for frozen food. The rise in population density has boosted the demand for packaged food overall, with Millennials playing a role in this expansion. Millennial consumers typically influence the demand for frozen food packaging items, and they represent 30% of the overall Latin American population. These individuals have a strong liking for single-serving and convenient food and beverage items.

Brazilian Packaged Food Industry Trends

The Brazilian packaged food industry is an important and expanding field, fueled by a considerable urban population and a rising middle class in search of convenient and health-oriented choices. The sector reconciles the consumer desire for cost-effectiveness with the drive for advancements in high-quality, nutritious, and eco-friendly products. A rising demand for health-oriented options exists as consumers gain greater awareness of nutrition and wellness. This has resulted in an increase in organic and natural items, with numerous brands adjusting their products to align with this trend.

Middle East and Africa Packaged Food Market

The packaged food market in the Middle East and Africa is seeing considerable expansion, fueled by various elements that demonstrate evolving consumer tastes, increased urbanization, and a growing need for convenient and ready-to-eat meal choices. With the economic development and urbanization of the region, lifestyles are noticeably changing, as an increasing number of consumers prefer packaged foods for their convenience and time-saving benefits. The market for packaged foods encompasses a variety of items, including snacks, prepared meals, and easily accessible foods, addressing the changing demands of a society with hectic lifestyles and a growing emphasis on convenience.

Saudi Arabia Packaged Food Market Trends

Packaged food market in Saudi Arabia growing at notable rate. Increasing demand in the booming F&B sector is benefiting the market. With the industry's growth in processed, ready-to-eat, and convenience food items, producers persist in depending on efficient packaging to maintain freshness, prolong shelf life, and guarantee product safety. Increased use of automation is providing a positive market perspective. Automated systems assist manufacturers in accelerating production lines, minimizing manual mistakes, and upholding hygiene standards, which are crucial for managing food products. The rising use of sustainable and recyclable packaging materials is driving market expansion.

Packaged Food Market Share, By Product Type, 2025 (%)

| Segments | Shares (%) |

| Snacks | 20% |

| Beverages Non-alcoholic | 15% |

| Dairy & Frozen | 13% |

| Bakery & Confectionery | 12% |

| Meat & Poultry | 10% |

| Health & Nutrition/Functional Foods | 8% |

| Canned & Ready Meals | 7% |

| Confectionery | 5% |

| Sauces, Dressings & Condiments | 4% |

| Oils & Fats | 3% |

| Baby Food | 2% |

| Others | 1% |

Which Product Type Dominated the Packaged Food Market?

The snacks segment led the packaged food market in 2025, due to factors like convenience, evolving consumer habits, and urban growth. Snacks are simple to transport, easy to eat, and quite delicious. As a result, they are eaten by individuals from various age groups several times daily. Because of busy consumer lifestyles, many opt for a meal replacement as a snack when time is limited.

The Health & Nutrition/Functional Foods Segment is Observed to Grow at the Fastest Rate During the Forecast Period

This expansion has been fueled by a broad consumer emphasis on gut health and its connection to immunity, energy, and mental wellness. Businesses in the food and beverages industry are progressively allocating resources toward functional formulations, backed by scientific evidence and growing consumer demand for clean-label ingredients.

The dairy & frozen segment is expanding at a notable rate. Dairy items like individual yogurt, convenient milk and frozen items, instant meals, and pre-chopped vegetables provide fast, easy options that conserve time and energy. Freezing and sophisticated dairy processing methods, such as UHT and aseptic packaging, greatly increase product longevity compared to fresh options.

Why did the Bottled Segment Dominated the Packaged Food Market?

Bottled segment held the dominating share of the packaged food market in 2025. The rising need for dairy drinks is boosting the demand for bottles within the food packaging sector. Health trends encouraging hydration and unique beverages enhance the bottle segment. Developments in lightweight, sustainable bottle designs and the emergence of biodegradable alternatives also contribute to market expansion.

Flexible Pouches & Stand-Up Pouches Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

The growth of urbanization and evolving lifestyles are driving up the need for convenient packaging solutions, where flexible printed plastic pouches stand out because of their lightweight and portable characteristics. Additionally, they are lightweight, convenient to carry, attractive on shelves, and simple to re-seal and store; moreover, pouch nozzles enhance their usability.

The canned/metal packaging sector is experiencing substantial growth throughout the forecast timeline. Metal packaging, especially in cans, is commonly utilized in numerous sectors because of its strength, light weight, and ability to be recycled. Cans are mainly located in the food and drink industry, where they act as vessels for items like soft drinks, beer, and canned goods.

Which Distribution Channel Dominated the Packaged Food Market?

Supermarkets/hypermarkets/modern grocery segment dominated the market with the largest share in 2025. Their superiority stems from a wide range of products, attractive pricing, and a robust brand image. Thanks to promotional deals, in-store tastings, and improved packaging, the shopping experience has enhanced consumer convenience, leading to increased purchases of convenience foods at retail outlets.

Online Grocery/E-Commerce Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Fueled by a strong desire for convenience stemming from contemporary, fast-moving lifestyles, along with significant rises in internet access and smartphone adoption.

Traditional/independent retail/mom-and-pop segment growing at notable rate. These retailers provide services customized for local demands, including home delivery and interest-free financing, which their customers greatly appreciate. In contrast to large corporations, small family-owned shops can swiftly adjust their products and operating hours to meet local demands without dealing with corporate red tape.

Packaged Food Market Share, By End-User/Consumer Type, 2025 (%)

| Segments | Shares (%) |

| General adult consumers | 65% |

| Seniors / Older adults | 7% |

| Children | 10% |

| Teenagers | 5% |

| Infants | 2% |

| Other / Institutional consumers | 11% |

Which End User Segment Dominated the Packaged Food Market?

General adult consumers segment held the largest share of the market in 2025. Many adults, especially in city settings and two-income families, face hectic job demands and have little time for conventional meal cooking. The overall adult demographic is becoming more health-aware and is actively looking for packaged foods that provide nutritional advantages, including organic, low-sugar, gluten-free, or protein-enhanced choices.

Seniors/Older Adults Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Currently, numerous older individuals desire a vibrant and healthy way of living. As a result, they largely favored convenient and nutritious packaged food choices. Consequently, a more active lifestyle and altered dietary habits have boosted the need for packaged foods, propelling market expansion.

The children's segment is expected to expand notably throughout the forecast period. The rise in demand from parents for nutritious, functional, and clean-label products that meet children's nutritional needs fuels growth. The increasing need for easy baby food packaging is mainly fueled by hectic lifestyles. Urbanization and increasing disposable income allow parents to opt for premium baby food products.

UFlex Ltd

Corporate Information

History and Background

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Key Acquisitions

Partnerships & Collaborations

Product Launches/Innovations

Key Technology Focus Areas

R&D Organisation & Investment

SWOT Analysis

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Packaging Type

By Distribution Channel

By End-User/Consumer Type

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMarch 2026

March 2026

March 2026

March 2026

Packaged Food Market