April 2026

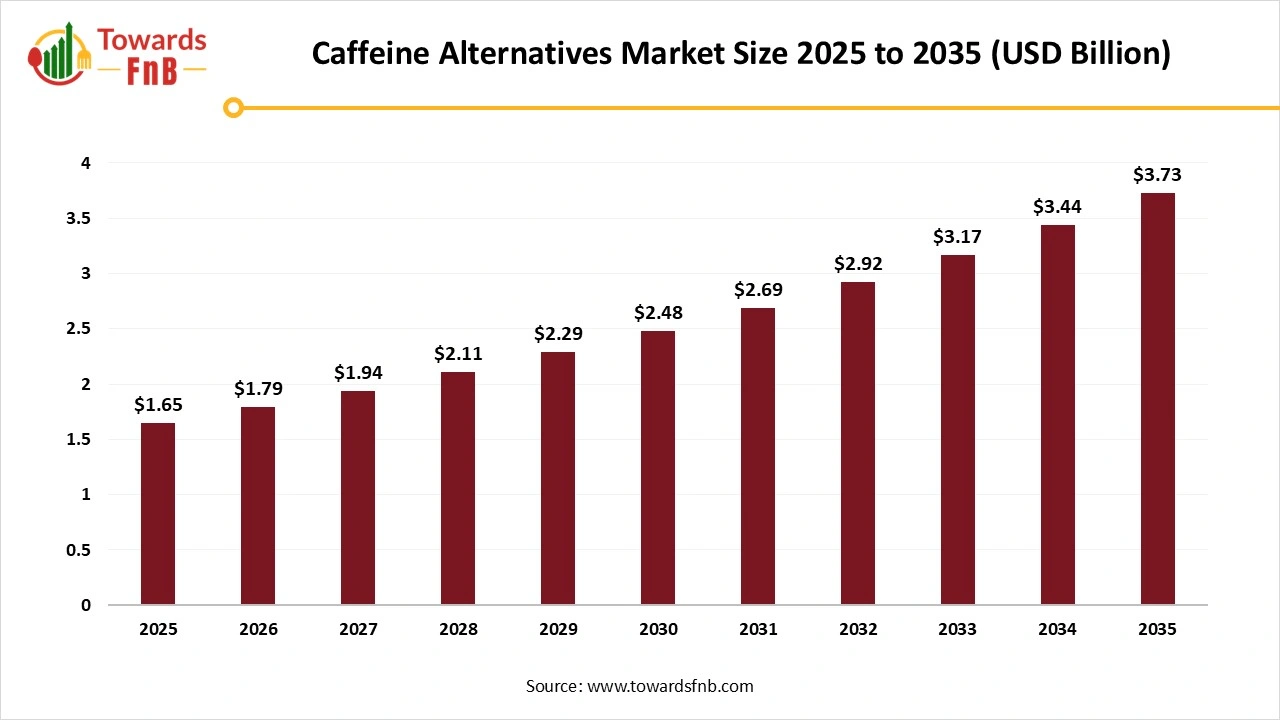

The global caffeine alternatives market size was estimated at USD 1.65 billion in 2025 and is expected to grow steadily from USD 1.79 billion in 2026 to reach nearly USD 3.73 billion by 2035, with a CAGR of 8.5% during the forecast period from 2026 to 2035. The market is experiencing the significant growth due the awareness about side effect of caffeine and growing demand for plant-based and natural products.

| Study Coverage | Details |

| Growth Rate from 2026 to 2035 | CAGR of 8.5% |

| Market Size in 2026 | USD 1.79 Billion |

| Market Size in 2027 | USD 1.94 Billion |

| Market Size by 2035 | USD 3.73 Billion |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

The caffeine alternatives market comprises plant-based, herbal, functional ingredient, and synthetic-free products designed to provide energy, alertness, and focus without the stimulant effects of caffeine. These alternatives aim to reduce side effects such as jitteriness, anxiety, and sleep disruption commonly associated with caffeine. They include adaptogens, nootropics, botanical extracts, amino acids, vitamins, and functional beverages formulated for sustained energy release, stress reduction, and cognitive performance. Products are consumed in formats such as beverages, supplements, powders, snacks, and capsules, and are targeted at health-conscious consumers, athletes, working professionals, and those with caffeine sensitivity.

The increasing consumer trend towards healthier living creates considerable market prospects for the caffeine alternatives sector. With an increasing number of people recognizing the harmful health effects linked to high caffeine intake, there is a growing interest in drinks that provide natural energy, calmness, and mental clarity without negative consequences. This trend creates avenues for businesses to create and produce new, practical drinks that appeal to health-minded consumers. The growing use of caffeine alternatives in the pharmaceutical industry is expected to generate significant and substantial opportunities for overall market expansion.

A significant challenge confronting the caffeine alternatives market is how consumers perceive the efficacy and reliability of these products compared to traditional sources such as tea and coffee. Due to scientific validation and cultural acceptance, numerous consumers view coffee and tea as dependable sources of energy and stimulation. Persuading consumers that caffeine alternatives can provide comparable benefits without the potential drawbacks of conventional caffeinated drinks such as anxiety, disrupted sleep, or addiction continues to be a challenging endeavour, fueled by rising demand for healthier, caffeine-free options and eco-friendly products.

Raw Materials Procurement

Retail Sales & Marketing

Waste Management & Recycling

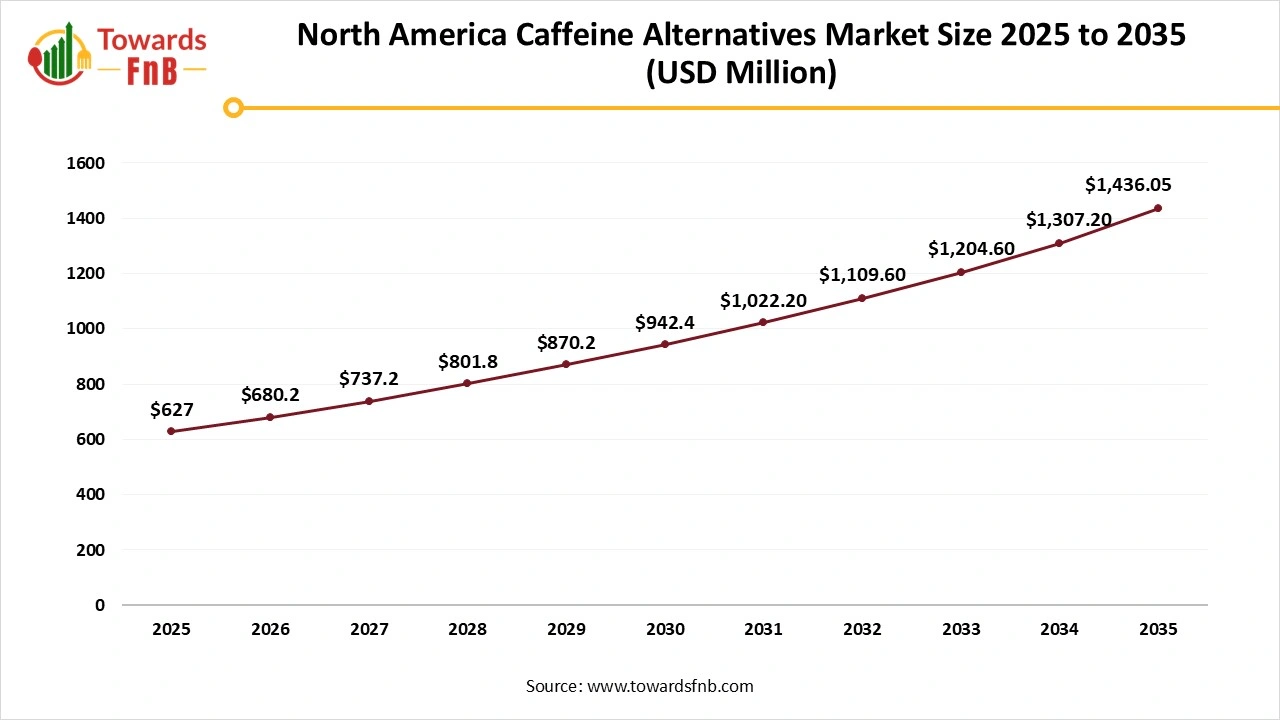

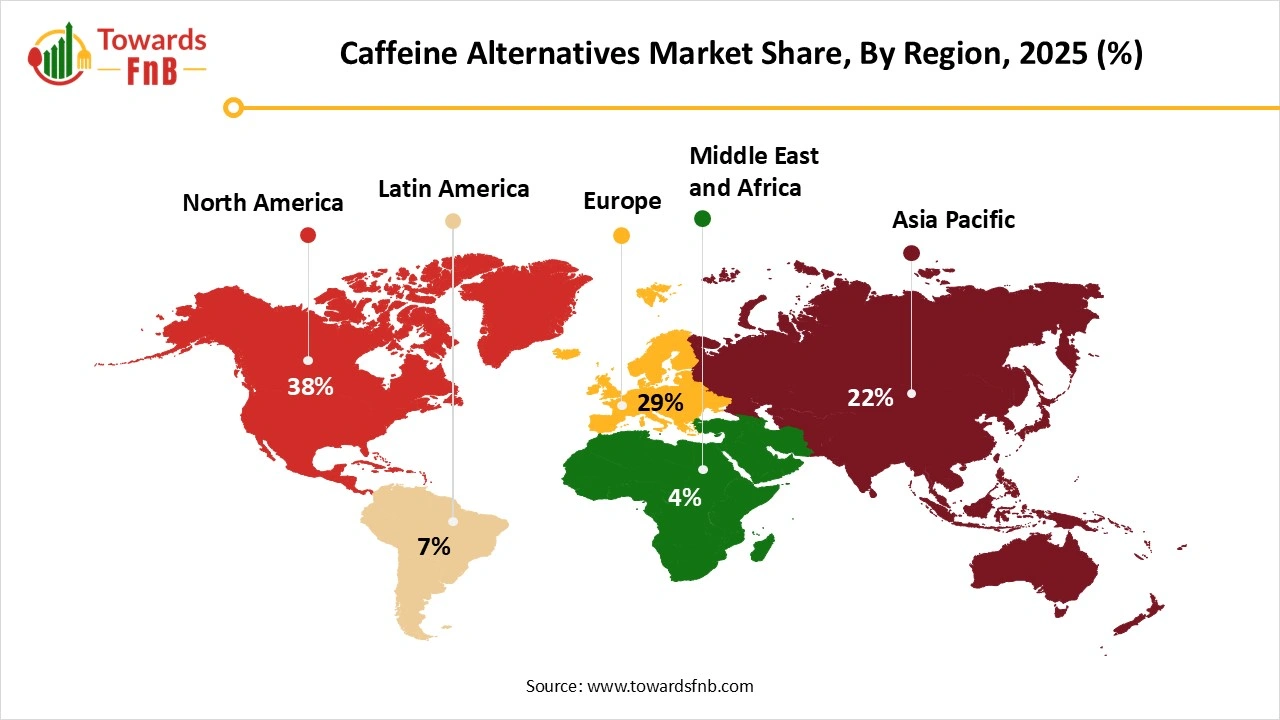

North America Dominated the Caffeine Alternatives Market in 2025

The area's increasing emphasis on wellness and organic items boosts the need for coffee alternatives created from chicory, barley, and various natural components. The market gains from a robust retail infrastructure, comprising supermarkets, specialty shops, and online platforms that improve product accessibility. Furthermore, the development of new products and increasing health awareness drive market expansion. The varied consumer base and considerable disposable income in North America provide chances for market growth and the launch of new coffee substitute products. The National Coffee Association reports that 62% of Americans consume coffee every day. Statista reports that almost 80% of coffee drinkers in the US have more than one cup of coffee each day while at home. Excessive caffeine consumption can make an individual feel nervous and restless. It may elevate their heart rate, worsen high blood pressure, and result in digestive issues and even sleeplessness.

North America Caffeine Alternatives Market Size 2025 to 2035

The North America caffeine alternatives market size was calculated at USD 627 million in 2025 with projections indicating a rise from USD 680.2 million in 2026 to approximately USD 1,436.05 million by 2035, expanding at a CAGR of 8.64% throughout the forecast period from 2026 to 2035.

In Canada, the need for caffeine alternatives is rising because of heightened health consciousness and a preference for healthier living. Consumers are looking for substitutes to conventional caffeinated items to prevent possible side effects such as anxiety, sleep disturbances, and dependency linked to high caffeine consumption. Additionally, there is an increasing enthusiasm for functional drinks and natural energy enhancers that provide prolonged energy and mental clarity without adverse effects.

Asia Pacific Expects the Significant Growth During the Forecast Period

Consumers in the Asia-Pacific region are progressively favoring ethically sourced items, emphasizing social and environmental factors, particularly prevalent in caffeine alternatives products. The movement for organic certification in the caffeine alternatives industry is escalating in Asia-Pacific consumer markets, particularly in nations like India and China. Most local consumers think that goods produced organically decrease exposure to synthetic chemicals and pesticides, increasing the demand for certified organic caffeine alternative products. The organic movement has gained prominence in the coffee alternative sector, propelled by an increase in people who acknowledge the advantages of the organic and sustainable method.

")

The India caffeine alternatives market has been experiencing significant growth due to increased health awareness among consumers and the rising trend of alternative drinks. Moreover, increasing disposable income and evolving consumer preferences further drive the market's expansion. The market is fueled by the growing population of young buyers seeking alternative choices that align with their evolving tastes. Various alternatives to coffee include chamomile and Tulsi tea, as well as traditional Indian drinks like masala chai.

Europe holds significant growth due to the growing demand for plant-based clean-label beverages and increased health consciousness. In place of conventional caffeinated products, consumers are increasingly choosing adaptogenic formulations,, chicory-based beverages, and herbal infusions. Product quality and consumer trust are further improved by strict regulatory requirements for food safety and labeling. Furthermore, the region's ongoing market expansion is being bolstered by the growing functional beverage industry.

Germany Caffeine Alternatives Market Trends

Germany is leading, motivated by a strong culture of herbal beverage consumption and a high awareness of natural wellness products. Consumers who are concerned about their health are becoming more interested in organic caffeine-free coffee alternatives and botanical beverages. Product availability is facilitated by the nation's specialized health stores and well-established retail infrastructure. Purchase behavior is also being influenced by growing interest in locally sourced and sustainable ingredients.

The MEA region is witnessing rapid growth because of growing urbanization and awareness of health issues associated with lifestyle choices. As part of healthier lifestyle choices,, consumers are investigating herbal teas and natural energy-boosting beverages. Market accessibility is increasing because of growing retail chains and e-commerce sites. Regional demand is also being supported by trends in premium beverages and the growing number of young people.

UAE Caffeine Alternatives Market Trends

UAE is emerging, fueled by a high demand for wellness-focused and functional drinks. Diverse consumer preferences are a result of both a large expat population and high disposable income. Novel caffeine-free blends and botanical drinks are being introduced by specialty cafés and health-conscious retail establishments. Another factor driving the nation's adoption of caffeine substitutes is the growing emphasis on productivity, fitness, and balanced lifestyles.

Which Product Type Dominated the Caffeine Alternatives Market in 2025?

Herbal botanical alternatives segment dominated the caffeine alternatives market in 2025. This expansion is linked to the rising consumer inclination towards natural and plant-based products, driven by heightened health awareness and a focus on preventive healthcare. A range of instant products and caffeine alternative mixes are available on the market, particularly those made from various plants and herbs such as ginger, rye, date pits, quinoa, lupine, chicory, barley, and oak, among others. These coffee alternatives offer various benefits, particularly being caffeine-free and containing a range of helpful phytochemicals.

Adaptogens & Functional Mushrooms Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Fueled by increasing consumer awareness regarding mental clarity, stress alleviation, and natural energy enhancers, where adaptogen-infused products have become increasingly popular. Rising consumer interest in functional drinks and natural, holistic methods to improve wellness. The market serves consumers looking for healthier substitutes for conventional coffee, along with individuals interested in natural solutions and functional food. This trend is additionally amplified by the addition of medicinal mushrooms like Lion's Mane, Chaga, and Reishi, which provide potential cognitive benefits, stress alleviation, and immune assistance.

Caffeine Alternatives Market Share, By Source, 2025 (%)

| Segments | Shares (%) |

| Plant-derived | 60% |

| Synthetic-free formulations | 40% |

Which Source Dominated the Caffeine Alternatives Market in 2025?

Plant derived segment held the dominating share of the caffeine alternatives market in 2025. Consumers are progressively attracted to natural and plant-derived components, pursuing products that match their desires for transparent labeling and eco-friendly sourcing. Consumers are progressively favoring drinks that adhere to sustainable, natural, and cruelty-free values. This change is driven by worries about the environmental effects of conventional farming methods and a quest for cleaner, more transparent goods. Consequently, beverages made from plants, including herbal tea, adaptogenic drinks, and fruit-infused waters, are becoming increasingly popular.

Synthetic-Free Formulations Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Shoppers are focusing on products with transparent labels, indicating a preference for items that contain natural, organic, and non-GMO components. Herbal extracts, adaptogens, and specific plants serve as natural alternatives that offer a steadier and more balanced energy increase, free from the jitters linked to caffeine. Consumers are progressively looking for products that correspond with health and wellness trends, resulting in a boost in demand for natural stimulants and functional drinks.

Caffeine Alternatives Market Share, By Formulation, 2025 (%)

| Segments | Shares (%) |

| Solid | 10% |

| Liquid | 60% |

| Powder | 30% |

Why did the Liquid Segment Dominate the Caffeine Alternatives Market in 2025?

Liquid segment dominated the market with the largest share in 2025, driven by increasing consumer demand for ready-to-drink coffee alternatives that provide convenience for busy lifestyles. Consumers on the go are increasingly favoring ready-to-drink beverages, like bottled herbal or grain-based coffee substitutes, which align perfectly with their hectic lifestyles. The liquid version also matches trends in functional drinks, as numerous RTD items are enhanced with superfoods, adaptogens, and other health-boosting components, attracting wellness-oriented customers.

Powder Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

Powdered caffeine alternatives are preferred for their convenience, enabling users to blend them into different drinks and meals. They also possess an extended shelf life in comparison to liquid versions, rendering them more attractive to consumers and retailers alike. The rise in popularity of sports and fitness has resulted in a higher demand for caffeine powder as a boost for performance. It is frequently utilized by athletes and fitness lovers to enhance stamina and lessen tiredness.

Caffeine Alternatives Market Share, By Function, 2025 (%)

| Segments | Shares (%) |

| Energy & Stamina | 50% |

| Mental Focus & Cognitive Support | 25% |

| Stress Reduction & Relaxation | 15% |

| Endurance & Athletic Performance | 10% |

How did the Energy & Stamina Segment Hold the Largest Share of the Caffeine Alternatives Market in 2025?

Energy & stamina segment held the largest share of the market in 2025. This is largely because of the rising demand for energy drinks among young adults, athletes, and professionals looking to enhance physical endurance and performance. The increase in the workforce and the demand for convenient, portable energy options have also played a role in the prominence of the energy and stamina sector. Functional drinks, which include herbal extracts, adaptogens, and vitamins, are becoming more popular as they provide advantages that exceed basic nutrition and enhance overall wellness.

Mental Focus & Cognitive Support Segment is Observed to Grow at the Fastest Rate During the Forecast Period

Propelled by the increasing need for enhancing mental performance. Additionally, significant transformations have been taking place in consumers' everyday lives that result in both physical and emotional strain. This has led to the incorporation of drinks and foods beneficial for brain health into their diets. Mental well-being is increasingly important to a large group of consumers worldwide who are willing to invest in products that enhance their mental health.

Why did the Health-Conscious Consumers Segment Dominated the Caffeine Alternatives Market in 2025?

Health-conscious consumers segment led the market in 2025. Increasing consumer awareness about health and wellness is driving demand for products. An increasing number of consumers are depending on nutraceuticals products, including functional foods and drinks, to maintain a healthy lifestyle and avoid illnesses. Numerous people are looking for substitutes for caffeine to steer clear of its negative impacts, including anxiety, sleeplessness, and dependency. This change is driving an increased demand for natural and plant-derived energy boosters, as consumers favor healthier choices that enhance general wellness. As buyers seek drinks that align with their health objectives, the market for caffeine alternatives is growing to feature items that provide these practical benefits.

Athletes & Fitness Enthusiast's Segment is Seen to Grow at a Notable Rate During the Predicted Timeframe

Caffeine alternatives seek to appeal to various customers, such as fitness lovers and professional athletes, because of their ability to enhance physical performance and aid in recovery. Producers of sports energy drinks are adding adaptogens such as ashwagandha for quick stress relief, along with plant-based ingredients high in electrolytes, probiotics, and BCAAs, to enhance gut health, aid muscle recovery, and boost immunity. Therefore, it transcends merely being a liquid to restore.

Which Distribution Channel Dominated the Caffeine Alternatives Market in 2025?

Online retail / e-commerce segment held dominating share of the market in 2025. The caffeine alternatives e-commerce platform has witnessed significant growth in recent years, fueled by a combination of changing consumer preferences, technological progress, and the broader digital retail environment. The growth of internet availability and smartphone usage has greatly reduced entry obstacles for consumers and specialty coffee brands, allowing for smooth online buying experiences. Today’s consumers are increasingly looking for convenience, customization, and a wider variety of coffee options.

Direct-to-Consumer (Brand-Owned Platforms) Segment is Expected to Grow at the Fastest Rate in the Market During the Forecast Period

D2C brands can interact directly with consumers, grasp their preferences, and customize their marketing strategies, resulting in enhanced brand loyalty and sales. D2C brands can experience quick expansion by emphasizing creativity, providing attractive pricing, and cultivating robust online communities. Brands such as Four Sigmatic and Ryze have effectively utilized the D2C model in the coffee substitutes market by providing mushroom-infused items.

HTeaO

Sip Herbals

Miko

By Product Type

By Source

By Formulation

By Function / Benefit

By End-User

By Distribution Channel

By Region

Principal Consultant

Vidyesh Swar, Senior Research Analyst at Towards Food & Beverages, specializes in market research, focusing on supply-demand evaluation, pricing analysis, alternative proteins, plant-based foods, and sustainable food technologies within the industry.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in Food and Beverages market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards FnB's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarApril 2026

April 2026

April 2026

April 2026

Caffeine Alternatives Market